Renuka Sane, Ajay Shah, Bhargavi Zaveri

Runs on banks

Runs on banks are to finance what supernovae are to astronomy. RK Narayan's book The Financial Expert vividly tells the tale of the chaos and misery of a bank run.

Bank runs are not random events. The key things that make bank runs happen is the fact that each depositor has the incentive to run when faced with a slight chance of a run developing. Robert K Merton used runs as a motivating example of his introduction of the concept of ‘self-fulfilling prophecies’. In order to understand runs, we must understand the incentives of each customer.

Suppose a bank is not protected by the government or by the central bank. Suppose you see many depositors running to take their money out of the bank. Now there are two possibilities.

If you believe the bank is unsound, then it is efficient for you to stand in the queue and try to take your money out. If others do this before you, then you may be left with nothing.

Even if you believe the bank is sound, you know that a bank with illiquid assets and liquid liabilities will default when faced with a run. While you will get your money back (as the bank is sound), you will suffer the loss of time value of money and you will suffer the uncertainty of it all working out. Hence, it's efficient for you to stand in the queue and try to take your money out.

Runs on mutual funds

We know a lot about runs on banks. What about runs on mutual funds?

At first blush, the simple technology of a mutual fund — NAV based valuation, full mark-to-market, liquid assets — seems run-proof. But in September, Rs 2.35 trillion exited Indian mutual funds. Why did such an outsized exit take place? It cannot be just coincidence that many people felt like leaving at the same time.

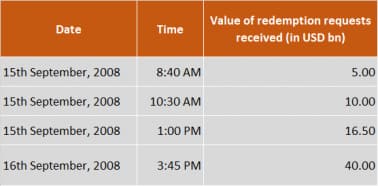

Large exits have taken place with mutual funds elsewhere in the world too. During the 2008 crisis, the Reserve Primary Fund (with exposure to Lehman Brothers' commercial paper) witnessed a similar run-like situation. The US district court's order directing the liquidation of the fund records show redemption requests aggregating to two-thirds of the value of the assets of the fund were received in a span of less than 48 hours immediately following Lehman Brothers having declared bankruptcy (graph below).

What are the incentives that shape the behaviour of an investor in a mutual fund? How can a mutual fund industry be susceptible to runs?

Channel 1: Over-valuation can lead to runs

Suppose a mutual fund has 100 bonds that are liquid, where the true price (market price) is Rs 100. In addition, it has 100 bonds that are illiquid. The market does not give a reference price for the illiquid bond. If we tried to find out a prospective sale price, it would be Rs 50. Suppose the mutual fund claims that this bond is worth Rs 75. The true portfolio value is Rs 10,000 + Rs 5,000 = Rs 15,000, but the mutual fund claims the value is Rs 17,500. Suppose there are 100 units. In this case, the NAV should be Rs 150, but it is shown as Rs 175.

Over-valuation destabilises rational investors. The rational investor knows that each unit is truly worth Rs 150, but if she redeems right away, before the mistake in the NAV calculation is corrected, she will get Rs 175.

When one unit runs at Rs 175, where does the excessive payment of Rs 25 come from? It comes from the investors who did not run. This is unfair, and it creates strong pressure to run.

Channel 2: False promises can lead to large redemptions

Suppose a mutual fund has been sold to investors under the false promise of it being a safe product. In this scenario, investors do not expect fluctuations in the NAV, and believe that their investments will be shielded from turmoil in the markets. If, for any reason, this expectation is belied, then investors may get spooked by sharp falls in the NAV. This may induce large redemptions.

In the US, there was a claim that the NAV of money market mutual funds would not drop below $1. This was termed 'breaking the buck'. In 2008, when the NAV did drop below $1, this caused panic and the flight of investors who had been told all along that the scheme would not break the buck.

Channel 3: Runs in an illiquid market

The Indian bond market is extremely illiquid, but even within this landscape, there is heterogeneity in the extent of illiquidity. Fund managers will be sensitive to the transactions costs faced when trading in alternative instruments, and choose the most liquid ones first.

Suppose a mutual fund has some cash in a liquidity buffer, it has 100 bonds that are more liquid, where the true price (market price) is Rs 100. In addition, it has 100 bonds that are illiquid. Suppose fair value accounting is indeed done, and we correctly value the illiquid bonds at Rs 100. The trouble is, the illiquid bonds incur large transactions costs when selling in large quantities. While there is a (bid+offer)/2 of Rs 100, in truth, when a large quantity is sold, the price realised will be Rs 90. This is an ‘impact cost’ of 10 percent.

Therefore, when the first redemptions come in, the mutual fund will adjust by using cash and then it will adjust by selling the liquid bond. At first, things seem fine. But in time, the mutual fund will have to rebuild its cash buffer. It will have to get back to a more diversified and more liquid portfolio. For this, it is going to have to sell the illiquid bond, and at that time the NAV will go down.

There is an overhang of selling of illiquid bonds that is coming in the future. In this situation, investors are better off leaving early as they get the clean exits associated with the early use of cash and the early sale of liquid bonds.

Channel 4: Systemic spillovers in an illiquid market

When large redemptions take place in even one or two schemes, at first they will use cash buffers and sell liquid instruments. But when they start selling illiquid instruments, this changes the price of those illiquid instruments. Now declines in prices hit the NAVs of all schemes that hold those instruments. Through this, large redemptions on a few schemes propagate into reduced NAVs (at future dates) across the entire mutual fund industry. Prediction: In periods of large inflows/redemptions, we will get a pattern of auto-regression in the mutual fund NAVs across days, across the multiple funds that hold a pool of illiquid instruments.

Rational investors anticipate this phenomenon, and have an incentive to run when they see large redemptions in even a few mutual fund schemes (and vice-versa).

Runs on mutual funds are a complex phenomenon

We have shown four distinct channels through which large redemptions on mutual funds can develop:

It is interesting to see the ‘curse of liquidity’. When redemptions come in, mutual funds will sell their most liquid bonds first. Through this, innocent bystanders — the issuers of liquid securities — will suffer from price impact and a higher interest rate.

Thinking about runs on mutual funds thus requires a full view of the problems of consumer protection (if all consumers accurately understood the risks that they were taking, they would be less spooked when events unfold), financial market development (the lack of a liquid bond market) and systemic risk (channels of contagion through which disruption of some parts of finance induces disruption of other parts of finance).

Interesting recent experiences in India

While India has not seen a full blown run on mutual funds as was seen in the US in 2008, a few instances of defaults on bond repayments followed by falls in NAVs and rise in redemption requests offer useful insights.

Amtek Auto (2015): In September 2015, Amtek Auto defaulted on a bond redemption of Rs 800 crore. In the Indian corporate bond market, once a default takes place, the bond tends to become highly illiquid. The Amtek Auto bonds were held by two debt schemes of JP Morgan Mutual Fund.

JP Morgan did an unusual thing: they put a cap on redemptions. It subsequently used something analogous to a good-bank-bad-bank structure, where the scheme was split into two, and the second part held the Amtek Auto bonds, and could not be redeemed.

This did not go down well with SEBI. SEBI sought to penalise JP Morgan for, among other things, not following “principles of fair valuation under mutual fund norms” and for changing fundamental attributes of the scheme without giving an exit option to the investors. Nearly three years after the incident, JP Morgan settled the matter by paying a settlement fee of about Rs 8.07 crore under the provisions of the SEBI Act, 1992 providing for settlement of civil and administrative proceedings.

Ballarpur Industries (2017): In February 2017, Ballarpur Industries defaulted. At the time, Taurus Mutual Fund held their commercial paper. Unlike JP Morgan's response, Taurus Mutual Fund reportedly marked down the value of the paper to zero. This is a sound and conservative strategy as it gives a bad deal to the persons who run.

Other mutual funds reportedly sold such paper to group companies or took it on their own balance sheet to shield the investor from the NAV hit.

IL&FS (2018): More recently, IL&FS group firms have defaulted on bonds issued by them. These bonds are present in certain mutual fund schemes. Some mutual funds have portrayed this event as a loss of 100 percent, while others have portrayed a 25 percent loss. Credit rating agencies were very late in understanding the problems of IL&FS, and to the extent that credit ratings are used in computing the NAV of a mutual fund scheme, these NAVs would have been overstated.

(Reproduced with permission from www.blog.theleapjournal.org. This is the first part of a two-part series.)

(Renuka Sane and Ajay Shah are researchers at NIPFP. Bhargavi Zaveri is a researcher at the Finance Research Group, IGIDR. Views expressed are personal).

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.