Neha Dave

Moneycontrol Research

Highlights

-Indostar transforming from wholesale financier to a diversified lender

-Acquired IIFL’s CV portfolio

-Incremental loan growth was driven by retail assets

-Asset quality has been resilient so far but remains vulnerable-Healthy earnings profile; compelling valuations

-----------------------------------------------------------

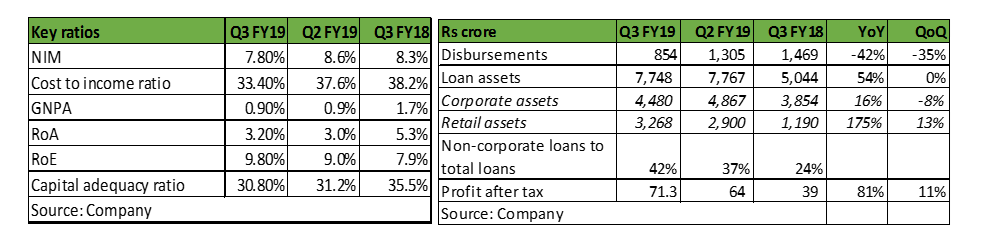

Asset financing non-banking finance company (NBFC), Indostar Capital Finance, reported mixed third quarter performance. A decline in credit costs and improving operating efficiency helped profit grow 81 percent year-on-year (YoY) despite a slowdown in disbursements and margin contraction.

In a separate release, Indostar announced the acquisition of commercial vehicle finance business of IIFL Finance. The acquisition includes the entire CV finance assets of Rs 3,949 crore, along with 1,337 employee team located in 161 branches spread over 18 states.

The acquisition is in line with management’s strategy to grow non-corporate book and will increase Indostar’s total asset book to Rs 11,697 crore from Rs 7,748 crore. Retail assets will be 62 percent of total assets.

Indostar’s stock has fallen sharply since end-September following liquidity concerns that engulfed the NBFC sector. Valuation has turned enticing, making it worth consideration.

Key positives

While overall assets under management (AUM) was flat, retail AUM segment grew 13 percent sequentially. This was offset by a de-growth of 8 percent in corporate book. Primarily a wholesale financier, Indostar forayed into SME, vehicle and housing finance to de-risk its loan book. The result of the diversification strategy is clearly evident in the changing mix of its Rs 7,748 crore loan book. Non-corporate loans now constitute 42 percent of the loan book as at December end from 24 percent a year ago. In fact, 67 percent of disbursements in Q3 was toward three focused retail segments.

Indostar’s asset quality has been resilient so far with overall gross non-performing assets (GNPA) of 0.9 percent as of end-December.

Having said that, the lender’s real estate exposure to the tune of 32 percent of its asset book is a contentious issue in the current environment and remains susceptible to cyclical downturns in real estate. However, we draw comfort from prudent risk management and the increasing proportion of retail loans which will bring more granularity to the loan portfolio in the medium term.

Despite scaling up of retail infrastructure (distribution network), the lender reported improvement in operating efficiency with cost-to-income ratio declining to 33.40 percent in Q3 as compared to 38 percent in the same period last year. This was possible because of gradual expansion as management intends to open more branches only after achieving breakeven in newly-launched branches.

Indostar reported healthy earnings profile with return on assets (RoA) of over 3 percent aided by fall in cost-to-income ratio and lower credit costs.

Thanks to the IPO in May that brought capital of Rs 700 crore, Indostar’ overall capital adequacy ratio (CAR) is healthy at 30.8 percent as of December 2018. A large quantum of equity gives it an edge over peer group in raising funds, though currently, it has depressed its return on equity (RoE) to below 10 percent.

Key negatives

Net interest margins (NIMs) fell to 7.70 percent, a decline of 80 bps sequentially. This was due to the higher cost of funds following tighter liquidity conditions. The company also witnessed softening of yields as it forayed into low margin products like housing finance.

Other observations

The lender has Rs 200 crore exposure to Essel group against which it has Rs 350 crore worth of shares of Zee Entertainment.

Outlook

Currently, Indostar’s market cap is less than its Q3FY19 net worth. The risk-reward is extremely favourable with the stock currently trading below FY20 estimated book value. The limited history of the company and sectoral concerns have made investors jittery. However, the stock’s current valuation is compelling, pricing in most concerns making it a worthy long-term bet.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!