Placement season is in full swing on college campuses. Understandably that’s the top priority for most students graduating in any year. But once you land a job, you need to be financially savvy, as your first paycheck should not be frittered away. Sure, treat your family and friends, but then let’s get down to business: managing money.

If you are in your 20s, or even in your 30s, and in your first, second or even third job and are just embarking on your financial journey, here are some handy tips to make sure you become financially independent.

Also read | How women in their first job can take control of their money

Set aside a small sum of money from your salary every month to invest in equities. Maher Dhamodiwala, founder of Financial Artists, a Mumbai-based financial planning firm, says that at a young age, when liabilities are low, people should invest up to 60-80 percent of their savings in equities.

“Equity beats inflation over the long term and this is the time in your life (the 20s) when you can maximise your savings through equities,” says Dhamodiwala. The best way to approach your investments is to follow an asset allocation approach. Keep around 60 percent in equities and the remainder in fixed income assets and a small bit in gold.

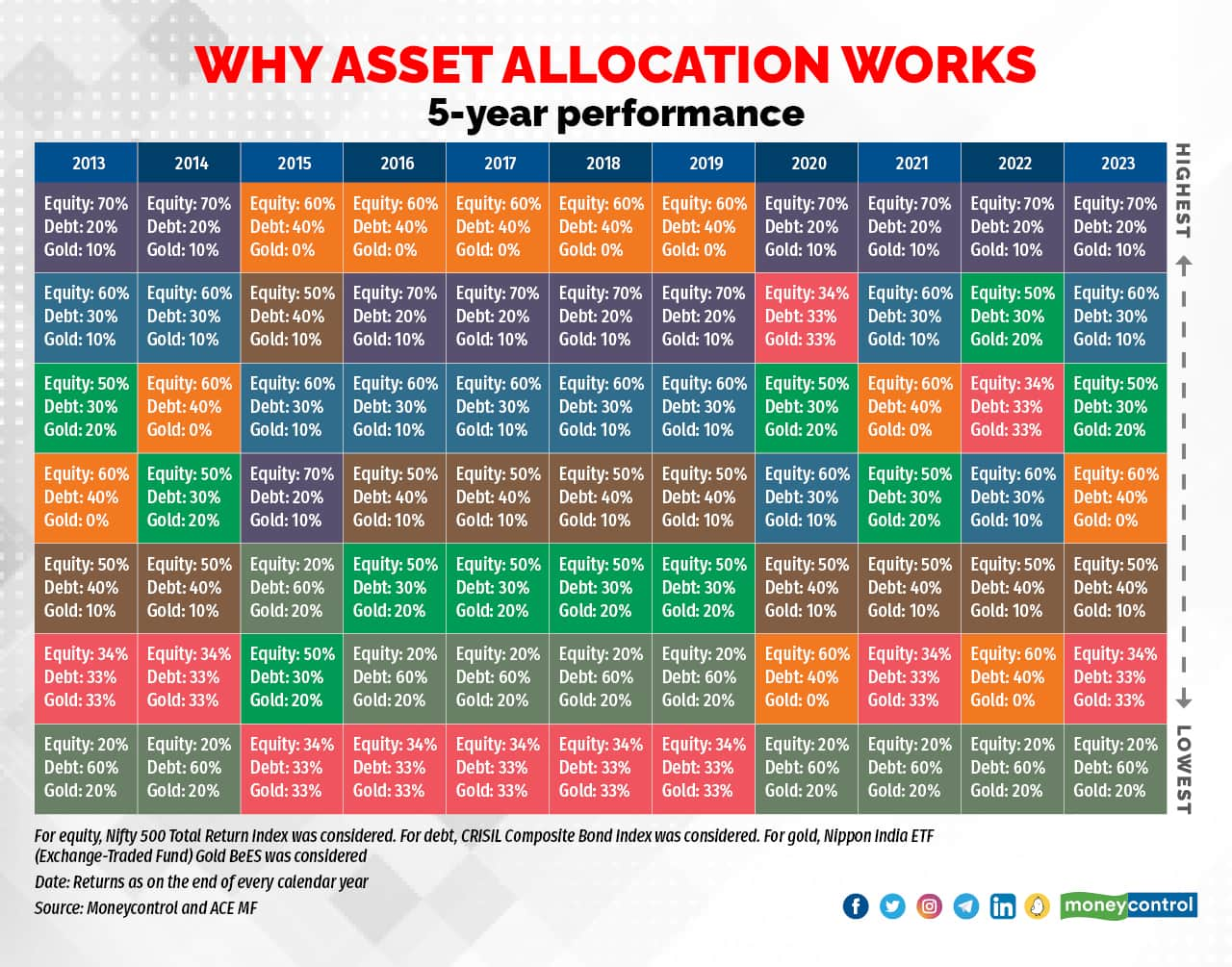

Asset allocation works because it lowers your portfolio risk and makes it in line what you can handle

Asset allocation works because it lowers your portfolio risk and makes it in line what you can handleBut what about those who live in metros such as Mumbai and Bengaluru and have to pay high rents to stay near their workplace or commute to save on rentals? Dhamodiwala agrees that life in big cities can be tough and expensive. There are two tricks to save:

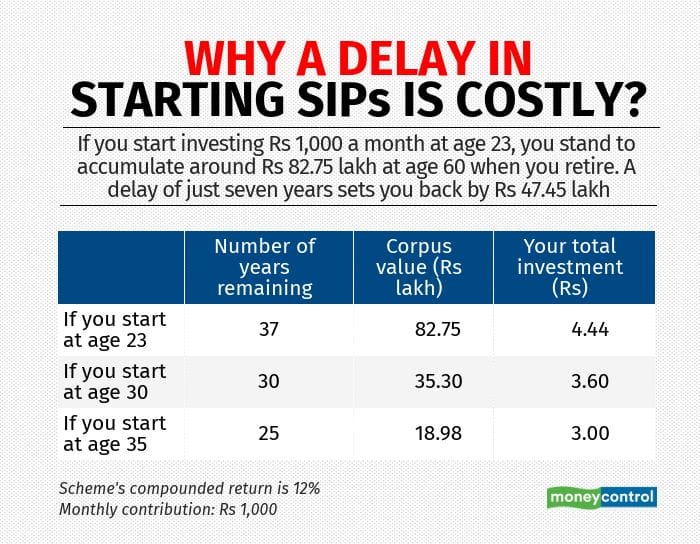

1) Start a systematic investment plan in your mutual fund (MF) with your first, or, at worst, your second salary. This is a facility whereby you make a monthly investment in a MF and it is automated; money goes out of your bank account and into your mutual fund every month. You just have to start the mechanism; thereafter, every month the investment is automated. Start small, if you have other expenses. All mutual funds allow you to invest Rs 500 in a SIP every month. But there is merit in starting early.

<see table>

A delay in SIPs keeps you away from your financial goals

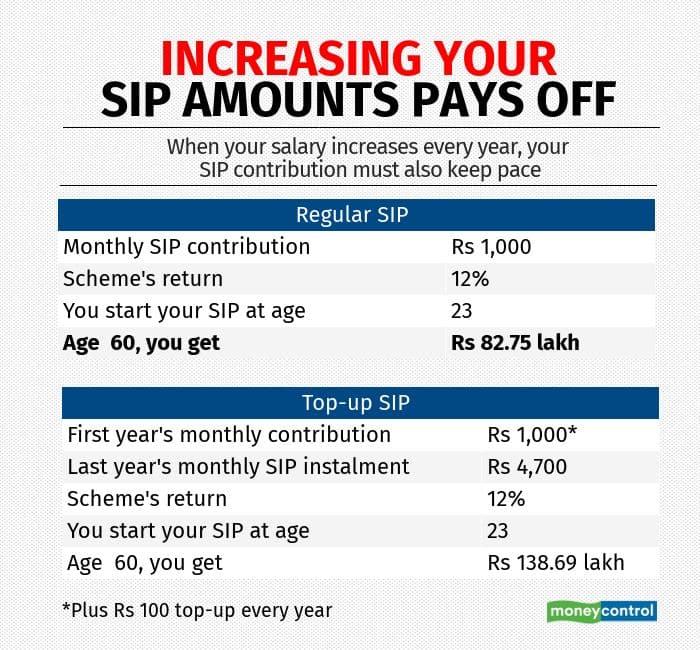

A delay in SIPs keeps you away from your financial goals2) Top-up every year. Since you get an annual increment, a bit of extra money should also be added to your monthly SIP <See table>.

A delay in SIP can be costly

A delay in SIP can be costlyKshitija Shete, cofounder of Gaining Ground Investment Services, advises youngsters to “invest in financial assets and not bricks.” She means that investments at a young age must go towards equities and debt instead of real estate.

“Having funds in hand gives flexibility and confidence to move around, take different job opportunities, relocate to foreign countries and so on,” she says.

Shete reminds that investing in real estate at a young age binds you to a property and makes it difficult for you to move into a bigger property as your family expands or if you have to shift locations.

Spend, but do not overspendYou experience financial freedom in your 20s and 30s when you start earning your first pay cheques. But keep your spending on a leash, say financial planners.

Viral Bhatt, founder of Money Mantra, a personal finance solution firm, says that he has observed that youngsters spend a lot on luxury items. Many of these spends are impulsive, which is bad if you do it often. “Spend only if you really need luxury items. It’s okay to spend, but it is dangerous to overspend,” he says.

Excessive spending also leads to borrowing. With online fintech firms and neo-banks mushrooming all around us, small-ticket loans are available for holidays, paying rent and so on. But these are expensive loans, which, when bunched up over time, can burn a big hole in your pocket. And they damage your credit score.

“Some of the ways to keep your debt under check can be avoiding the use of buy-now-pay-later kind of options, and personal loans to fund discretionary spending,” says Prableen Bajpai, founder of FinFix.

But is all borrowing bad? Suresh Sadagopan, founder of Ladder7 Financial Advisories, says that there are exceptions. “Borrowing for education is fine as it enhances one’s prospects in one’s career. Loans for a residential home at a serviceable level are fine somewhat later in life, when one has decided where to settle,” says Sadagopan. His warning: “Do not use credit cards for conspicuous consumption like buying a mobile, vacation and so on. Never get into a situation of going into revolving credit payments vis a vis credit card dues. If you refrain from frivolous borrowing, you will be well on the road to achieving financial freedom.”

Emergency fundOne way to be financially free is to let your investments grow and not keep touching them regularly. One of the surest ways to let your investments grow is to have an emergency corpus. This is a small pot of money that you keep aside for emergencies or contingencies.

Bhatt says you need to have a corpus of at least 3-6 times your monthly salary or monthly expenses. Bajpai suggests that along with your regular systematic investment plan (SIP), which goes into equity funds for long-term goals, invest in debt funds to build an emergency corpus. And have a separate corpus for “big purchases and fun activities”, says Bajpai.

An emergency or contingency corpus helps if you, say, lose a job or even take a sabbatical. That’s when your monthly salary stops but your expenses continue. Rentals, EMIs, insurance premiums, children’s school fees, grocery and utility bills must be paid. Your contingency fund should be big enough to meet such non-negotiable expenses when your salary stops.

Buy insurance today

Health insurance is just as important. This insurance pays your bills in case of sickness and hospital admission.

You could meet your hospitalisation expenses with your savings. But once you dip into your savings, the amount goes down by that extent and it can take years to replenish it. On the other hand, if your health insurance foots the bill, your outgo will be very low, should you be hospitalised.

Also read | How to optimise personal health insurance when you already have an office-provided cover

“Personal medical insurance is a must-have even if your employer provides you insurance. Include your parents wherever possible in your insurance cover. This is important as the employer cover will be available only during the tenure of your employment. If you go on a sabbatical or leave your job to launch a startup, a personal cover will be invaluable. Also, every employer cover may not be equally good,” says Sadagopan.

Tip: Stay away from life insurance policies that agents push you to buy to save tax and get a “handsome return”, especially during the tax-planning season. These policies give returns of less than 6 percent and don’t yield much.

Make a financial planOnce you take care of the basics, it’s time to make a financial plan.

Dhamodiwala says that it’s best to keep things simple. Make a list of your long-term financial goals, decide how much money you need to achieve them, and then work backwards to decide how much you need to set aside every month. He says it is important to think long-term here and not get swayed by short cuts.

“Avoid cryptocurrencies. A few of my young clients have invested in cryptocurrencies and are now sitting on huge losses because of the troubles in the crypto world,” he says.

Also read | Millennials and cryptocurrencies: A story of missed profits, hard lessons and missed profits

Sadagopan says that it’s important to set aside at least 10 percent of your take-home salary to meet your long-term financial goals, to begin with. “This can be slowly hiked to 30 percent and even more,” he adds.

A good mutual fund distributor or a Securities and Exchange Board of India-registered investment advisor is a useful guiding hand to help plan your finances. If you cannot find one, there are online platforms that give you packaged portfolios tailored for various types of financial goals.

But over time, make sure you find an advisor to guide you in person through the market’s ups and downs.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.