")

Krishna KarwaMoneycontrol Research

Kewal Kiran Clothing (KKC) reported a subdued set of numbers for the March quarter and ended the year on a tepid note. Given the intense competition in a largely commoditised business, the prevalence of discounted offerings from online portals, and few entry barriers in the segment, we do not see the possibility of any early turnaround.

Despite it being a well-run company, the myriad industry headwinds give rise to caution and we believe investors would be better off avoiding its stock.

KKC deals in garments for men and women through four brands - Killer, Easies, LawmanPg3, Integriti. The company’s products include jeans, formals, semi-formals, casuals, and accessories. Retailing is done through exclusive and multi-brand outlets, large format stores, and e-commerce.

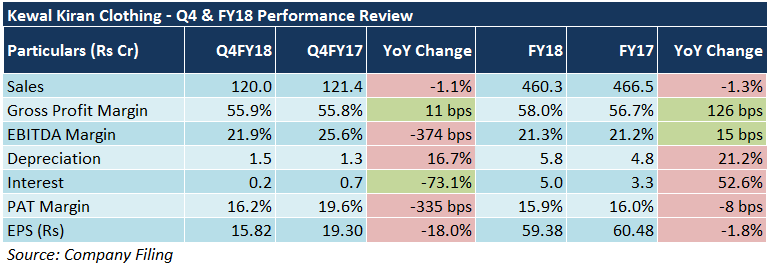

In the quarter gone by, despite a low base (demonetisation impacted Q3 and Q4 of FY17), KKC reported a rather weak set of numbers. The company’s Q4FY18 margins were impacted mainly on account of a de-growth in revenue and a steep year-on-year (YoY) increase in employee expenses.

In terms of brands, revenues from Killer, which accounted for 53 percent of KKC’s FY18 turnover, grew by only 2 percent YoY. Lawman and Integriti, which constituted 17 percent and 21 percent of the company’s FY18 sales, respectively, witnessed a sharp decline of 12 percent and 11 percent YoY.

Should you invest?

Although KKC’s financials have been consistently healthy, problems pertaining to sluggish revenue growth continue to persist. The company’s policies have been conservative in comparison to its peers, who are investing aggressively in business integration (backward and forward), product launches, branding, and market expansion.

Since KKC’s products are essentially commoditised, risks stemming from high input (cotton) costs are also quite significant. This is because it is hard to pass on such price hikes to customers when there is little or no brand loyalty. Extension of the end-of-season sale leads to lower realisations, which, in turn, may dent profit margins.

KKC’s augmented retail presence across multi-brand outlets, large format stores, national chain stores, and online portals failed to yield incremental sales during FY18, when compared to FY17. Since the company derives nearly 80-90 percent of its revenue from these platforms, this issue ought to be addressed.

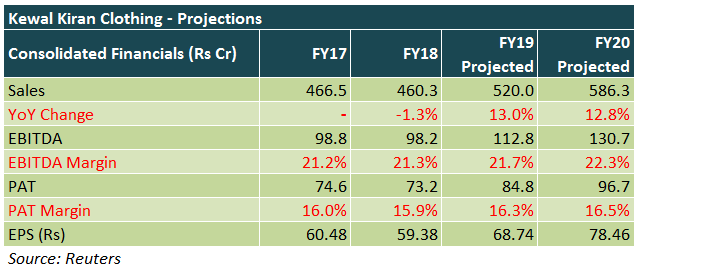

The stock has corrected pretty significantly over the past three months and is currently trading at 20.4 times FY20 projected earnings. Although its valuation doesn't seem too demanding, the outlook remains subdued. Investors looking to participate in a growth journey should avoid this stock.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.