In his book 'One Up on Wall Street', the legendary fund manager Peter Lynch introduced the term 'diworsification' to describe companies' excessive diversification through acquisitions, often into unrelated businesses. Predictably, this led to substantial capital misallocation and destruction. Over time, the term has expanded to include over-diversification within an investment portfolio.

The concept of diversification, now firmly ingrained in the world of investing, is a fundamental element of Modern Portfolio Theory, initially formulated by Harry Markowitz in 1952. Diversifying across a variety of assets and stocks can reduce total risk, defined by volatility, while maximising the overall return in a portfolio.

Total risk has two components: Systematic risk and unsystematic risk. Systematic risk encompasses market risks that cannot be mitigated through diversification. This includes geopolitics, macroeconomic factors like recessions, inflation or interest rates—essentially, risks inherent in the market.

Unsystematic risks are specific to individual companies or sectors and can be reduced through diversification. Examples include risks associated with management, strategy, business models, financial structures and operational factors.

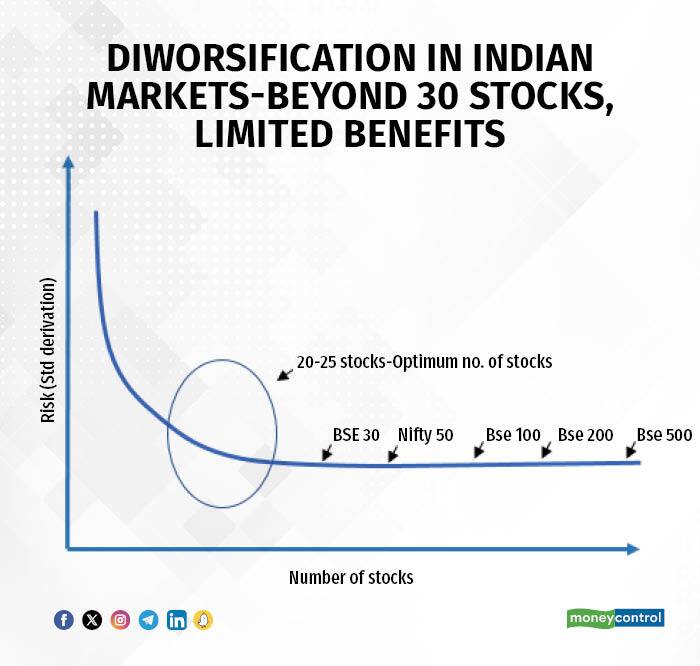

By including a mix of uncorrelated or less correlated stocks from various sectors or with different business models, one can reduce unsystematic risk as the number of stocks in a portfolio increases. Refer to chart 1 for an illustration of this concept, where total risk decreases as unsystematic risk diminishes with a rising number of stocks in a portfolio.

However, adding more stocks beyond a certain point does not further reduce risk and can lead to suboptimal investment decisions, lowering the expected return of the portfolio. The question arises: What is the optimal number of stocks to hold in a portfolio? When does 'diworsification' become a concern?

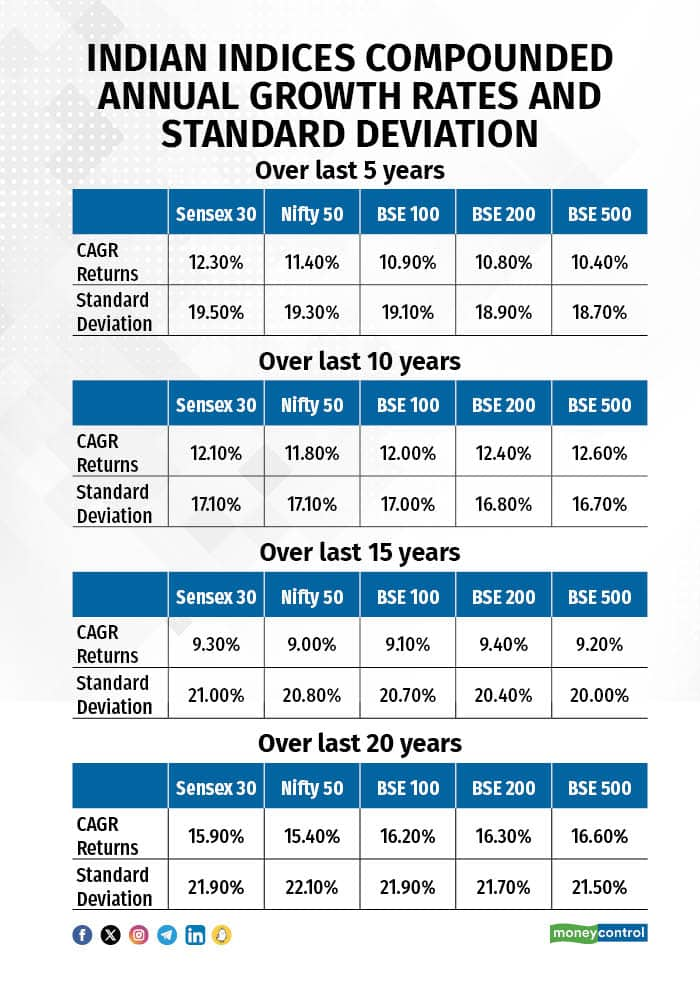

To answer this question, we analysed the returns and risk (standard deviation) of portfolios of different sizes over a 5-20-year period. For objectivity, we employed market indices—the BSE Sensex (a 30-stock portfolio), NSE Nifty (a 50-stock portfolio), BSE 100, BSE 200, and BSE 500.

Chart 2 displays the returns and risks of these portfolios over various time horizons. Interestingly, they all delivered nearly identical returns while assuming nearly identical risks. Going beyond 30 stocks clearly does not provide additional benefits, and holding fewer than 15 stocks increases concentration risk. We believe that an optimal portfolio should typically contain 20-25 stocks.

Chart 1: Diversification reduces Unsystematic/Stock risk…but only up to a point

Note: This is an illustrative chart, not on scale | Source: Avendus Olivo

Note: This is an illustrative chart, not on scale | Source: Avendus Olivo

Chart 2: Diworsification in Indian markets—Beyond 30 stocks, limited benefit Note: This is an illustrative chart, not on scale | Source: Avendus Olivo

Note: This is an illustrative chart, not on scale | Source: Avendus Olivo

Source: Bloomberg, Avendus Olivo, Data as of August 31, 2023. Above returns and standard deviation are based on daily price returns of the index for the respective period.

Diworsification = Lack of Focus

Maintaining a large number of stocks can dilute potential returns because the gains from a few successful investments may be offset by the poor performance of numerous underperforming ones.

Additionally, it increases the complexity of research and monitoring, demanding more time and resources. As the number of stocks grows, staying well-informed about each holding becomes increasingly challenging.

Diversification extends beyond the number of stocks in a portfolio; it also involves selecting the right mix of stocks. Achieving an optimal risk-return balance necessitates diversification across sectors, market caps, styles, themes, and trends.

Avoiding 'diworsification' applies to an investor's overall portfolio as well. We frequently observe investors with exposure to numerous Mutual Funds and Portfolio Management Service schemes (PMSes), resulting in exposure to a large number of stocks overall. Investors must also be aware of the 'overlap' between funds and schemes to prevent investments in highly correlated products. In a time when the Indian investment landscape appears promising, consolidation is imperative. Beware of 'Diworsification'.

Tridib Pathak, Executive Director and Portfolio Manager at Avendus Olivo PMS, possesses over three decades of experience in managing listed Indian equity assets for both domestic and offshore funds. He currently heads the long-only portfolio at Avendus Asset Management.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.