Madhuchanda DeyMoneycontrol Research

This early bird of the earnings season rarely disappoints and the current quarter was no exception. IndusInd Bank reported another set of predictably decent earnings for the first quarter of FY18.

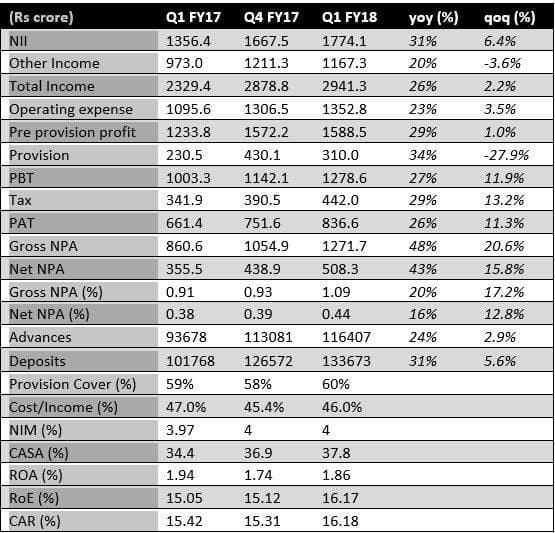

The reported profit-after-tax of Rs 836.55 crore grew by 26 percent on a year-on-year basis, riding on 31 percent growth in net interest income (difference between interest income and interest expense), thanks to 24 percent growth in advances and a stable net interest margin at 4 percent. The non-interest income grew by 20 percent driven by 25 percent surge in core fees. Distribution of third-party products, investment banking and forex were the drivers of the core fees.

The sequential growth was especially impressive at 11 percent as the previous quarter was witness to an incremental provision of Rs 122 crore on a corporate account (Jaiprakash Associates) pending closure of a cement deal with UltraTech.

What continues to impress us about IndusInd is its superior execution on the asset as well as the liability front along with an excellent management of asset quality in a difficult environment with a reasonably large book.

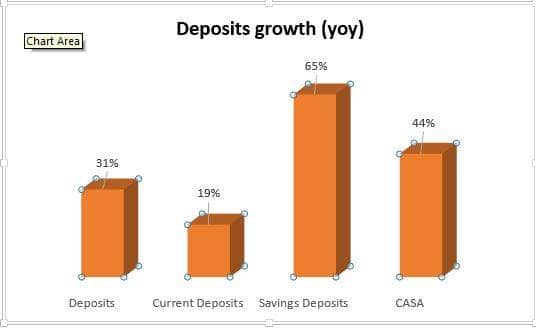

Low-cost deposits gaining traction: While overall deposits grew by 31 percent, the low-cost CASA (current and savings account) grew by 44 percent. Although the bank had internally set a target of achieving 40 percent CASA by 2020, it looks set to hit the same much earlier.

The growth in savings account has been particularly impressive as the bank is adding new customers at a brisker pace and has achieved some breakthrough in government business as well.

De-risking the book: The efficiency that the bank is building on the funding side is positively impacting its market share in credit and helping it to create a higher quality corporate book.

The bank is systematically capturing market share in the working capital lending business, thanks to its cost advantage on the liability front in the MCLR (marginal cost of lending rate) regime. The selective exposure to high-rated corporates is reflecting on its capital adequacy ratio that has shown a steady improvement. This strategy will enable it grow without consuming capital at the same rate.

In an industry where public sector banks are not playing an active role in incremental businesses, savvy players of the likes of IndusInd can actively garner market share. Our analysis suggests that while IndusInd has 1.5 percent share in overall bank credit, its share in incremental credit in the past one year stands at an impressive 5.6 percent.

Retail book all set to grow in the second half: The quarter saw corporate book growing by 26 percent and retail by 22 percent largely on account of the lower growth of vehicle finance book at 17 percent. With the disruption on account of BS IV largely behind and the adjustment pangs of GST not lingering beyond September, a lot of pent-up demand is expected in the second half of the fiscal that should drive stronger growth in retail and lend support to net interest margin.

Creating buffer for the rainy day: The provision of Rs 122 crore that was created in the last quarter didn’t flow to profit but was used up to create a cushion for the rainy day. The bank has created floating provision of Rs 70 crore, Rs 33 crore standard asset provision (pending some receipt from the corporate post the deal closure), Rs 10 crore for security receipts (receipt against asset sale to asset reconstruction companies) and Rs 10 crore for the micro finance book. In fact, the provision coverage has shown an improvement.

Cautious on troubled sector: The loan book on micro finance hasn’t grown in the quarter and out of the Rs 50 crore portfolio at risk, Rs 31 crore has been provided and incremental provisioning requirement in the coming quarter is unlikely to be insignificant. Similarly, the exposure to telecom has also come down to 2.1 percent of assets (down from 3.1 percent previous quarter) and that too only to corporates rated above A. Incidentally, the bank has prudently increased the standard asset provisioning for this exposure.

Asset quality, optical slippages: While optically gross NPA has risen by 20 percent sequentially, the same is on account of slippage of two accounts from restructuring book. Consequently, the restructured book has fallen from Rs 415 crore to Rs 200 crore and the overall stressed (NPA+restructured) assets hasn’t altered.

The bank has minuscule Rs 50 crore exposure to the dirty dozen (coming from three accounts) and carries substantial provision on them. The management does not expect major stress from any account if more were to be considered for resolution by consortium lenders.

We continue to be impressed with IndusInd’s strategy of emboldening its position when the competition is weak, with its superior execution strategy. The stock has generated a handsome return and trades at 4X adjusted book of FY18. However, it will continue to enjoy the fan following of long-term investors looking for high-quality growth.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.