Note to readers: No two people’s financial plans can ever be the same. Our income, expenses, goals, aspirations and financial obligations differ. But the first principles are more or less common, depending on your age bracket. Moneycontrol personal finance’s new series called ‘Life stage financial planning’ will tell you what these broad principles are, depending on whether you are in your 20s, 30s, or 60s. Today’s story is about how to plan your finances when you get to your 30s. That’s when you leave the fun part of your 20s behind and get serious about money management.

When you enter your 30s, you should pay close attention to your finances. In your 20s, you would have got your first job and salary. You may have spent on buying new clothes, eating out, socializing, and some travelling, basically focusing on having a good time. But the 30s mark a new phase of your life. Hopefully, you are settled in your job and career – your salary may have increased substantially. Many in their 30s also typically look to get married, perhaps expand their families and buy a house. It is not just your finances that you need to take care of now. You are also, in a way, responsible for your spouse’s finances. Elsewhere, your parents are also getting older, perhaps close towards retirement, if not already retired. You need to take care of them, as well. Your responsibilities just increased. It’s time to get serious. Here’s what you need to do.

For years, financial advisors have advocated the need to have an emergency corpus. The onset of Covid-19 emphasized the need for it. Many people lost their jobs as companies’ cut back on their employee cost on the back of low sales and reduced profitability. Self-employed people also saw a drastic fall in their income. Here’s where an emergency corpus comes in. This kitty must hold an amount that’s worth 12 months of your living expenses. In times like these when you lose your job suddenly, your emergency corpus comes to your rescue. Apart from your food and grocery bills that you can’t just avoid, your emergency corpus should also be enough to help you pay your monthly rent, insurance premiums and all the loan instalments you’ve committed to.

Health insuranceAlthough your 20s were the best time to buy your health insurance, you won’t be too late doing so even now. Your office-given insurance cover is not enough. Buy your own cover too. “Your parents are getting older. Think of buying an insurance cover for them as well. Most of our parents have old-time insurance covers of around Rs 1-3 lakh, which in today’s times is not enough,” says Varun Girilal, Co-founder and executive director, Mitraz Investment Advisors. Varun also recommends opting for an additional insurance cover if your employer offers, even if you have to shell out extra premium. “Some firms offer insurance covers that cover your parents, which is helpful,” he adds.

Do you need to own a house?Perhaps the biggest question for someone in her 30s is to buy a home or not. That is because this is the age when most get married and expand their families, the need to buy a house is most felt in this age group. But should you rent or buy?

Raj Khosla, Founder, MyMoneyMantra says that “today is as good a time as any to buy a house. ”Home loan rates are almost at their historic lows and property prices have also been sedate for a few years now.” He says that if you are sure of staying at a place for the next 10 years at least, then now is the best time. “Else, if you think you might want to sell your house after 3-4 years, do not buy. But make sure all your EMIs combined do not exceed 50 percent of your take-home pay,” adds Raj.

Despite home loan rates being at their lowest, you still have to pay your equated monthly instalments (EMI). Varun states the tale of one his clients who is a doctor who runs a hospital. Due to COVID-19, his hospital – which is not a COVID-19 centre – has been shut since the lockdown was declared in March. Despite the massive drop in his income, the client still has to pay his housing loan EMI.

Suresh Sadagopan, Founder of Ladder7 Financial Advisories, explains in his recently-released book ‘If God Was Your Financial Planner’ that the cost of your house is not the price you pay to buy it. It also includes the massive interest cost on the housing loan you’d be repaying over the next, say, 15-20 years. “A home loan EMI is one of the biggest obstacles for many other dreams a person can have,” says Varun.

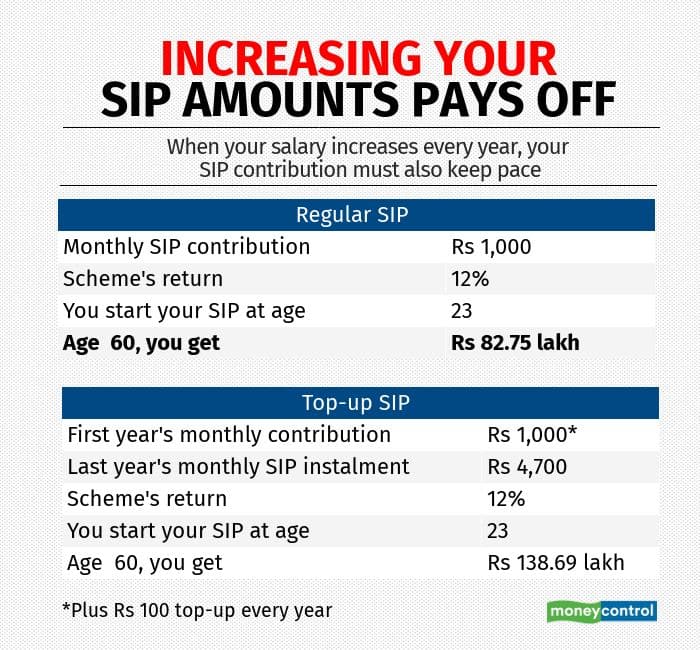

Go aggressive on equitiesIdeally, you should start saving up when you are in your 20s. But if you hadn’t started your systematic investment plan (SIP) in a mutual fund (MF) scheme, then now’s the time. You need equity and debt in your portfolio. But, as you have a long way to go before you retire, you can afford to invest aggressively in equities. “By your early or mid-30s, if you do not have close to Rs 10 lakh in your portfolio, then you must start investing in equities immediately. A good corpus in your kitty by the time you turn 40, enables you to have alternative lifestyles – starting a business, getting into farming etc. – where you need some cushion in the initial years and so on,” says Kartik Jhaveri of Transcend Consulting. Varun says, “If there is an age where you can afford to take risks, it is your 30s.”

Karthik says that a few years ago, people used to aspire retiring at 50. But today’s millennial doesn’t want to wait till 50. He says today’s youth aspires alternative lifestyles such as starting firms, way early. For this, he says, a good corpus is required and that comes through early and disciplined investing. Don’t just start SIPs. Invest lump-sums too – your annual bonus or at least a part of it.

Varun advises automating your investments and SIPs are just the way to do that.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.