India's software developers are betting big on learning all the nuts and bolts about the fast-emerging blockchain technology. The country is home to the second most number of blockchain developers in the world with nearly 19,627 developers, according to a market analysis carried out by Dappros, a London-based blockchain consulting firm.

In fact, India is second only to the United States, which has 44,979 blockchain developers as of October 24, 2018.

The India figure may be higher as the data collected by Dappros is mainly based on information from open sources such as LinkedIn. It does not account for developers whose social network profiles are not accessible.

Same goes true for developers in the US.

Read — India to be one of the world's blockchain leaders by 2023: Survey

A large number of blockchain developers in the country would mean that India may get an edge over other countries when it comes to developing applications based on Blockchain or improving applications through the technology.

But why choose blockchain technology? Something whose popularity can be attributed to the rise of cryptocurrencies - which itself remains marred with controversies.

The technology itself, apart from being used by cryptocurrency firms, finds use in multiple fields such as credible database management, government programmes and at several steps in the supply chain management.

Before we look at the uses of blockchain, let us understand how this technology works.

How does blockchain technology work?In a blockchain technology-based network, if someone requests for a transaction or tries to access some information, that request is broadcast on a peer-to-peer (P2P) network consisting of computers, known as nodes.

The network of these nodes validates the transaction, which can involve cryptocurrency, contracts, records or other information, and the user's status using a known algorithm.

Once verified, the transaction is combined with other transactions to create a block of data for the ledger. The new block is then added to the existing blockchain in a way that is permanent and unalterable.

The unchangeable property of blockchain and its public availability among its users, whether in a public ledger or a private one, provides transparency and shows real-time data of transactions.

In the real world, for instance, one can imagine the purchase of a car. If the whole process - right from the manufacturing to the selling, reselling and even reuse or termination of the car will be recorded on an unchangeable ledger that is in public domain then this will eliminate, to a large extent, the possibility of tamper, fraud and prevent its use in illegal activities.

Read — Blockchain: Utopia or Reality?

Alternatively, in simple terms, blockchains are similar to a spreadsheet that is duplicated thousands of times across a network of computers. The network is designed to regularly update this spreadsheet, making the data easily accessible to everyone on the internet. Since the blockchain database is not stored in any single location, it makes it difficult for a hacker to corrupt the information.

The technology has gained significance over the past few years as it promises enhanced security, transparency and incorruptible haven for storing information.

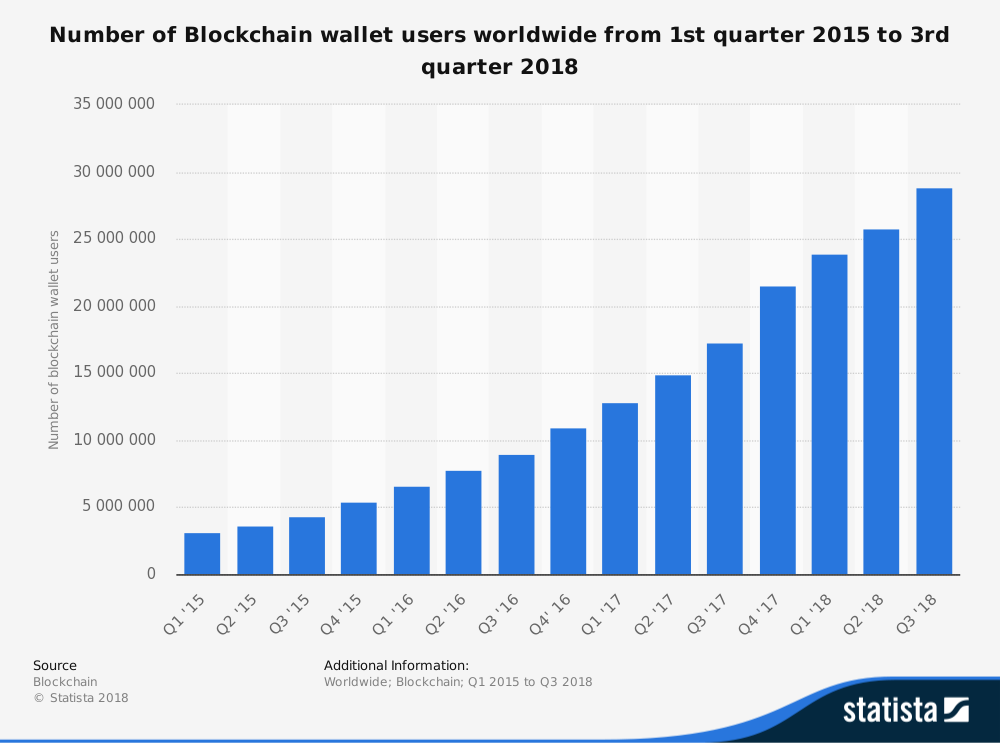

Where can we use blockchain technology?Currently, finance offers the strongest use cases for the technology. The number of blockchain wallet users across the globe jumped 809 percent in Q3FY18 from Q1FY15, according to blockchain.info.

The number of blockchain wallets has been growing since the creation of the Bitcoin, reaching over 28 million users as of September 31, 2018.

Source: Statista.

Source: Statista.The World Bank estimates that over $430 billion in money transfers were sent in 2015 through blockchain wallets and at the moment there is a high demand for blockchain developers.

While finance seems to be the strongest case of use for blockchain, it offers multiple benefits to businesses that use this solution at areas that require a high degree of trust for business transactions.

Read — Blockchain: The right medicine for asset management industry

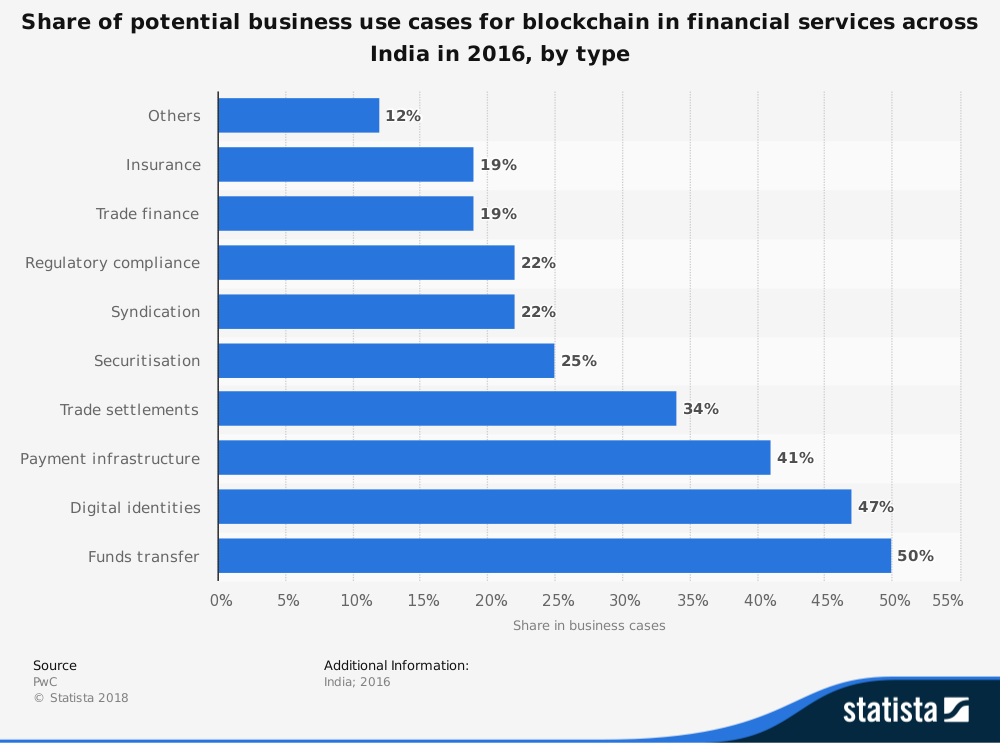

Other possible cases where blockchains can be used include digital identities, payment infrastructure, trade settlements, securitisation, trade finance, and insurance.

For instance, smart contracts in blockchains can be used in real estate to support complex legal agreements. In a smart contract, parties can agree on a sequence of conditional execution paths based on events. Smart contracts, invented in the 90s by Nick Szabo, in blockchain are little programs that execute if certain criteria are met. They were integrated into blockchain technology and cryptocurrencies by Ethereum. Thus, smart contracts can be applied for any system that involves a contract between a seller and a buyer.

Source: Statista.

Source: Statista.Many enterprises including Microsoft and IBM are focusing on this technology as the model provides users with more accessibility, privacy and control over their personal data. The blockchain technology offers companies a better solution to protect their users' data.

The technology also offers a possibility to reduce costs and an opportunity for businesses to build and maintain an infrastructure that delivers capabilities at lower expenses than traditional centralised models.

Read — How and why blockchain technology is a tough nut to crack for hackers

Blockchain can process transactions faster because it doesn't use a centralised infrastructure. And even though there is no system totally secure from cyber attacks, the distributed nature of blockchain provides an unprecedented level of trust. These characteristics of blockchain have been drawing the attention of several startups, enterprises as well as government to implement this technology.

"In the past year, we have seen several instances of funding for blockchain based Bitcoin exchanges based in India. However, in the traditional financial services sector, the potential use cases around the underlying architecture of blockchain, i.e. Distributed Ledger Technology (‘DLT’), look promising. Blockchain based systems offer vastly improved trust and transparency, and due to its native regulatory advantages, the adoption of DLT in the Indian banking sector is also finding support from regulators," according to a FinTech Trends Report by PwC.

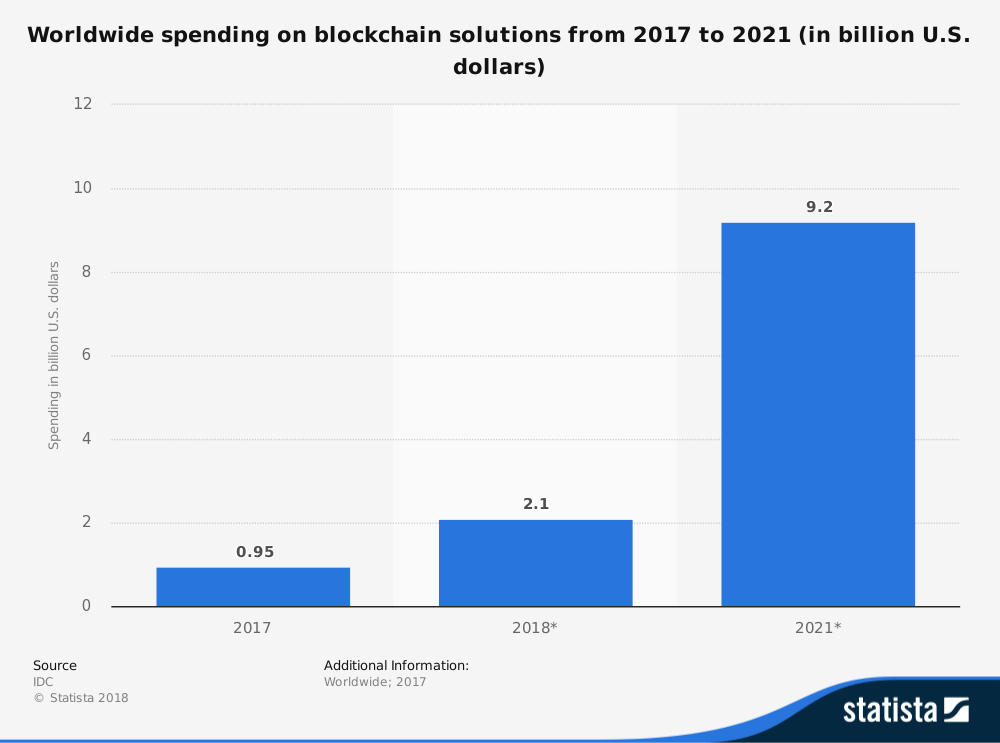

Use of blockchain to increase furtherOwing to a number of these benefits, the worldwide spending on blockchain solutions has been increasing. Worldwide spending on blockchain solutions is forecast to reach $2.1 billion in 2018, more than double the $945 million spent in 2017, according to the inaugural Worldwide Semiannual Blockchain Spending Guide from International Data Corporation (IDC).

Source: Statista.

Source: Statista.IDC expects blockchain spending to grow at a robust pace over the 2016-2021 forecast period with a five-year compound annual growth rate (CAGR) of 81.2 percent and total spending of $9.7 billion in 2021.

"Many technology vendors and service providers are collaborating and working with consortiums such as the Enterprise Ethereum Alliance and the Hyperledger Projects to develop innovative solutions that improve processes such as post-trade processing, tracking and tracing shipments in the supply chain, and transaction records for auditing and compliance. Also, multiple regulators and central banks have made positive comments about blockchain and DLT and this will help to accelerate demand in regulated industries such as financial services and healthcare," Bill Fearnley, Junior Research Director, Worldwide Blockchain Strategies, said.

These developments indicate that use blockchain technology is going to shoot up in coming years. This also means that the Indian blockchain developers may be bidding on the right technology.

"It is clear that with the numerous benefits associated with Distributed Ledger Technology (DLT) and support from regulators, blockchain is poised for rapid growth in the Indian banking sector in the years to come," the FinTech report said.

Challenges aheadWhile the available data indicates at a massive expansion in the use of blockchain technology, it still has a lot of barriers on its path. According to a PwC report, many organisations that have at least some involvement with blockchain technology feel regulatory uncertainty (48 percent) is the major barrier for its adoption worldwide.

Lack of trust among users (45 percent) and the ability to bring the network together (44 percent) are the next two barriers that these enterprises believe would affect them in the next three to five years.

Source: Statista.

Source: Statista.Since the technology is still new, users are skeptical about its reliability, speed, security, and scalability. There are also concerns regarding a lack of standardisation and the potential lack of interoperability with other blockchains.

Lack of understanding among users also contributes to the trust gap. Even now, many executives are unclear on what blockchain really is and how it is changing all facets of businesses. People would perhaps need more time to adopt this new technology, develop trust and use this platform for several applications.

"It is perhaps ironic that a technology meant to bring consensus hits a stumbling block on the early need to design rules and standards," the report said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

| 1W returns-4.19% |

| 1W returns-4.63% |

| 1W returns-5.77% |

| 1W returns-9.71% |

| 1W returns-10.56% |

| 1W returns-14.26% |

| 1W returns-17.33% |

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.