At a time when numerous pharmaceutical industry stalwarts are battling with regulatory issues and erosion of margin in the once highly profitable generic business in regulated markets, Eris Lifesciences's (ELL) offer for sale is a welcome change. With a predominant focus on the domestic formulations market, a robust portfolio of largely prescription-based drugs, and a tilt towards a more promising chronic portfolio, the company seems fundamentally strong.

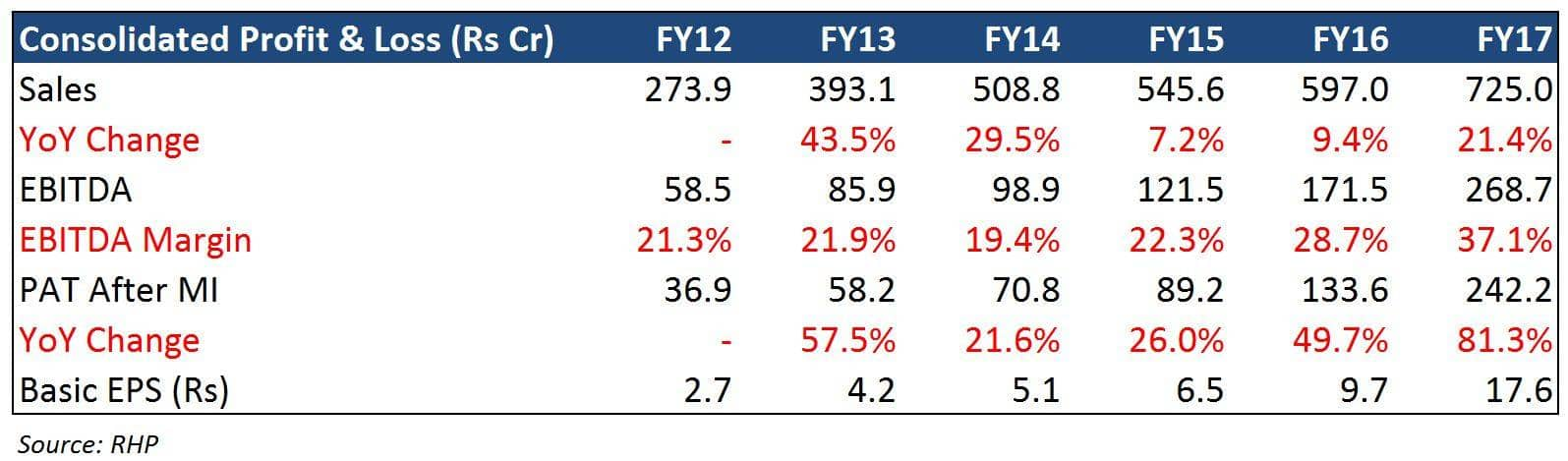

In the past four years, while the company's revenues have grown at a CAGR of 17 percent, EBIDTA recorded a growth of 33 percent, as operating margins improved from 22 percent in FY13 to 37 percent in FY17. The after-tax-profit has exhibited a very commendable CAGR growth of 43 percent in the past four years. Consequently, the company boasts of return ratios in the mid-forties.

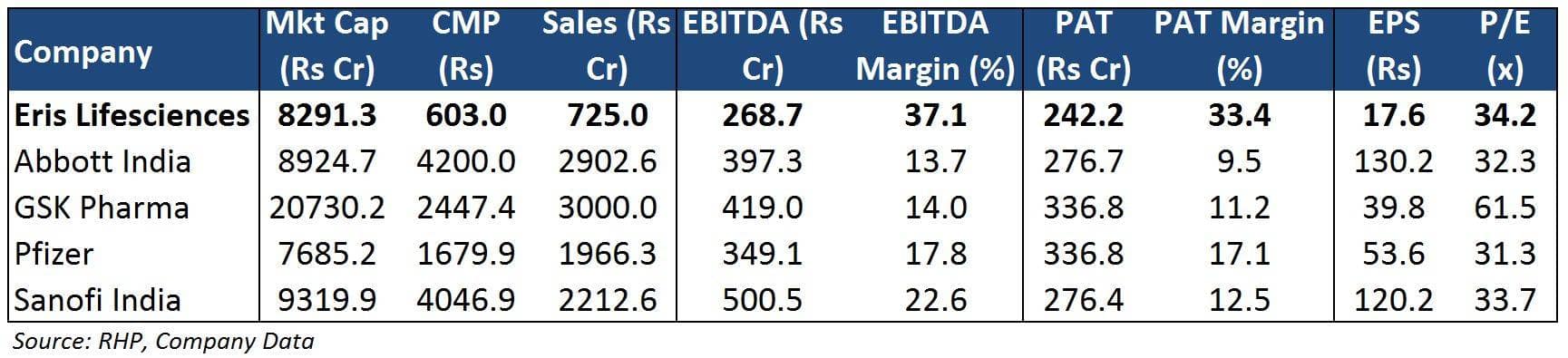

At the upper end of the price band of Rs 603, the stock is available at 34.3x FY17 earnings. While, prima facie, the same looks expensive, the valuations are justified on account of the superior business profile and earnings matrix. Subscribing to this IPO would certainly benefit the investors.

BackgroundIncorporated in 2007, Eris Lifesciences (ELL), an Ahmedabad-based company, is engaged in the business of manufacturing and commercialising branded pharmaceutical products in the Indian pharmaceutical market (IPM). Its chronic formulations cover therapeutic segments like cardiovascular diseases and diabetes, whereas the acute segment covers vitamins, gastroenterology, and gynaecology. The company’s focus market in India is largely the metros and Tier 1 cities, since the incidence of lifestyle disorders and availability of specialists/superspecialists are largely concentrated in these areas.

The Rs 1,740 crore offer, with a price band of Rs 600-603, will see the complete exit of financial investor Botticelli (the investment arm of ChrysCapital) and a minor stake sale from the promoter.

So what makes Eris Lifesciences a good investment proposition?Strong Sales Growth: ELL largely caters to diabetologists and endocrinologists that generate the highest value per prescription. ELL’s chronic segment, which recorded the highest pan-industry CAGR growth of 28.9 percent in the past four fiscals, positioned the company in India’s top 25 in the chronic formulation space.

From FY13 to FY17, the company’s sales grew at a CAGR of 21.7 percent, outperforming the overall market’s CAGR growth of 11.8 percent.

With a steadily growing presence in the chronic pharma market pan-India, ELL's efforts are directed towards connecting with medical professionals across the country to monitor drug requirements closely.

Chronic segment revenue (Rs 549 crore) composition in FY17 (%)

Chronic segment revenue (Rs 549 crore) composition in FY17 (%)  Acute segment revenue (Rs 289 crore) composition in FY17 (%)

Acute segment revenue (Rs 289 crore) composition in FY17 (%)

Brand Portfolio Expansion: The product portfolio of ELL includes 80 mother brand groups.

ELL targets adding one new brand per division every year through its seven divisions. To consolidate its brand strength, the company’s expansion strategy entails introduction of new drug brands in therapeutic areas of neurology, dermatology, osteoarthritis, and musculoskeletalogy.

ELL and its subsidiaries, with 138 trademarks in their combined kitty, are seeking registrations for more than 200 trademarks to simultaneously intensify their brand appeal.

ELL acquired 40 trademarks from ‘Amay Pharma’ (to strengthen its cardiovascular and anti-diabetic product offerings) and 75 percent of ‘Kinedex’ (to enhance its footprint in connection with mobility disorders).

Local Market Focus, Industry Tailwinds: India's pharmaceutical market is amongst the biggest markets globally and continues to expand at a good pace. Unlike most of its blue chip peers, ELL’s focus is solely on the domestic market, thereby insulating itself from regulatory hassles of developed market regulators and price erosion in generics.

A large portion of the market is led by prescriptions and not by hospitals or over-the-counter drugs. More number of registered medical practitioners, improving medical diagnostics, and higher healthcare spending by the government have resulted in the number of prescriptions going up.

Risks: While the business apparently looks convincing, investors must bear in mind that manufacturing of certain products is outsourced by ELL to 20 manufacturers, thus making the company dependent on latter's performance to an extent. Disruptions at the company's only manufacturing facility at Guwahati (Assam), in addition to withdrawal of region-based tax incentives due to termination or non-compliance issues, could have an adverse bearing on the financials, too.

Changes in regulatory policies pertaining to drug pricing, unpredictability associated with raw material prices, high dependence on mother brands, and an unexpected shift in demand towards generics at the expense of brands are some of the other concerns.

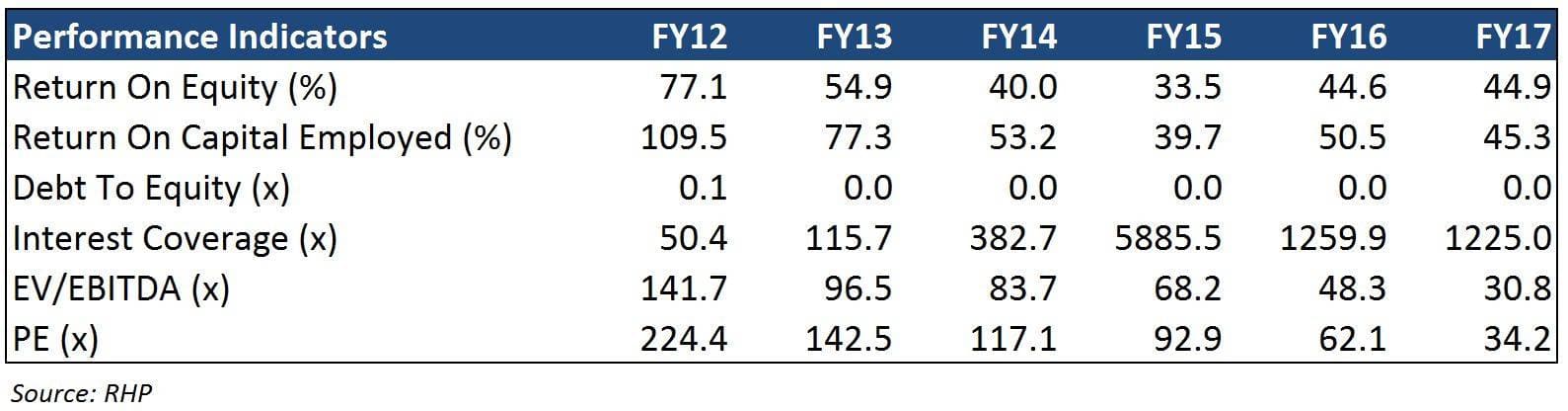

Financial Snapshot

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.