Jupiter and Fi, two of India’s leading neobanking platforms, compete fiercely in the market but have one thing in common: Federal Bank. The bank serves as the backbone for these fintechs, which provide it with a technology interface.

Federal Bank has been expanding its fintech partnerships across services at a scorching pace, with 50 tie-ups at last count. The long list of tie-ups and Federal Bank’s keenness to continue adding fintech partners has made many wonder: how many is too many?

In a post-earnings conference call, Federal Bank CEO Shyam Srinivasan set the record straight. Srinivasan reasoned that the bank would have had to open 2,000 branches -- something that would have required a lot of investment, time and effort -- to achieve the same growth in the absence of these tie-ups.

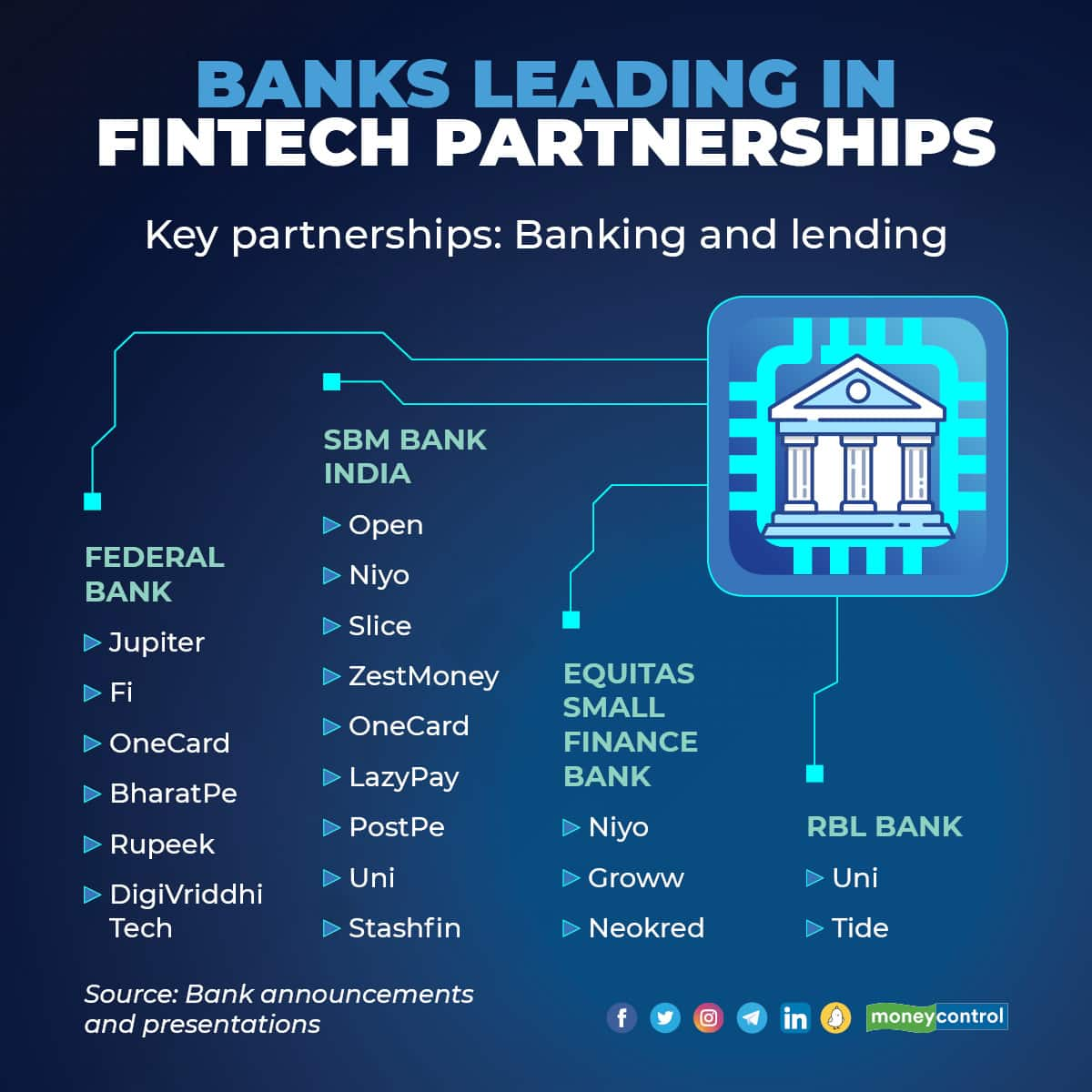

Federal Bank leads in the number of partnerships with a host of startups. But, other small banks such as Equitas Small Finance Bank, State Bank of Mauritius India, RBL Bank and many others share Srinivasan’s view and are looking at fintech partnerships as a business model.

The idea is to reach a scale that is, if not equal, closer to many larger banks. These banks have tie-ups across fintech verticals such as neobanking, prepaid cards/Buy Now Pay Later (BNPL), credit cards, payment gateways, merchant payments and SME lending.

Sharper focus

While such partnerships have grown over the past few years, banks are now looking at the model more seriously than ever. A testament to this is that many banks have now formed departments to focus solely on fintech partnerships, and set certain internal targets.

According to Rakesh Pozath, Partner - Financial Services at Bain & Company, “Everyone understands that the future is embedded finance. Meaning, you cannot expect your customers to come to your digital platforms for everyday banking needs. You have to be present where they go, where they shop, where they transact.”

For banks, the online presence and easy interface of fintechs helps gain customers across deposits and lending. Fintechs earn through fees and commissions across banking services and small-ticket loans.

We take a look at why these partnerships work for the banks and how the landscape is likely to evolve over the next few years.

Branch light, fintech heavy

Partnerships are a faster and cheaper way for banks to onboard more customers. Banks with a regional focus, such as Kochi-headquartered Federal Bank or Thissur-headquartered South Indian Bank, can now have customers across the country without investing in a large branch network. Banks would otherwise have to invest crores in infrastructure and staff on a new branch, depending on the city and locality

Until 2015, Federal Bank’s strategy was to expand its branch network. But as digitisation swept the country post-demonetisation, the bank changed its approach.

In a conversation with Moneycontrol late last year, Federal Bank Executive Director Shalini Warrier, who leads these tie-ups, said: “The bank’s strategy on distribution can be encapsulated as “branch light, distribution heavy”. We have expanded distribution through collaboration with fintechs and today, we have a team focused on providing the best of services to our multiple fintech partners”

Similarly, State Bank of Mauritius India, too, has an asset-light model with just eight branches across six cities. The bank has chosen partnerships as the mode for retail customer onboarding and growth. The bank declined to comment when Moneycontrol reached out.

State Bank of Mauritius India has a large number of tie-ups across lending and BNPL fintechs, including Slice, ZestMoney, OneCard, LazyPay, PostPe and Uni. It has also partnered with neobanking platform Niyo, a partnership that it has in common with Equitas Small Finance Bank.

Commenting on State Bank of Mauritius India, a fintech founder said, on condition of anonymity: “Newer banks have an advantage of a newer technology architecture. Secondly, they are small, so they’re nimbler. For them, these partnerships are easy to work out.”

Strong growth

In terms of numbers, 75 percent of Federal Bank’s new accounts originate through these tie-ups and it has added 12 lakh customers through partnerships with Fi and Jupiter. Over 3.5 lakh accounts are opened each month. Current Accounts and Savings Accounts (CASA) deposit balances in these accounts grew three times in just the third quarter of FY22.

In the same quarter, the bank saw 7.7 times growth in credit cards issued in partnership with FPL Technologies’ OneCard, with over 81 times growth in spends by customers.

Equitas Small Finance Bank has opened over 10 lakh accounts through its partnership with Niyo. As of December 31, 2021, over 2,000 fixed deposit accounts were opened in partnership with investing platform Groww. Accounts opened through the bank’s fintech tie-ups amount to 40 percent of the bank’s total accounts. These two banks specifically are transparent about how they gain from these partnerships while serving as a backbone for many fintech startups.

“For those that have turned into small finance banks (SFB) from being microfinance institutions (MFI) earlier, the biggest challenge was to mobilise deposits. What proved a success for SFBs was partnerships with fintechs. Fintechs have access to the premium customer segment that prefers apps for banking and investing,” explained Jaikrishnan G, Partner and Head of Financial Services Consulting at Grant Thornton Bharat.

He added, “For smaller banks, their current network and infrastructure cannot meet the demands of evolving customer behaviour to venture into newer products and segments on their own. Fintech partnerships come in as a handy enabler to package their proposition with a new-age factor.”

Choosing partners

The key for banks is choosing a few partnerships that give the best results. While Federal Bank has 50 partnerships overall, only four or five key fintechs help get in customers; the rest are technology-enabling partners. For Federal Bank the important names are Jupiter, Fi, OneCard and BharatPe, which is a merchant acquisition funnel.

RBL Bank, which is the fifth-largest credit card player in India, has tied up with Uni to expand card issuance in the prepaid cards space.

Parool Seth, who heads RBL Bank’s New Economy vertical, among others, explained: “If you look at the industry, there are pockets of products that banks are building on and they are developing that expertise. You have to choose a few partnerships and make sure that those attain a certain depth over time so that it's beneficial to both the fintech and the bank.”

Banks approach fintechs based on certain philosophies and commonalities in an environment where the Reserve Bank of India (RBI) is increasingly delving deeper into how new and innovative products stack up in terms of regulatory compliance.

“There is an elaborate due diligence process. We look for expertise in technology and digitisation, the architecture of the business, founders’ credibility and a background check, and the funding available to them. For most partnerships, banks and fintechs look at what is in it for them. But we look at what is in it for the customer,” said Murali Vaidyanathan, Country Head for Branch Banking, Products, Liabilities, Digital and Marketing, at Equitas Small Finance Bank

Fintechs too see partnerships as a strategic meeting of minds and values.

“We worked with Federal Bank first because we found that they were very focused on the consumer experience of the user and ready to invest in building new APIs that would actually fit for the user from an open banking perspective,” said Fi co-founder Sumit Gwalani. “They have been extremely earnest towards making the consumer experience better. This has also been our focus and hence our wavelengths match and it fits perfectly.”

Where is the line?

Banks see partnerships with fintechs continuing as a natural business model. But with a large number of tie-ups, how many are too many? Currently, banks seem to be forging ties where they see the right fit, despite a large number of these startups having begun operations only in the past few years, and just last year in some cases.

“Ever larger banks and PSU Banks are open to partnerships,” said the founder mentioned earlier. “Partnerships have become a business model now, it’s no more an experiment. But, in two to three years’ time, banks will start evaluating which partnership is contributing how much and there will be a natural selection process.”

“Partnerships will remain for a while because building all the tech stacks in-house takes time for banks. The ability of these partnerships to acquire is phenomenal. As long as there is value creation on both sides, this game will continue,” added RBL Bank’s Seth.

While the entire financial services landscape is dotted with startups today, with time, the fintech ecosystem itself is expected to see some amount of consolidation. Either that, or banks themselves will look at the top players in each vertical, according to industry experts. In every debate around fintechs, the arguments are in favour of scale. The ones that scale will survive longer.

“Every fintech has a fixed cost that goes towards compliance because we function in a regulated environment. Therefore, if fintechs don’t scale, it is cumbersome for the bank and these fixed costs become a problem. That is why you will see that fintechs that don’t scale will be culled by the banks at a certain point,” said another founder.

This is similar to what happened with payments – the offering that serves as the first point of contact to bring customers on to digital platforms. While a large number of banks and apps offer UPI, only three players rule the market – PhonePe, Google Pay and Paytm Payments Bank make up around 95 percent of the monthly volumes.

Speaking on condition of anonymity, a banker said: “Every fintech wants to offer some new product that may or may not have a future. So, there will be some consolidation, and larger fintechs that have the ability to innovate and prove themselves on customer acquisition will survive.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.