Many of us have our favorite economic and financial indicators. I’m referring to those indicators that don’t get a lot - if any - attention from the television channels geared toward finance and markets and yet can provide important insights. One of my favorites - the divergence between key US and German fixed-income benchmarks - is at a notable level.

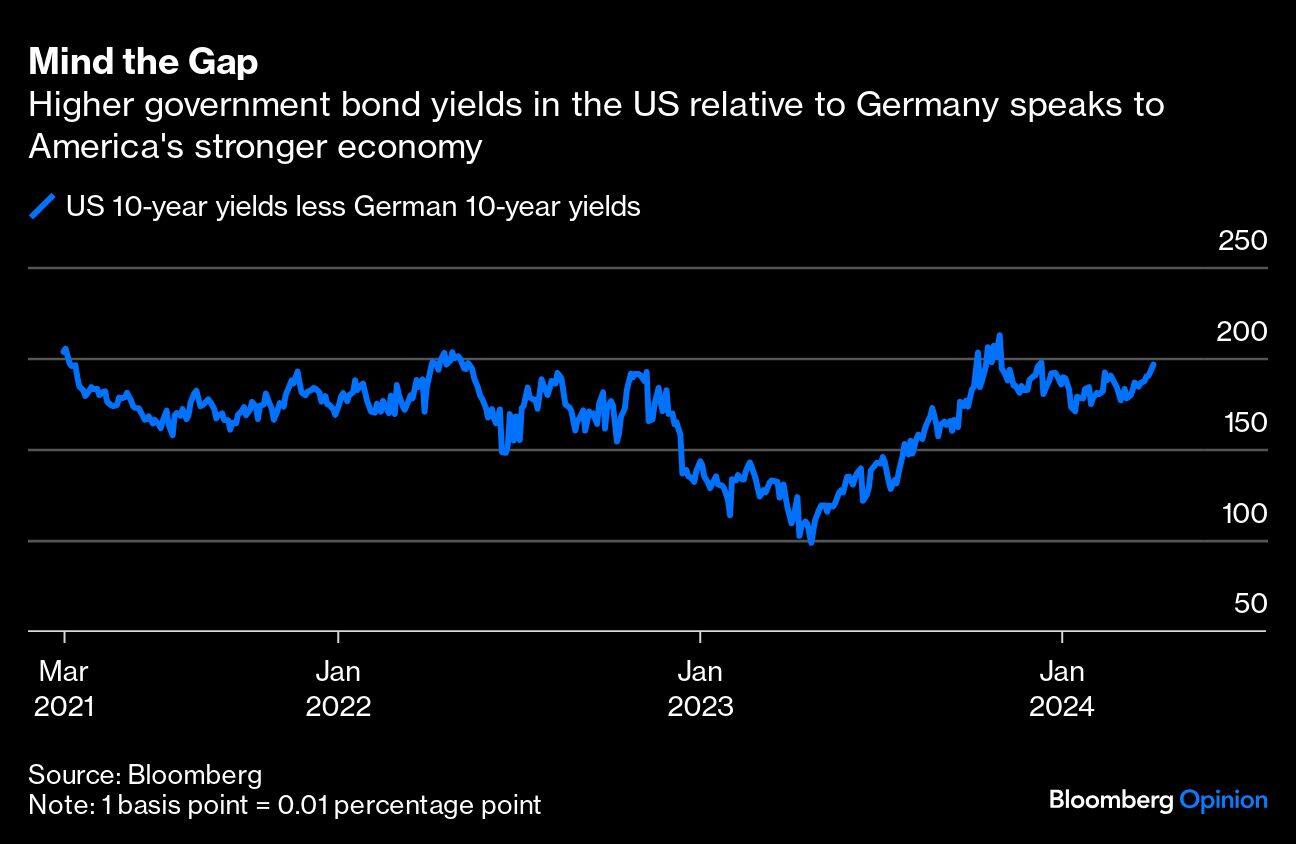

More specifically, I’m talking about the difference between the yield on the 10-year US Treasury note and its counterpart in Germany (which also serves as a benchmark for much of Europe). In early trading Wednesday, this differential had risen to 200 basis points in favor of the US, a level only reached three times since the start of 2020. Moreover, and as shown in the chart below, it is now well above the low over the past three years of 90 basis points and just short of the high of 214 basis points.

Two major developments have driven the recent widening. One is that US economic data overall has been stronger than consensus forecasts. The other is lower-than-expected euro zone inflation data.

Fundamentally, the widening captures the dominance of American economic exceptionalism over European economic stagnation, illustrated most comprehensively by the contrast between 4% growth in US gross domestic product in the second half of 2024 and recession in Germany. With that comes a divergence in inflation rates, with US price increases proving more stubborn than Europe’s in what many view as the “last mile” in central banks’ battle against inflation.

Importantly, there is more to this divergence than just recent economic numbers. The US economy is on a healthier endogenous growth path compared with Europe.

In addition to being supported by a more favourable set of initial conditions – from greater flexibility in factors of production to more agile entrepreneurship – US growth also has been boosted by a bigger fiscal impetus and stronger policy focus on the drivers of future economic growth. Also, as noted recently by Andrew Balls, the Pacific Investment Management Co.’s chief investment officer for global fixed income, in an interview with Bloomberg News, the structure of the US mortgage finance system makes its economy less sensitive to higher interest rates.

Also, the policy support being provided to three critically important sectors in a secular transition – technology, life sciences and energy – has an even greater influence in light of the important advantages that come with being among the very “first movers.” If implemented properly, this support is enough to maintain the US growth advantage over the medium-term, though probably not enough to act as a major engine of growth for many other countries (unless they, so to say, “pull up their socks” both economically and financially).

Specifically, and given what is happening regionally in Europe and in its major trading partner China, it is unlikely that more buoyant US growth will give Europe much of a boost. It is even less likely that Europe’s sluggishness will drag down the US economy. Only a major exogenous shock of some sort that derails the US, such as another monetary policy mistake by the Federal Reserve or a geopolitically-driven surge in oil prices ti, say, $100 or more a barrel, would result in the type of convergence that sees the 10-year yield differential narrow back to 100 basis points or less.

This outlook has implications for global investors beyond relative portfolio positioning in international fixed income markets. For example, it serves as a cautionary note to those looking to quickly fade US equities in favour of Europe as well as those betting on a weaker dollar.

The divergence can also serve as yet another complication for a global economy that is already navigating multi-year structural changes such as the reworking of supply chains, the greater weaponization of cross-border trade and investment tools, and what is likely to be the uneven application of major productivity-enhancing innovations such as artificial intelligence.

Am I making too much of a financial indicator that many overlook in their analyses of high frequency data? Time will tell. In the meantime, I will keep it under constant review.

Mohamed A. El-Erian is a Bloomberg Opinion columnist. Views are personal and do not represent the stand of this publication.

Credit: Bloomberg

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.