With the recent Union budget focusing on infrastructure and growth, investors are looking at companies with strong fundamentals that could help spawn returns in the long run. KNR Constructions is one such stock, according to many analysts.

Although underlying concerns regarding order wins persist, market participants are upbeat about the company's growth prospects in the long run.

For FY24, the budget allocation for roads was increased by 25 percent to Rs 2.59 lakh crore, after a 16 percent rise in FY23. ICICI Securities said the increase in road capex is positive for engineering, procurement and construction (EPC) companies in the road segment because orders will get a boost. And several analysts have touted KNR Constructions as one of the beneficiaries.

In 2022, the stock touched a low of Rs 202.85 and a high of Rs 330. On February 15, 2023, the scrip settled 0.4 percent lower at Rs 255.65 on the BSE, which means the stock is still 22.5 percent away from 2022's high.

About the company

KNR Constructions is an EPC company headquartered in Hyderabad. Its major projects are in the roads and highways segment and it has an established presence in irrigation and urban water infrastructure management as well.

Its order book as on December 31, 2022, stood at Rs 8,100 crore, out of which Rs 6,256.4 crore was from the road sector and Rs 1,843.7 crore from the irrigation sector.

Besides, out of the total order book, 36 percent of orders are from state governments while central government orders form 11 percent of the book. The order book translated into a revenue visibility of around 2.5 times its FY22 revenue, said Nuvama Wealth and Investment.

On a consolidated basis, the company's revenue from operations in the December quarter rose to Rs 874.93 crore from Rs 854.64 crore in the corresponding period in the previous year while net profit jumped 112 percent YoY to Rs 105.76 crore.

Higher raw material costs led to the operating margin shrinking to 19 percent in the quarter under review from 21 percent a year earlier.

For FY23 and FY24, the company’s revenue guidance stands at Rs 3,500 crore and Rs 4,000 crore, respectively, and it has guided for EBITDA (earnings before interest, taxes, depreciation and amortisation) margin remaining between 18 and 19 percent.

Recoveries from the Telangana state government toward irrigation orders and monetisation proceeds from the consummation of transaction with Cube Highways helped KNR Constructions turn net-cash again with a net cash balance of about Rs 125 crore at end of Q3 FY23. This is against around Rs 16o crore net debt at end-Q2.

Why the bullishness?

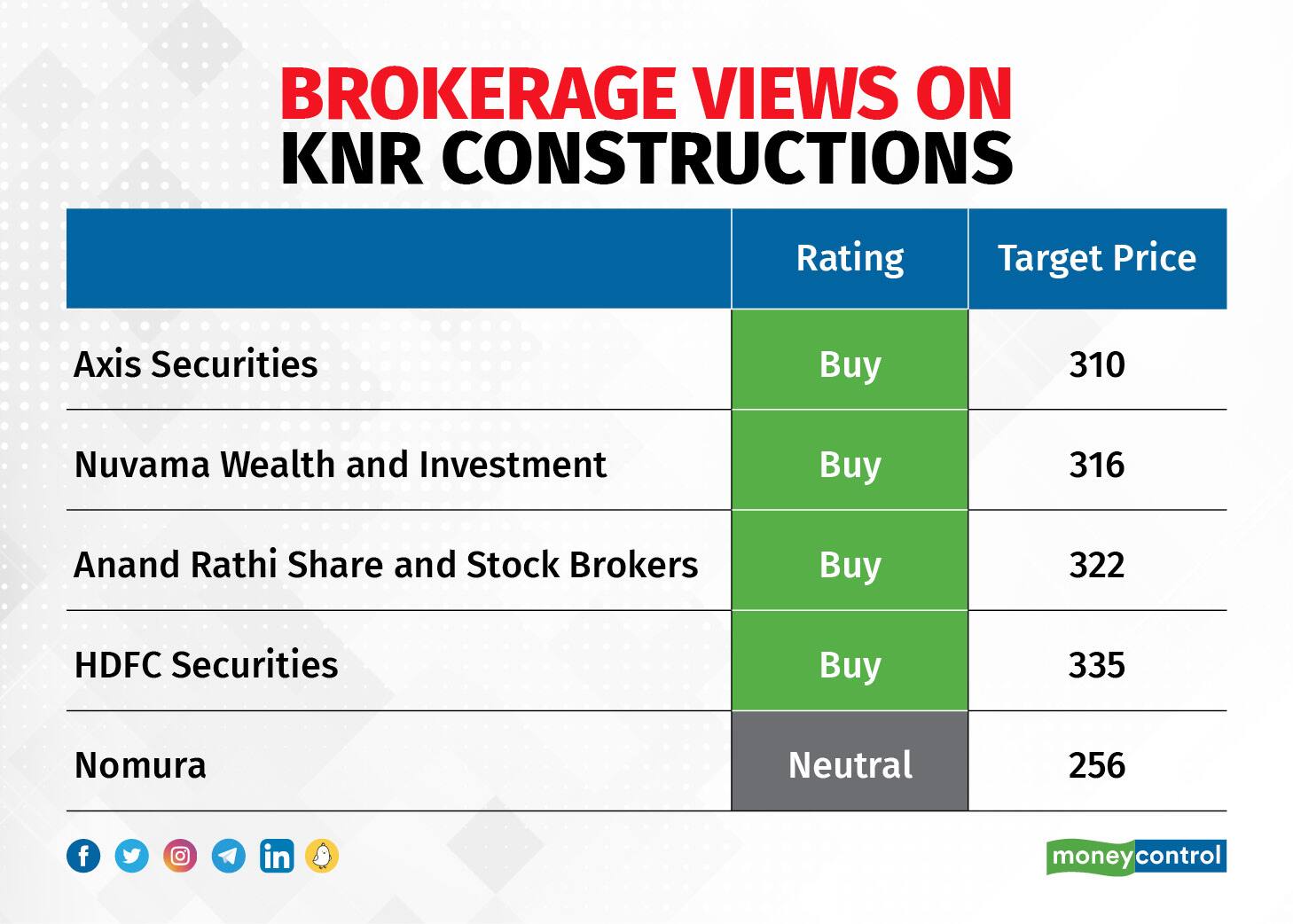

The company's robust order book gives revenue visibility over the next two-three years, said Axis Securities. "With a healthy NHAI (National Highways Authority of India) pipeline, we expect the company to receive better order intake which shall drive its revenue growth moving forward. We expect the company to grow its revenue at a CAGR (compound annual growth rate) of 11 percent over FY22-24," the domestic brokerage firm said.

Also Read | This capital goods stock may rise another 45% on green energy push

Newer opportunities emerging in various infra-related sectors and further diversification augurs well for the company, especially since the company is looking to enter other segments such as railways and metros to keep the revenue stream unaffected.

Nuvama Wealth and Investment said, "We remain positive on KNRC’s (KNR Constructions) strong execution capabilities and lean balance sheet (stemming from a healthy operating cash flow), despite short-term challenges pertaining to a dwindling order book."

What's the hiccup?

Axis Securities cautioned, "The absence of major order wins to date in FY23 remains a concern," while appreciating the company’s policy of not chasing orders at a lower margin.

The company has not bagged any major order since September 2021, which has led to a moderation in revenue visibility. The management has attributed the lower order inflows to higher competitive intensity in the road segment, noted Nuvama Wealth and Investment.

"However, the build-up in order book remains critical to sustain its revenue growth momentum," it added.

Owing to subdued revenue growth in Q3, Nuvama Wealth and Investment trimmed its FY23 earnings estimate by around 8 percent and also cut its FY24 EPS estimate by 7 percent to factor in the risk of a delay in order inflow.

Even Anand Rathi Share and Stock Brokers is of the opinion that order additions remain an area of concern, and need to be addressed at the earliest. The brokerage also highlighted that stiff competition in the road sector affects the company.

Nomura believes that lack of order inflows due to aggressive competition and a depleted order book leads to concerns.

The foreign brokerage firm pointed out that the key upside risk is a spike in order wins while delay in payments in state government projects and aggressive competition are downside risks.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.