Term Insurance is the best way to secure your family’s financial well-being over the long term. They’re cost-effective and simple. Every person with financial dependents must consider buying a term plan before thinking about any other investments.

Pure term plans have one drawback. They don’t offer any payback if you outlive the policy term. You pay premiums for several years and don’t get anything back at the end of the term. There’s one option that’ll seem very enticing to you: TROP or Term Insurance with a Return of Premium.

TROP is a type of term insurance plan that offers a benefit to your family in case your death happens during the term, plus a survival benefit to you, should you outlive the term. The survival benefit is a return of all the premiums you pay through the policy duration.

TROP may sound like a win-win situation where you get your money back in any case. But is that too good to be true? Let’s find out.

How is a TROP plan different from a pure term insurance policy?

Here are two major differences between a regular term insurance policy and a TROP plan.

Premiums: Premiums of a pure term insurance policy are usually very low. In fact, one of the best features of term insurance is the fact that you can get up to a 1000X cover for your annual premiums. On the other hand, premiums for a TROP plan are considerably higher.

Benefits offered: While you get only a death benefit in a pure term plan, TROP plans offer both death and maturity benefits. The higher cost of TROP plans is for the additional assurance that all premiums will be returned to you after the policy term.

What is returned and what is not?

It is important to note even with a TROP plan that not all your payments would actually be returned. Only some parts of the premiums you pay are returned, and even this varies from insurer to insurer. Make sure you go through all the terms and conditions carefully before signing up for a TROP plan.

Generally speaking, here are the parts of the premiums you get back.

Base policy premiums that you paid during the policy term are paid back.

Additional underwriting premiums, that is, extra premiums charged based on medical reports, health, habits, etc. are usually returned. Some exceptions exist. Modal loading premiums, that is, additional premiums the insurer charges when you choose to pay the premiums in monthly, quarterly, or half-yearly modes instead of the annual mode, are usually returned.

Similarly, here are the parts of the premiums that are not returned.

Taxes on the premiums you pay are not returned. (As these are paid to the government).

Rider premiums are not returned. In case you’ve bought an accidental death benefit rider or a critical illness rider , the premiums for those covers are not paid back. There are some exceptions.

Can you surrender a TROP plan during the policy term, and still get repaid?

If you decide to discontinue the TROP plan in the middle of the policy term, you’ll have two options.

Take the surrender value and stop the policy

As soon as you decide to surrender the policy, the insurance company will calculate and pay a surrender value. A surrender value factor (SV factor) is defined by every insurance company and depends on the number of years your policy was in force. The SV factor is multiplied by the total premiums paid to determine the surrender value.

When you surrender a TROP policy:

Death benefit: Will not be paid (as the policy is closed)

Surrender benefit: Is paid to you immediately

Please Note: The formula and factors to calculate the surrender value can be different for different insurers/ products.

Continue the policy as a reduced paid-up policy without further premiums

In a reduced paid-up policy, you can continue the policy until the end of the term without paying any future premiums. The death benefit, however, will be proportionately reduced based on the premiums you’ve already paid.

If you continue the reduced paid-up policy, the reduced benefit will be paid to your nominee if you pass away during the policy term. If you survive, the insurance company will pay back all the premiums you paid before the policy was converted to a reduced paid-up policy.

When you move to a Reduced-paid up policy:

Death benefit: Will be proportionate to the premiums you’ve paid

Maturity benefit: Will be a return of all the premiums you’ve paid

Why might TROP plans not be a good option?

A TROP plan might seem like a good option to invest in, but in reality, it is not. Here are two reasons why.

Expensive premiums

Term insurance is the cheapest type of life insurance available today. However, unlike a pure term insurance policy, the premiums of a TROP plan are very high. The premiums are twice or thrice the premium of a regular term plan and, hence, unaffordable for many.

No Returns on the premiums you pay

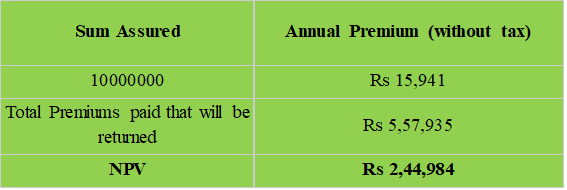

The exact amounts of premiums you pay are returned by the insurance company on the maturity of the policy - and these amounts do not earn any interest. Further, this premium amount is not even adjusted for inflation. When you calculate the NPV (Net Present Value) of the premiums, you’ll be in for a surprise. Here’s an example for you.

NPV calculation of the premium amount for a 30-year-old, male, non-smoker, Rs 1 Crore cover, up to 65 Years, regular pay.

The premiums of Rs 5,57,935 are paid back as survival benefit. But when you take into account inflation and calculate the NPV, the actual value of that premium amount is only Rs 2,44,984. Instead, if you invest the additional premiums in a suitable avenue, you’ll likely earn some interest and grow that money.

In my opinion, what you should do is purchase an adequate term insurance cover for your family as a pure term plan and cover the financial risk of your death. Invest the balance amount in any other financial instrument that will give you better returns.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.