Buying health insurance is an essential item in a personal finance to-do list. If you have already bought one then you are supposed to renew it every year. Over a period of time, the quantum of health insurance required goes up, and so does the premium payable. Rising health insurance premium rates further inflate the bill. That makes many look for larger cover at relatively less price. Some end up buying super top-up policies. Of late, many insurance companies are offering restoration benefit that makes many believe that their existing covers are enough to take care of large hospitalisation expenses.

Insurance industry officials tell us that these days some first time insurance-buyers typically want to buy policies with restoration benefit and want to settle for a sum-assured they otherwise would have thought inadequate. At the time of renewal, these insurance buyers may end up opting for the renewal of their base health insurance plan and not renew their super top-up insurance plan as they see a restoration benefit being included in the base health insurance plan. Before you decide to buy a fresh insurance cover with restoration benefit or chose to renew your existing policy, get to know the fine print. Basically, does restoration benefit work for you or are you better off buying a fresh insurance policy (super top up) over your existing policy.

What is restoration benefit

The restoration benefit, also known as “recharge”, is an in-built facility offered by the insurer to restore the sum-assured if it is exhausted in the policy year. The idea is to offer insurance cover even if one uses up all he has. For example, one has a health insurance benefit of Rs 3 lakh and suffers from a cardiac condition. The claim of Rs 4 lakh is raised, and he is paid Rs 3 lakh. If the policy has in-built restoration benefit, then he will get another sum-insured of Rs 3 lakh, in the same year, as opposed to the policy amount being restored in the next year like in all other typical health policies. Now, say, he is hospitalised due to an accident in the same year going forward, the insurer will honour a claim up to Rs 3 lakh. “The restoration benefit is available within the same policy which is triggered post-exhaustion of base sum-insured and cumulative sum-insured if any,” says Puneet Sahni, the head of product and marketing, SBI General Insurance Company.

Though the offering looks good, do understand it in finer detail before you opt for one.

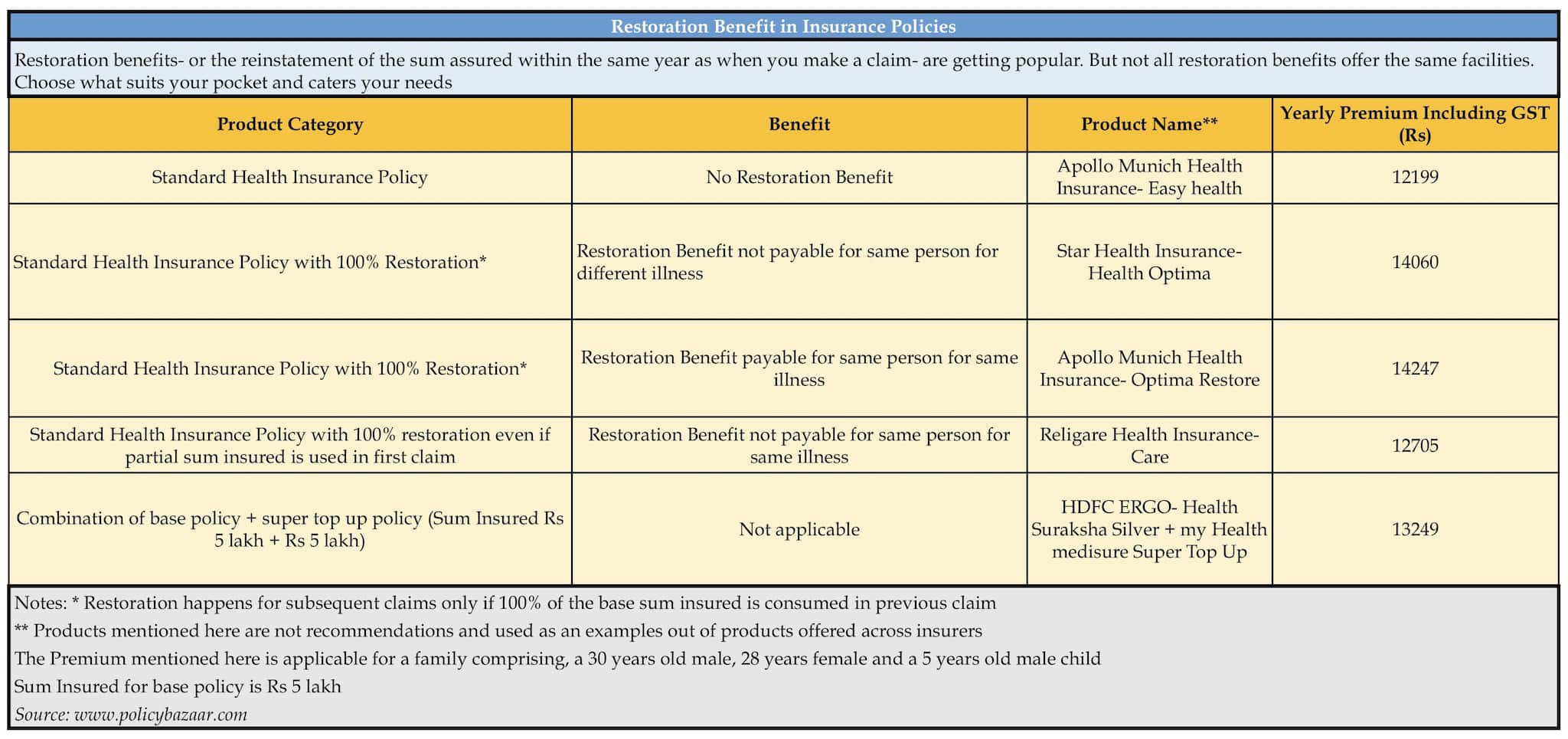

Premium

In any insurance product, more features it offers, more premium it charges. The restoration benefit comes with a marginal increase in premium. The quantum of increase in premium, though, would differ from policy to policy, depending upon the extent of restoration benefit, age bracket of the policy-buyer and other features of the policy. For example, according to PolicyBazaar.com - an online insurance market place, Apollo Munich Health Insurance – Easy Health policy charges an annual premium of Rs 12,199 towards the premium for a sum-insured of Rs 5 lakh for a family floater cover for 30 year male, 28 year female and a 5-year-old male child. This policy does not offer restoration benefit. Religare Health Insurance-Care, which offers the restoration benefit for the same sum-assured, however, charges Rs 12,705 for the same policy.

“If you get a policy with the restoration benefit at the same premium payable on the policy without the restoration benefit, go for the former. It is a no-brainer. But, always remember that the restoration benefit is good to have but not a must-have condition,” says Abhishek Bondia, the co-founder and principal officer of SecureNow.

Sum-assured

The restoration benefit is generally offered to insurance plans above a threshold. The threshold may vary from insurer to insurer. Typically, the restoration benefit is seen on covers in excess of Rs 3 lakh.

Coverage

The restoration benefit comes with a battery of conditions. Most insurers replenish your sum-assured only when the entire sum-insured is exhausted. Some, however, choose to replenish it even if a part of your sum-insured is exhausted. Let’s understand the implications by looking at how the claims are settled.

For example, in the first case where the restoration benefit kicks in when the sum-assured is totally exhausted, the insured person has a cover of Rs 5 lakh, and he claims Rs 4 lakh on account for hospitalisation due to cardiac condition. Later in the same policy year, he is hospitalised on account of an accident and raises a bill of Rs 3 lakh. In this case after his first claim, he has remaining sum-assured of Rs 1 lakh. Hence, the restoration benefit will not kick in. For his accident claim of Rs 3 lakh, he will be paid only Rs 1 lakh.

But, if his insurer has agreed to replenish the sum-assured even if it is exhausted partially, the insured will be paid both claims in the same claims’ scenario above.

Restoration and family-floater

“The restoration benefit is very useful in family-floater insurance policies. Even if one member of the family uses up the sum-assured, other members are not deprived of the health insurance cover,” says Amit Chhabra, business head – health, PolicyBazaar.com. But, he quickly advises that, before purchasing a policy with the restoration benefit on a family-floater basis, do spend some time understanding the limitations defined in the restoration benefit. Do check the broad exclusions the policies define for the restoration benefit.

Many policies do not offer any restoration benefit to the same person again in a given policy year. In other words, the restoration benefit is not available to the family member who makes a claim; it gets available to other family members. Some policies let the same member use the restored sum-assured but for some un-related condition. For example, if the insured person goes for a cancer-related condition and uses the sum-assured and later gets hospitalised again for the same condition, he cannot avail the insurance. But, if he gets hospitalised for some other reason – say for the treatment of injuries arising out of an accident or a cardiac condition not related to his previous ailment, the claim is payable. There are some policies that offer the restoration benefit to the same person for the same illness. Look at the table.

But, even in those cases, do read the fine print. Some policies do allow the coverage for the same person and the same illness with a specified time gap within one year.

No claim bonus

The insurer restores the base sum-assured for the remaining part of the policy year, when you use up your base sum-assured and the accumulated sum-assured arising out of no claim bonus in the past. “Unutilised part of the restored sum-assured cannot be carried to next policy year. Also your no claim bonus gets reduced as per policy conditions once you use your sum-assured. Restoration of sum-assured does not restore your additional sum-assured accrued to you by way of no claim bonus in the past,” says Abhishek Bondia.So should you dump your top-up policies?

Before you decide on top-up policies, understand how they work. A top-up policy pays to the extent of the sum-assured you have bought when the claim amount exceeds the threshold limit called deductible. This rule is applied strictly for each claim.

So let’s say one has bought a base policy of Rs 3 lakh and top up of Rs 10 lakh with deductible of Rs 3 lakh. In this case, if the policy holder incurs three claims of Rs 5 lakh, Rs 2 lakh and Rs 4 lakh, then his base policy will pay for Rs 3 lakh out of the first claim, and top up will pay for Rs 2 lakh. In the second claim, assuming that there is no restoration benefit in base policy, this money will be paid by the policy-holder from his pocket since the claim is less than the deductible amount. In case of the third claim, the top-up will pay Rs 1 lakh after applying the rule of Rs 3 lakh deductible, as mentioned before. In this last claim, since the policy-holder had already exhausted his base policy for his first claim (Rs 5 lakh), only the top-up policy would be available at the time of his third claim (Rs 4 lakh).

But, if the same person goes for a super-top plan, keeping all other things separate, he will see all his claims getting paid by the super top-up policy as the base sum-assured is getting used up in the first claim itself. A point to note that super top-up policies aggregate all the claims to apply the rule of deductible.

“The restoration benefit is available within the same policy which is triggered post exhaustion of base sum-insured and cumulative sum-insured, if any. The restoration benefit is guided by the terms and conditions of the base policy. However, the super top-up is a separate cover which has an aggregate deductible and cover limit. This cover is independent of any base health insurance. The super top-up cover is guided by the terms and conditions of the super top-up policy which might be different from the base cover,” says Punit Sahni.

You cannot have the restoration benefit without a base health insurance policy. But, you can have a top-up plan without a base health insurance policy. If you are a person with sound cash-flows through the year and are willing to take care of hospitalisation claims up to a fixed amount, a top-up plan can be bought to tide over only large expenses. For example, one may buy a top-up cover of Rs 20 lakh with Rs 5 lakh deductible.

“The super top-up is generally designed and bought for high severity exigencies where the frequency of such events is very low and, hence, makes sense for buying a top-up cover at a relatively much lower cost than the base cover. For example, a base cover of 20 lakh vs a base cover of 10 lakh and a super top-up cover of additional 10 lakh, the combination version shall cost approximately 40 percent cheaper,” points out Punit Sahni.

The super top-up covers work the best when there are large claims arising out of one critical illness or allied conditions. The restoration may not come to your rescue, given the way it triggers. Do not dump your top up plan just because you have a restoration benefit in your base health plan. “If you have a family history of critical illness or lifestyle diseases, do not dump top-up plans that have run for a few years. When you have paid for these plans for four-five years, all existing conditions too are covered. Go for top up plans with a deductible amount of Rs 5 lakh. If you have a base health plan with Rs 5 lakh then this combination will take care of you in most cases, whether your base policy offers restoration benefit,” says an actuary who wishes not to be identified.

If you find the restoration benefit and the top-up too complicated, do not just sign up the first product that comes your way. “The best way to understand these product is to ask questions to your insurance adviser. Consider various situations of series of hospitalisation in a family. Understand if the policy will pay the claim, the quantum of claim payable for each of these claims,” says Amit Chhabra.

There are no one-size-fits-all answers here. What works for your neighbour will not work for you. Hence, it makes sense to break down the products and understand how they are expected to deliver in various situations. And, do not ignore the cost attached to it.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.