Madhuchanda Dey

Moneycontrol Research

Kotak Mahindra Bank (KMB) ended FY18 on a strong note with a picture perfect execution. Business growth has resumed and given the superior liability franchise and adequate capital, market share gains will only accelerate in the future. Its asset quality picture has improved further. The bank is ideally placed to capitalise on financialisation of savings in India, given its strong presence in broking, asset management and insurance. With a savvy management steering the group and strong outlook for the individual businesses, it looks to be in a vantage position. While the valuation prima facie looks expensive at 4.3 times FY19e book, we feel the potential of subsidiaries is still not fully captured in the price.

Group profitability driven by capital market businesses, asset management and insurance

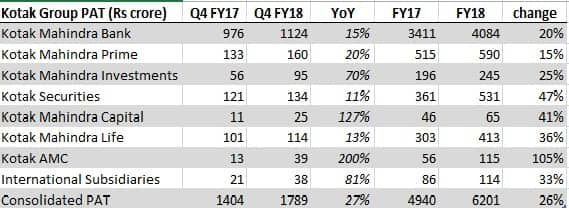

A peek into the quarter suggests that the 27 percent growth in group’s profitability was contributed by the bank as well as its subsidiaries. Of this, strong growth was posted by Kotak Mahindra Investments, Kotak Mahindra Capital, Kotak AMC and its international subsidiaries.

Subsidiary performance at a glance

Source: Company

Full year consolidated profit growth of 26 percent was led by capital market and asset management subsidiaries. This indicates that financialisation of savings is clearly having a positive rub off on the group.

A solid quarter

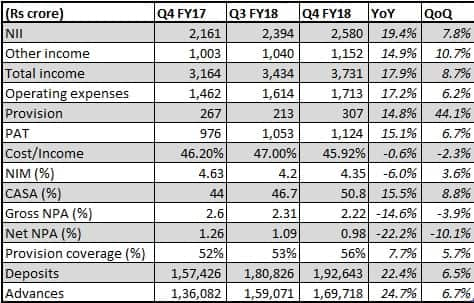

KMB delivered a steady performance in Q4 FY18. After-tax-profit growth of 15 percent year-on-year (YoY) was supported by a 19.4 percent YoY growth in net interest income (difference between interest income and interest expenditure), 15 percent rise in non-interest earnings driven by a 33 percent surge in core fees and 15 percent YoY growth in provision that reflects the underlying strength of its asset quality. The rise in operating expenses was due to a Rs 82 crore provision on account of increase in gratuity ceiling. Without this ad hoc cost head, the bottomline of the standalone bank would have grown by close to 21 percent. Net interest margin (NIM) rose sequentially.

Quarterly snapshot

Source: Company

Asset quality: As good as it gets

Asset quality showed no signs of stress with gross and net NPA figures declining sequentially and SMA2 (special mention accounts) falling to 0.04 percent of total advances at Rs 72 crore.

Growth making a come back

The bank is an extremely well-capitalised entity (capital adequacy ratio of 18.2 percent) and is steadily but carefully pushing the growth pedal. Advances grew 25 percent YoY in Q4 FY18. It now commands a 4.2 percent share of all incremental advances in the sector. Growth was broad-based with most segments, except business banking, contributing. Muted performance of the banking business has been a conscious decision as the management is still wading through the waters cautiously in light of the changing competitive landscape in the SME (small medium enterprises) segment post implementation of the Goods & Services Tax (GST).

Source: Company

In a hyper competitive lending landscape, the management is able to compete thanks to the robust liability profile it is steadily building. The ratio of low-cost deposits at the end of the quarter stood at 50.8 percent. The bank commands a 4.9 percent share of system deposits and has been growing its customer base and low cost deposits at a fast clip with the help of its various digital initiatives.

Source: Company

Building solid businesses outside the bank

KMB has shared details of its relatively small but growing life insurance business in which it now holds entire stake. Based on the key parameters shared, our calculation suggests that the insurance business itself would be valued upwards of Rs 26,000 crore, or Rs 138 per share.

Value KMB’s stake in life insurance business at Rs 138/share

The capital market-linked businesses have also been delivering strong growth. Kotak Securities, for instance, has a market share of 8.5 percent in the cash segment and its profitability has grown 47 percent YoY in FY18.

Total assets under management of the group has risen 29 percent YoY for the year at Rs 182,519 crore. Kotak Asset Management Company has improved its overall FY18 market share to 5.36 percent versus 4.68 percent in FY17 and also improved its equity average assets under management (AAUM) market share to 4.63 percent versus 3.67 percent for FY17.

On the wealth management side (housed under the bank), it has built a formidable business and caters to 40 percent of India’s top 100 families with a relationship value of Rs 2,25,000 crore.

Going forward, as these non-banking businesses assume higher share of consolidated profitability (the bank still contributed 68 percent in FY18), investors may see a valuation upside emanating from the consolidated business. Seen in this context, its valuation at 4.3 times FY19 book does not appear too expensive. Hence, long-term investors should consider KMB as a core high quality holding in their portfolios with a steady growth prospect.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!