Sachin PalMoneycontrol Research

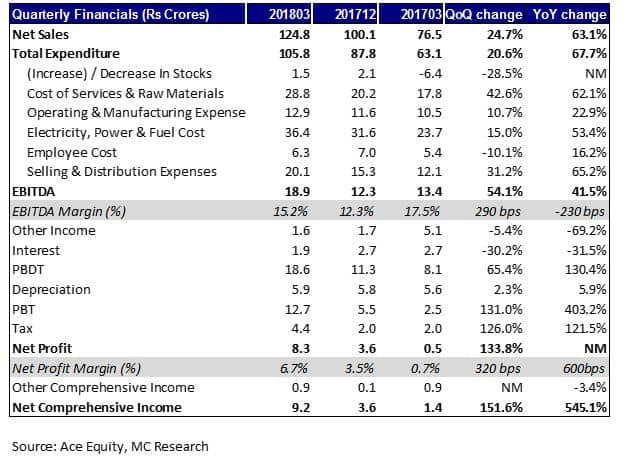

Shree Digvijay Cement, a Gujarat-based cement manufacturer, reported a healthy set of numbers for the March quarter. The company reported an EBITDA (earnings before interest, tax, depreciation and amortisation) of Rs 18.9 crore on sales of Rs 124.7 crores.

The company's performance was particularly remarkable as it reported a rise in sales of 63 percent compared to the same quarter a year ago, and also reported its highest quarterly sales figure in the last three years.

The company's EBITDA margin for the quarter under review declined to 15.2 percent, as against 17.2 percent in the March quarter last year. However, this was higher than the 12.3 percent margin the company reported in the December quarter this year.

The increase in selling and distribution expenses was the primary reason for margin retracement.

Total comprehensive income surged almost 2.5 times quarter-on-quarter (QoQ), driven by healthy operating profit and lower interest costs. The interest costs came in much lower as the company reduced its gross debt from Rs 96 crore to Rs 25 crore in FY18.

Yearly performance

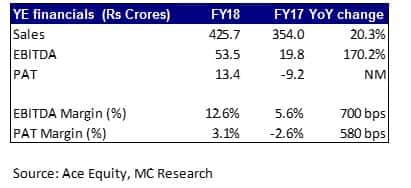

The company reported a revenue growth of 20.3 percent YoY for FY18. Supported by growth in revenue and operational efficiencies, EBITDA too rose to Rs 53.5 crore for the year.

The company also reported a turnaround at the PAT level, with net profit coming in at Rs 13.4 crore, as against a net loss of Rs 9.2 crore last year.

Shree Digvijay Cement (SDC) is promoted by Brazilian company ‘Votorantim Cimentos’, which holds a 75 percent stake in the company. Votorantim is the seventh largest company (by EBITDA) in the building materials industry globally.

Shree Digvijay Cement (SDC) is promoted by Brazilian company ‘Votorantim Cimentos’, which holds a 75 percent stake in the company. Votorantim is the seventh largest company (by EBITDA) in the building materials industry globally.

SDC sells three varieties of cement under the ‘Kamal’ brand name. The product portfolio includes SRPC Cement (Sulphate Resisting Portland Cement), PPC Cement (Portland Pozzolona Cement) and OPC Cement (53 Grade Portland Cement).

Although the company appears to be doing well in recent quarters, SDC had accumulated losses of around Rs 46.8 crore up to FY17. In March 2018, the company approved a scheme of restructuring, under which the accumulated losses will be adjusted against capital reserves.

The stock is trading at an EV/LTM EBITDA (LTM stands for last twelve months; EV stands for enterprise value) multiple of 8.9 times, which is at a minor discount to industry peers. The discount is warranted because SDC’s performance has lacked consistency in recent years.

On a market cap of Rs 470 crore and enterprise value of Rs 474 crore, the stock is currently trading at EV/tonne of Rs 4,409 on a capacity of 1.1 million tonnes per annum. This translates to an EV/tonne of USD 68, which is at a steep discount to the replacement value. Should the company ever decide to move on from such a small capacity, the deal is likely to happen at a premium.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.