Fund managers have told market regulator Sebi that they expect market manipulation in the derivatives segment, possibly by a major player. These fund managers, which manage substantial assets under management (AUM) and are based both in India and abroad, are not naming names say they have observed suspicious trading patterns and that they will reduce exposure significantly if this continues unchecked.

According to sources, the Securities and Exchange Board of India (SEBI) is evaluating the submissions but has yet not found evidence of manipulation. Sebi’s probe is ongoing.

To buttress the manipulation charges, market participants cite the example below:

February 1, 3.30 pm, Sensex: 77506; price of Sensex 77500 call, 4th Feb Expiry: Rs 300.

February 4, 1.30 pm, Sensex: 78277; price of Sensex 78300 (ATM) call, 4th Feb expiry: Rs 319.45

They point out that there was hardly any difference between the price of similar options on very different days. One was the day the Union Budget was presented, which was three days away from expiry day, which should translate to higher uncertainty around the Sensex expiry price and therefore higher option prices. The other was an uneventful day and an expiry day, with as little as two hours to expiry, both of which should translate to less uncertainty and less option price. And yet, the prices were similar.

Also read: Mutual funds, SEBI likely to lock horns in key meet today on proliferation of thematic funds

“It is like betting on a horse race that's 500 metres before the finish line and another race that's 5 metres before the finish line by factoring in the same level of uncertainty,’ said one of the sources cited.

Fund managers who cumulatively hold three decades' experience trading options and with an impressive return profile—one even delivering 40 percent returns with 5 percent drawdown for nearly a decade - told Moneycontrol that they and many of their peers see this as an indication that there is a fund or collective of funds that could be manipulating the Indian derivatives market.

While this has impacted the returns of many fund managers, others have managed to protect their returns by guessing the moves of the suspect entities and aligning their trades to it. But, according to a fund manager whose returns have not been affected so far, the returns are not the chief concern since they can and have found ways to adapt. The chief concern is the integrity of the Indian securities market, which can be compromised.

So, what is the alleged oddity?

Derivative prices are supposed to move in tandem with the underlying asset or with an expected move in the underlying asset, in this case the index. In the Indian market, things are different, said the fund managers.

What they are seeing is a sharp price movement in derivatives and then a subsequent price movement in the underlying asset to justify the former.

Those are what they have come to call “violent expiry days”.

“On such days, implied volatility (IV) of options goes from 12 percent to 36 percent for no reason… it’s beyond 3 sigma, beyond bizarre,” said a fund manager, who spoke on condition of anonymity.

Implied volatility (IV) is a measure of how much the market believes the price of the underlying (Nifty/ Sensex) can fluctuate and sigma is the standard deviation in its levels. Therefore 3 sigma would mean that the market was expecting the underlying price to be three standard deviations away from the existing level.

According to a fund manager, a 3-sigma move is meant to happen once in 300 days, but it is happening on every expiry. "Someone is clearly buying options in bulk, causing the prices to become exorbitant and then moving the market to profit disproportionately from them," added the fund manager.

This can be done by buying/selling in the cash market but, according to the fund manager, it is likely that the underlying is being moved with synthetic futures and/or deep in-the-money (ITM) options.

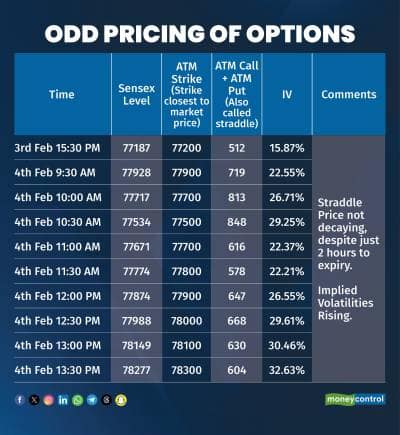

Fund managers draw attention to the ATM call + ATM put price for Sensex expiry on February 4. Options are supposed to decay over time as the finish line (or expiry time) draws close, and there is lesser uncertainty around expiry level. However in this case the ATM straddle price is higher than the prior day’s close right until 1:30 PM on expiry day. Then the Sensex moved 1.81 percent on February 4.

* IV: Implied Volatility

* IV: Implied Volatility

Just as there are violent expiry days, there are quiet expiry days. These are expiry days, “when option prices are half or lower than what they should be and these days are followed by absolute and unreal quiet in the market”.

How it all began

By January 2022, with leading exchanges introducing several contracts that had weekly expiries, there was an option contract expiring every day of the week. This led to a massive surge in volumes in zero days to expiry or 0DTE trades.

By June 2023, these fund managers started noticing oddities, which have become more severe in recent times. Chintan Dhruv, a fund manager, who graduated from IIT Bombay and IIM Calcutta where he was among the top five rank holders, says that quiet expiries came first, which people adapted to by selling options, then out-of-the-blue, violent expiries rocked the market. He goes on to explain how the initial set of violent expiries were first noticed on the least liquid indices but then they came to be visible on more liquid ones.

Over several months of witnessing quiet and violent expiries play out, with options getting exorbitantly expensive beforehand on violent days only to be followed by a steep move in the underlying, and vice versa for quiet days, slowly a theory began to emerge on the presence of a whale in the deep waters of Indian options.

Adding fuel to fire was a widely publicised court case between Jane Street Group and Millenium Management Global Investment Fund in April 2024 where the former accused two of its former employees of stealing a strategy and taking it to the latter. But what caught Indian traders’ attention was that Jane Street claimed to have made $1 billion from a strategy on Indian options in 2023.

The volatile expiries, with their sudden spikes in option prices, have been particularly hard to stomach, with retail option sellers scrambling to cover their positions and wiping out their capital in a matter of seconds.

What the fund managers are now openly adding is that there are also “quiet expiry days”, when the option premiums/prices get crushed abnormally and the underlying index then trades in a tight range even when other indices are seeing big moves. Quiet days would benefit an option seller.

Karthik P, Partner at Karna Stock Broking, a proprietary trading firm, does not want to say that there is a single or a group of manipulators in the market because he has no evidence for that, but he believes that the market activity is suspicious and needs regulatory scrutiny.

He does not even think that the manipulator, if there is one, is necessarily a big foreign hedge fund. According to him, it could even be a brokerage that knows that a big fund is placing a large cash-market order and is asking a related third party to take a position in the derivatives market to benefit from that.

Also read: Sebi mulls expanding investors pool for angel funds

Is Indian market more vulnerable?

Karthik, whose firm also tracks the US market, explained why Indian market has always been vulnerable to this kind of manipulation. Basically, India’s cash market is much shallower than its derivatives market, because the latter has massive volumes.

“The massive volumes in this segment is why SEBI has acted to cut down volumes in the derivatives market. It has always been like that but in the last four to five years, it has just increased dramatically… but the cash market did not grow in tandem.” In October 2023, a report from Axis Mutual Fund estimated that derivatives volumes then were 400x cash trading volumes; versus 5x-15x seen in other markets.

With cash markets being illiquid, you don’t need much money to move indices and, with derivatives markets liquid as gold, you can build large positions there .

Has the reduction in expiry days helped?

On October 1, 2024, the market regulator issued a circular to regulate index derivatives market and reduce speculative activity in this segment. One of the directives resulted in weekly expiry contracts being reduced to two a week or one per exchange.

Dhruv says that this has not reduced the risk; In fact some days there are even more exaggerated moves than before. “People fearing the manipulator are now afraid of selling options, leading to a less liquid market. The manipulator now has to buy options at even higher prices. This means that the manipulator needs to make even bigger moves in the underlying than before to profit from the bought options.”

“We have significantly reduced expiry day trading because one is only left guessing the nature of the expiry. Instead, we trade in contracts that have monthly expiries (since gamma is weaker when expiry days are further away). We have also reduced the capital deployed in the derivatives market by half,” said Dhruv.

Some of the largest moves on expiry days have indeed been post SEBI’s implementation of fewer expiries.

Sebi not Convinced ?

A fund manager has made a presentation to the Securities and Exchange Board of India (SEBI). Sources at the regulator said that SEBI is aware of these concerns and are constantly monitoring the market for any signs of manipulation. However, as a regulatory source said, “the claim (the fund managers’) is like saying that there is an elephant rampaging in the town centre, but we can’t see it”. It would suggest that the regulatory officials are viewing the concerns with scepticism.

Another fund manager said that all the regulator needs to do is check who is taking exposure to move the market and if related parties are taking positions in the derivatives market.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.