The year 2024 has been one of global uncertainty, with geopolitical tensions—ranging from the ongoing Ukraine crisis to conflicts in the Middle East—shaping the economic landscape. Major elections in key democracies like India’s recently concluded Lok Sabha elections and the upcoming polls in the US have added to the volatility. Yet, amid these disruptions, India has shown remarkable resilience. With a targeted growth rate of 7 percent and minimal currency fluctuations, India remains an attractive destination for both foreign and domestic investors.

As the country’s financial markets reach new milestones, the sophistication of its investor base is also evolving. Many are now turning to more complex financial products, such as Alternative Investment Funds (AIFs), seeking both diversification and exposure to niche assets. Over the past three years, AIFs have achieved a compound annual growth rate (CAGR) of 32 percent, underscoring the robust demand for these non-traditional investment vehicles.

AIFs offer a gateway to investments across venture capital and private equity, to hedge funds, real estate, pre-IPO opportunities, and various debt instruments. Their ability to invest in both listed and unlisted equities, along with innovative debt products, has made AIFs a vital tool for portfolio diversification and delivering superior returns.

Rising star

One of the standout categories within AIFs is private credit, which presents a distinct risk-reward profile compared to traditional debt instruments. As banks and traditional lenders focus more on high-rated corporate and retail loans, private credit is stepping in to fill a crucial gap, providing mid-market and emerging companies with much-needed financing.

In 2023, the value of private credit deals surged almost 40 percent to over $8 billion from $6 billion the previous year, while the number of deals rose from 77 to 108, according to an EY report. This trend has accelerated in 2024, with private credit deals reaching a record high of $6 billion across 96 deals in just the first half of the year.

The growing demand for private credit is driven by the need for flexible, non-traditional financing solutions. Many of these businesses have strong growth potential but lack the collateral or credit ratings required by conventional lenders. Such companies can turn to private credit for tailored capital solutions that align with their specific financial needs, including availing of non-dilutive capital. AIF investments across categories as on March 31, 2024, touched ~$50 billion, according to a SEBI report.

This is expected to double in the next five years. The reason for such growth stems from the possibility of private credit extending to situations such as debt to performing credit and distressed and special opportunity trades, spanning multiple sectors, capital structures, and end-uses.

The current fiscal not only witnessed a few big-ticket deals (such as KKR, ADIA in Reliance Logistics and Warehousing, investment by Zeal Global & SC Lowy in GMR Highways, Nimmagadda Prasad’s debt raise of $293 million, etc.) but also a significant number of small-ticket investments in mid-market companies (Incred’s investment in Whizdam Finance, BPEA Credit’s funding of mPokket Financial Services, and Modulus Alternatives and Incred’s financing of Fourth Partner Energy).

The increasing reach of private credit, from large companies and highly complex trades to mid and emerging companies, is a sign of its higher acceptance. The recent fundraise by domestic and global funds such as Edelweiss ($1.3 billion Special Situations Fund), Kotak ($170 million performing credit fund), and BPEA ($90 million performing credit fund) is evidence of growing demand for private capital in India.

Risk-return dynamics

Private credit typically delivers superior returns, frequently outperforming traditional fixed-income products. Whether it's plain debt, structured debt, or equity-linked instruments, the flexibility of private credit makes it an attractive option for companies. Meanwhile, for investors, the value lies in its risk-reward proposition. Returns can range from coupon-based payments and event-linked returns, to equity upsides and back-end premiums.

The internal rate of return (IRR) in performing credit is in the range of 14-16 percent. In more complex situations, such as distressed funding or rescue financing, the IRR is 18 percent and above.

However, higher returns come with proportionate risks. These risks primarily stem from the credit profiles of investee companies, market conditions, and the underlying deal structures. To navigate these challenges, private credit funds employ rigorous risk management strategies.

Unlike banks and non-banking financial companies (NBFCs) which manage extensive loan books, private credit funds typically focus on smaller portfolios, often overseeing just 8-10 active investments at a time. This enables closer monitoring and hands-on management of each asset. Risk management is further reinforced through term sheets, cash-flow ring-fencing, third-party monitoring, and flexible structuring with collateralisation, or equity-linked payouts.

Alternative to traditional investment products

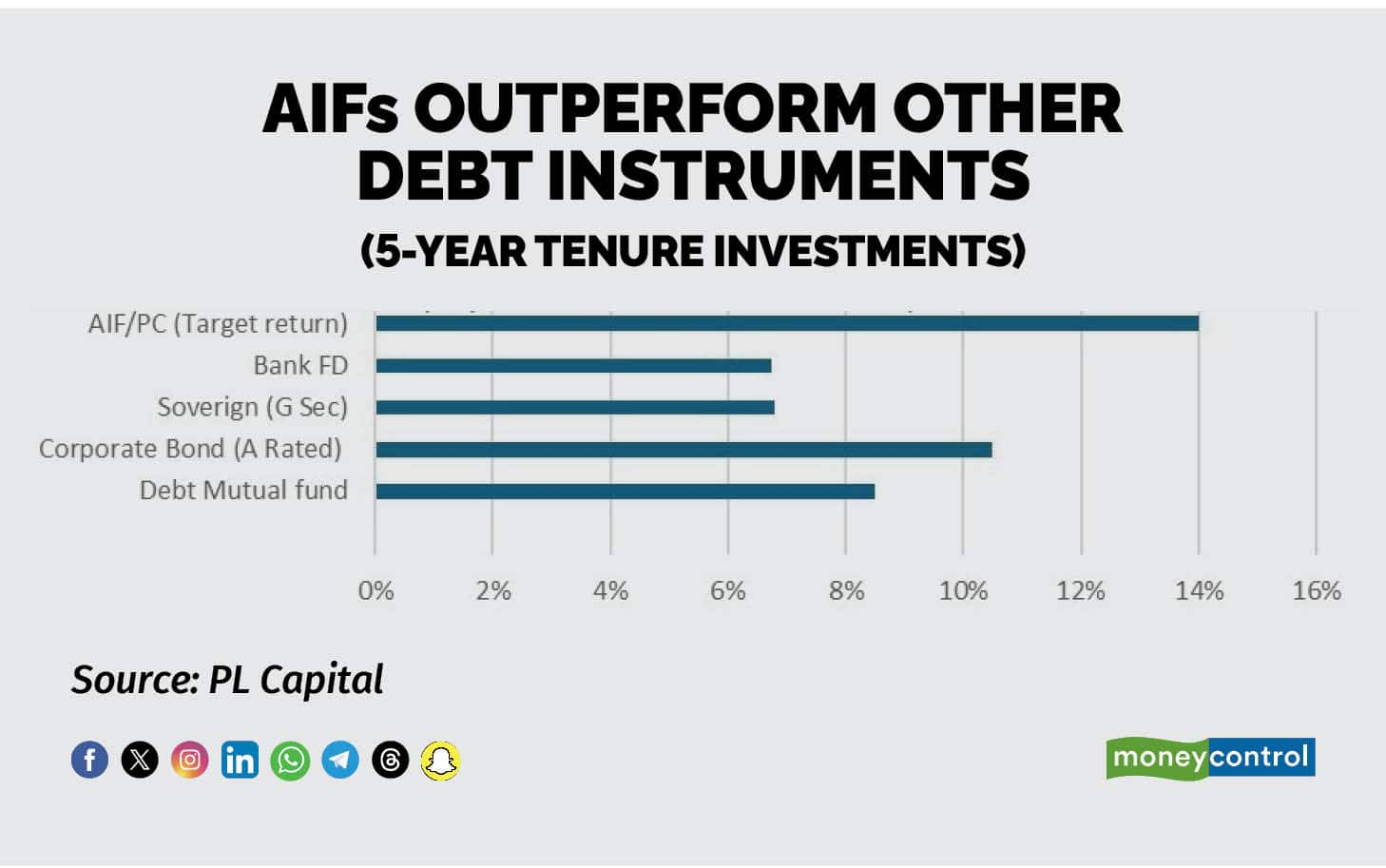

Unlike traditional fixed-income products like bonds or debt mutual funds, private credit typically offers IRRs that are 4-6 percent higher, creating a more attractive risk-reward dynamic. Additionally, the removal of indexation benefits from debt mutual funds in 2023 has made traditional debt products less attractive to investors, further bolstering the case for private credit.

In this scenario, a structured product like private credit serves as a compelling alternative for investors seeking higher returns, strong risk management, and diversification within their fixed-income portfolios. Indian investors have traditionally favoured equity as an asset class since it has outperformed the rest. As per an NSE report of July 2024, the Nifty 50 TR index had delivered 15.3 percent returns (with a volatility of 19 percent) for the five-year period ending on March 31, 2024.

Considering the above, private credit, in particular performing credit, can be a strategically important product in an investor’s portfolio since the returns are generated by investing in performing companies with demonstrated earnings, and with lesser volatility. Considering India’s valuation premium (P/E) and RoE gap, which is currently the highest among emerging markets, and a market cap / GDP ratio of ~1.4, fundamentally priced credit (credit that's priced to match the risk)allows investors to balance their allocation in assets other than equity.

Not surprisingly, private credit funds are attracting a growing range of investors—from UHNIs and HNIs to family offices and institutions. This burgeoning market is set for expansion, fuelled by a supportive regulatory landscape, improved corporate credit quality index, maturing wealth and family office management, increasing institutional participation, and enhanced transparency.

(Kapil Sachdeva is Senior Vice President and Credit Head – PL Alternatives, PL Capital Group)

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.