A pure term life cover is an insurance policy that promises to pay your nominee an amount (sum assured of the policy), if you die. But it doesn’t come bundled with investment, unlike traditional life insurance policies. But insurance companies have another way of selling it to you. What looks like a term cover, but comes with an investment wrapper around it. Though you get some return from this policy even if you do not die, the premium is higher.

It’s not profitable for the policyholder. Here’s why.

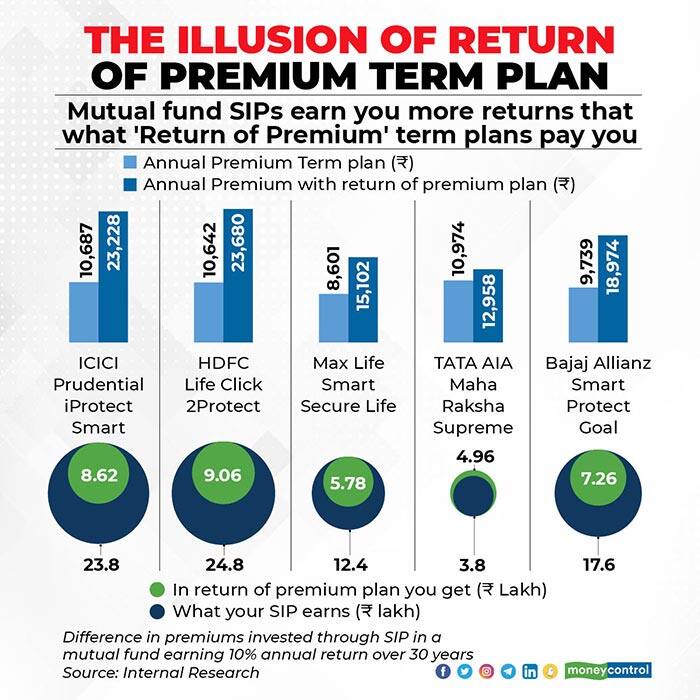

Investing via mutual fund SIP earns better returnsThe right way to look at a life insurance policy is that you pay a cost for protecting your family’s financial future. That is not an investment. That’s why a pure term life cover comes cheap. Whatever extra you save, on account of a low premium, you are free to invest elsewhere and earn returns.

Let’s look at policies from HDFC Life Insurance and ICICI Prudential Life Insurance.

HDFC Life has a term policy for a 30-year-old woman, with an annual salary of around Rs 15 lakh, which she can buy for the next 30 years at an annual premium of Rs 10,690. In this case, the premiums paid will not be returned; it is a pure term policy. In the same policy, you have the option to get your premium back. Here is where the extra cost starts to stack up. Now, the premium itself increases to Rs 23,230 a year. Hence, for the next 30 years, you pay an annual excess charge of Rs 12,540. Over a period of 30 years, that is a difference of ₹3,76,230.

Your first red flag should be that you are paying more to get your money back.

Let’s not stop here. You can take the difference in the amounts of the two types of policies and break it up into equal monthly investment amounts of Rs 1045 to invest in equity-oriented mutual funds. At an assumed rate of 10 percent annually, continued for 30 years, this will grow to roughly Rs 24 lakh. By opting for the regular term policy instead of the return of premium cover, not only are you saving money but also earning a lot more by investing it correctly.

ICICI Prudential iProtect Smart has a return of premium product version and a regular one. The difference in annual premium of the two versions, assuming a maturity age of 60 years and a policy term of 30 years, is Rs 13,000 annually. That is a difference of Rs 3,91,000 over a period of 30 years.

Monthly investments worth Rs 1086 for the next 30 years at an assumed return of 10 percent a year will get you approximately Rs 25 lakh. This is a lot more than any return of premium or survival benefit amount that the policy will pay out.

What should you do?When something sounds too good to be true, it probably is. A term life insurance policy that gives you your premium back is just that. You are losing the opportunity to earn better returns elsewhere by paying a high premium.

If we can figure out the most effective and efficient way to invest money for long periods or decades, it’s hard to imagine that insurance companies don’t already know this.

Mixing insurance and investment is always costly. It’s always a better idea to separate investment from insurance. Don’t fall for the bogus charm of ‘return of premium’ on your term policy. Maximise your life cover, and buy pure term life policies and invest your savings elsewhere, say a quality mutual fund, for better returns. Keep it simple.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.