Mamaearth has a tendency to be the first off the block. It was the first unicorn of 2022. Now, it is going to be the first unicorn to offer an IPO in 2023, actually the only one to do so in over 18 months.

As it is also going to be the first digital-first D2C company to go the public route, Bombay Shaving Company Founder, Shantanu Deshpande, believes its reception by investors will determine the fate of its other venture-funded peers. If the string of firsts wasn't enough, some of its earliest investors are sitting on 100X returns at the top end of the IPO valuation.

But, all’s not hunky dory. At a time when investors are searching for islands of profitability in the new age sector, the Sequoia-backed unicorn saw itself slide into the red in FY23. It has kept its valuation flat compared to its last round of funding, yet appears to be pricier than well-entrenched peers. Advertising costs are rising at a fast pace. And, its reliance on new launches for incremental revenue is increasing.

ALSO READ: Mamaearth open to exploring tactical and strategic opportunities to outgrow markets: CEOMeanwhile, social media posts are trickling in about why the IPO might not pop. After the company mopped up Rs 765 crore from anchor investors and employees oversubscribed their portion, retail investors gave the fundraise a slow start on Day 1.

With the noise around Mamaearth's debut expected to rise over the next few days, here are seven things about the D2C unicorn you must not miss.

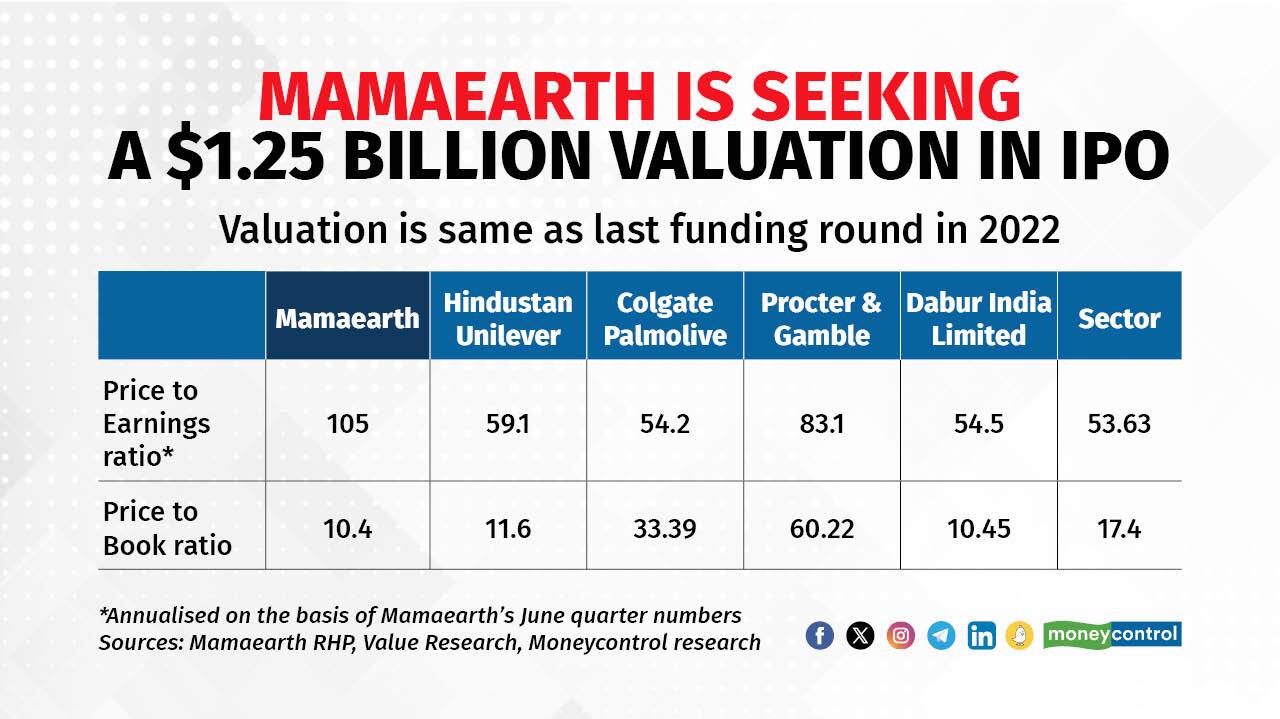

Valuation conundrumAfter a controversy earlier this year when Mamaearth’s founders rubbished reports that it was seeking a valuation of over $3 billion, the company has priced itself at around $1.25 billion (or Rs 10,423 crore). It is a flat valuation compared to the $1.2 billion the company commanded in 2022 when it had become the first unicorn of the year.

Further, the stock is being valued at a P/B ratio of 10.454 times, compared to its peers' average P/B of 17.4 times, according to Value Research. However, concerns remain on the pricing front as the valuation being sought is over 105 times the company’s annualised FY24 earnings (based on a net profit of Rs 24.7 crore in the June quarter).

"The average P/E ratio of our competitor entities (which are listed companies in India that are of larger size with longer operating histories and varied business models and offerings, that operate in the fast-moving consumer goods space, including the BPC segment) is 53.63," Mamaearth said in its red herring prospectus.

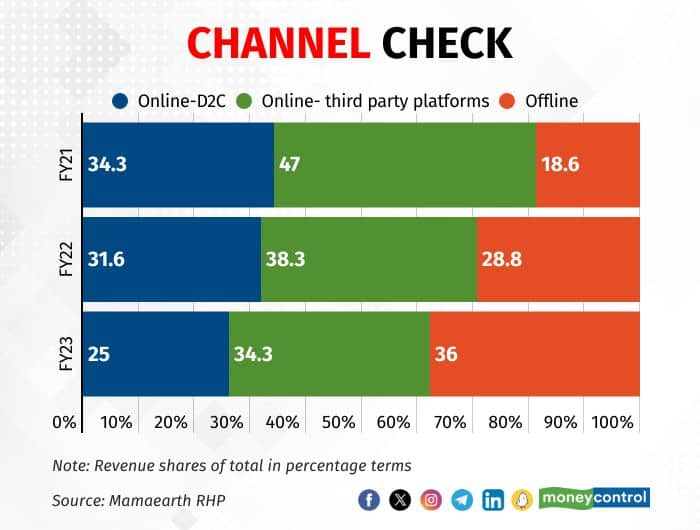

Mamaearth’s sales from its own websites and apps are decreasing as a portion of total online sales. While D2C sales constituted 46.73 percent of overall online sales in the June quarter of FY23, this share dropped to 35.65 percent in the corresponding period of FY24.

At the same time, Mamaearth’s reliance on third party e-commerce marketplaces like Amazon and Flipkart is increasing for online sales, although it is decreasing overall with its offline foray. The share of online sales from such marketplaces rose from 53.27 percent to 64.35 percent during this period. However, the commissions and fulfillment charges paid to third party platforms for these sales have flatlined at just over 27 percent during the period.

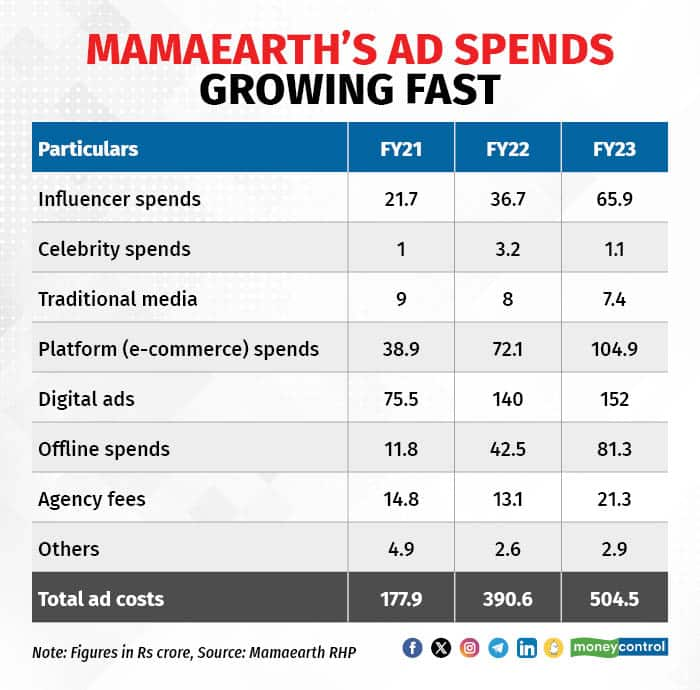

Mamaearth's advertisement expenses as a percentage of revenue from operations was 35.52 percent in FY21, 41.49 percent in FY22, 38.68 percent in FY23, 34.99 percent in Q1 of FY23 and 41.33 percent in Q1 of FY24 on consolidated basis.

While most of the ad spends till now have been online on influencers and e-commerce platforms like Amazon and Flipkart, the company’s increasing focus on offline sales means that it will have to ramp up its ad spends on traditional media.

Of the Rs 182 crore of IPO proceeds that Mamaearth intends to spend on ads over the next 4 years, the lion’s share of Rs 150 crore is expected to be for television campaigns, according to its red herring prospectus.

At the same time, as the company’s reliance on third party marketplaces for sales is rising and the platforms are focussing on increasing their own profitability, Mamaearth is having to spend more on ads on these platforms. As a share of revenue from platforms, Mamaearth ad spend on this channel increased from 8.23 percent in Q1 of FY23 to 10.44 percent in Q1 of FY24.

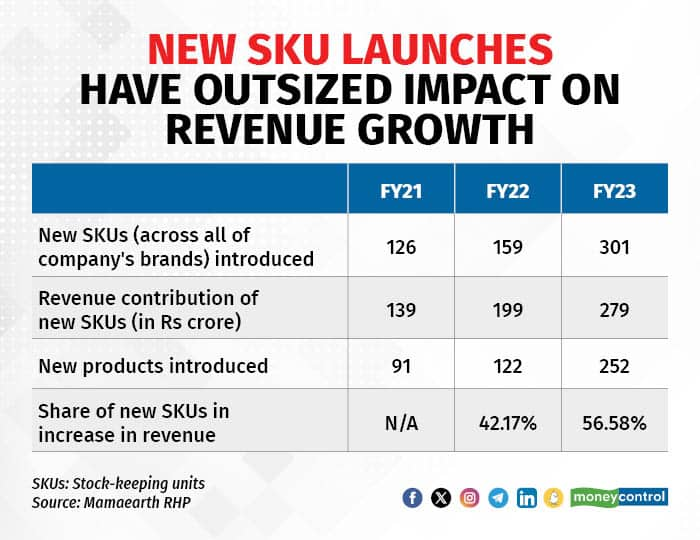

As is typical of consumer brands, the growth of Mamaearth’s topline is reliant on the launch of new products. While 159 new stock-keeping units (SKUs) accounted for 42 percent of the increase of its revenue in FY22, the dependence grew to 57 percent in FY23.

Mamaearth’s revenue from offline channels were 18.63 percent of the total in FY21, 28.87 percent in FY 22 and 36.14 percent in FY 23. For Q1 of FY22, ending June 30, revenue from offline channels was 31.90 percent and for the same period FY 23, it was 33.47 percent.

With the offline share of revenues in an upward trajectory, Mamaearth is increasingly competing with the likes of HUL, P&G, Dabur and Reckitt on their territory. This is expected to demand more operations and advertising resources to be spent on the ground with the deep-pocketed incumbents.

ProfitabilityIt’s an evergreen debate whether or to what extent digital-first D2C brands should be valued as tech companies. One of the reasons that companies want to talk about being ‘tech’ is investors are attracted to the economies of scale that tech can deliver — so the costs associated with each incremental sale keep decreasing and margins keep going up.

Mamaearth is no different — its red herring prospectus mentions the phrase ‘economies of scale’ no less than 13 times.

The company says, “As our business scales, we intend to proactively work towards deriving further benefits of economies of scale across all aspects of our business model, including procurement and manufacturing, supply chain and distribution, advertising and promotional expenses, and operating expenses.”

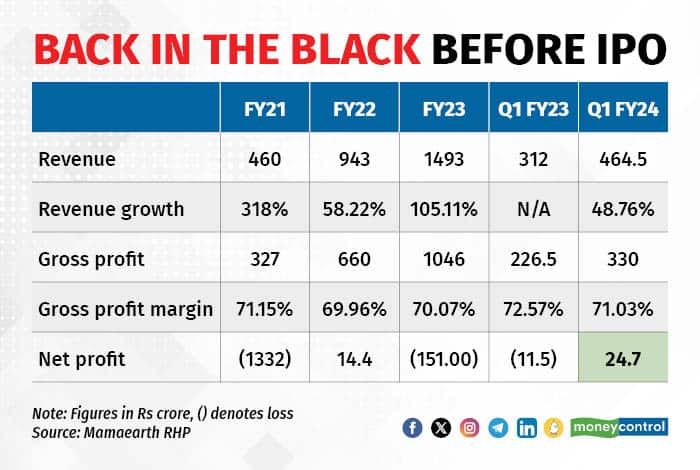

Between financial years 2022 and 2023, the company's gross profit margins increased by 0.11 percent from 69.96 percent to 70.07 percent, respectively. This, the company argues, was driven by economies of scale which has contributed to lower procurement costs, specifically for key ingredient ranges such as onion and ubtan for its flagship brand.

The bottomline is yet to reflect any economies of scale. The company saw a net loss of Rs 151 crore in FY23, net profit of Rs 14 crore in FY22 and net loss of Rs 1,332 crore in FY21.

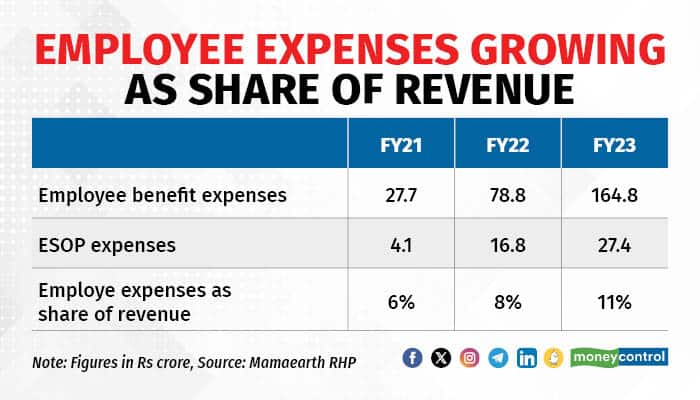

Employee benefit spending as a percentage of revenue has been on the rise — it was six percent in FY21, eight percent in FY22 and 11 percent in FY23. However, Mamaearth seems to have been trying to rein in this cost recently as the metric dropped from 12 percent in the June quarter of FY23 to 9.5 percent in the same period of FY24.

Also, employee costs have risen almost 6X between FY21 and FY23 – over the same period, revenue has grown 3X.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.