Anubhav SahuMoneycontrol research

Bhansali Engineering Polymers (BEPL), a leading manufacturer of a speciality polymer (ABS), is expected to benefit from a ramp-up in capacity. Resultant volume growth holds significance in the Indian market, which is greatly served by imports (40 percent). Further, the company’s focus on high-margin variants, research for new products, and a debt-free balance sheet warrant investors' attention.

Company’s Brief

Incorporated in 1984, Bhansali Engineering (market cap: Rs 1,150 crore) is one of the two biggest manufacturers of ABS (Acrylonitrile Butadiene Styrene) polymer. BEPL and Ineos Styrolution, together, cater to about 60 percent demand for ABS in the Indian market. Two-thirds of Bhansali’s ABS products are specialty variant, serving client requirements. The company has a technical tie-up with Nippon A&L (leading ABS resin manufacturer) for future expansion plans and new variants of the ABS. Its manufacturing facilities are located at Abu road and Satnoor (MP). End-market for the company’s products is the auto industry (accounting for about 50 percent of BEPL's revenues), followed by white goods industry. Key clients for the company are Maruti, Hero MotoCorp, LG and Samsung.

ABS: High margin plastic for usage in consumer durable goods

ABS is a relatively high-margin thermoplastic compared to commodity plastics like poly ethylene, poly propylene and polystyrene. It is made by polymerising styrene and acrylonitrile in the presence of polybutadiene. As the proportion of all three ingredients varies, product's functional properties — strength, rigidity and shiny surface (acrylonitrile, styrene) and toughness at low temperature (butadiene) — also differ. It has its usage in automotive (dashboards), white goods, electronics and cellphone industries.

Supply deficit in Indian market provides scope for expansion

Currently, demand for ABS in Indian market is 275,000 MT and is expected to grow by close to 15 percent CAGR in the medium term. Bhansali Engineering and Ineos Styrolution have a capacity of 80,000 MT each in the ABS business constituting 58 percent of the domestic demand. Rest of the demand is catered to by imports which, in turn, are majorly general purpose ABS (low margin).

ABS manufacturing business has a high barrier at entry not only because of the investments, but also due to R&D (research and development) required for superior functional qualities and customisation. High degree of customisation is one key reason for the clients’ stickiness leading to long-term contracts. It is worth noting that LG Chem, one of the largest ABS producers globally, sources ABS variants from BEPL for its India requirement to meet required local functional and appearance traits.

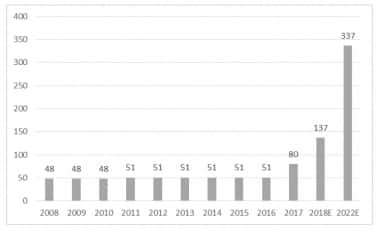

Four-fold Capacity Expansion by 2022

Bhansali is operating at a capacity utilisation of 64 percent which is expected to reach 90 percent by the end of FY18. It is expecting a major capacity expansion from 80,000 MT to 137,000 MT per annum by the end of FY18. It is a brownfield expansion where the required capex (Rs 35 crore) will be funded through internal accruals. Additionally, the company is targeting 200,000-MT capacity near Kandla by the year 2022. Being closer to a port would also help in saving freight cost.

Chart: Ramp up in manufacturing capacity (‘000 MT) expected

Supply Interruption of Raw Material is Key Risk

Monomers and other raw materials used for ABS are oil derivatives and subject to fluctuation in international oil prices. Key raw materials for ABS — styrene and acrylonitrile — are imported. So, international supply and demand dynamics drive the prices of these materials. Other crucial raw material is butadiene, which has been a cause of worry in the last financial year due to limited supply. However, as per Bhansali Engineering, butadiene constitutes about 15 percent of weight of raw material and hence, relatively a lessor factor impacting cost dynamics.

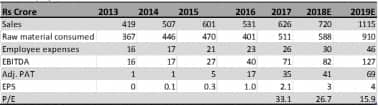

Financial Projections

Based on the near-term capacity expansion plans, the company is expected to post revenue CAGR (FY17-19E) of 33 percent. Even though the company management is quite optimistic on capacity utilisation front, we estimate 70 percent utilisation (close to global average) for the added capacity in the year 2019, which is feasible in our view, on account of supply deficit in the domestic market. EBITDA margins are expected to remain in the vicinity of 11 percent based on improved product mix offsetting a relatively higher input cost. Interest expenses are expected to remain contained as the company plans to incur near-term capex from internal accruals.

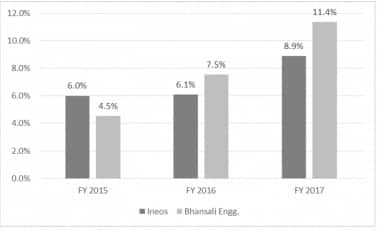

Improving EBITDA Margin Profile

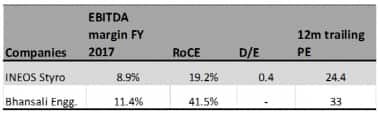

The company’s trailing valuation multiple is elevated compared to its peer Ineos Styrolution.

This, however, has to be seen in the context of a sharp run-up in the stock price and its superior fundamentals and the growth plans. Investors got to remember that considering the future volume and earnings growth, valuations at 15.9 times 2019E earnings look reasonable. With trailing P/E at 33x, and earnings CAGR (FY17-19E) at 41 percent, PEG ratio works out at 0.8, making it still a worthwhile investment case.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.