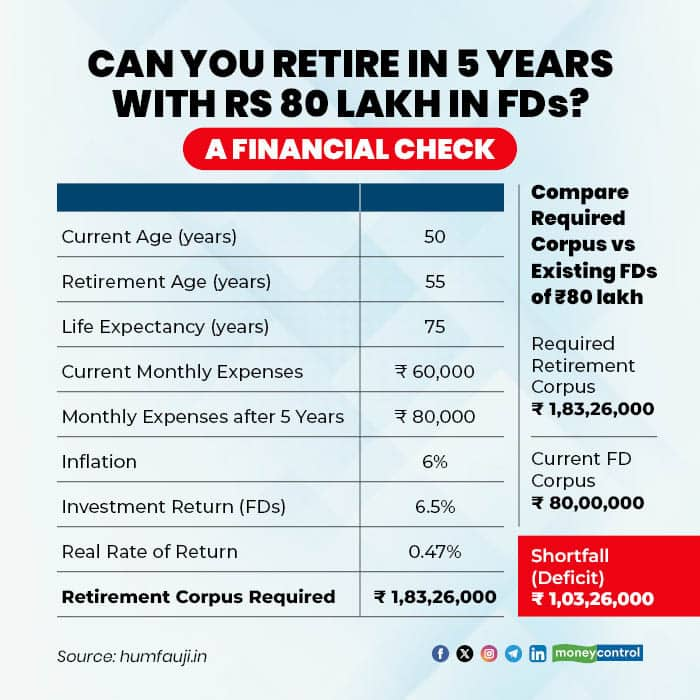

Imagine turning 55 with dreams of travel adventures and peaceful retirement, only to watch your savings dwindle faster than expected. For a 50-year-old investor with Rs 80 lakh parked in fixed deposits (FDs) and current monthly expenses of Rs 60,000, retiring in five years sounds tempting but is it feasible?

With inflation at 6 percent and life expectancy stretching to 75 or beyond, experts warn that safety nets like FDs may not be enough.

Let’s look at investment strategies and safeguards needed for a secure retirement.

Projecting expenses: Inflation's hidden toll

Retirement planning starts with being real. Today's Rs 60,000 monthly spend — covering essentials such as groceries, utilities and leisure — will balloon under 6 percent inflation.

Monthly expenses at 55 will increase to Rs 80,000. “This is the revised baseline amount required every month at the start of retirement,” said Sachin Jain, Managing Partner, Scripbox. This jump underscores how costs compound — food, healthcare, and fuel don't stay static.

To sustain Rs 80,000 monthly for 20 years (ages 55 to 75 years), assuming a 6.5 percent FD return barely outpacing inflation, the required corpus hits Rs 1.83 crore.

“A meager 0.47 percent return after inflation and taxes, meaning your money fights just to hold ground,” said Col Sanjeev Govila (retd), CEO of Hum Fauji Initiatives, a financial planning firm.

The Rs 80 lakh corpus covers only 44 to 46 percent of retirement needs, risking premature depletion and potential exhaustion by age 70, Govila said.

The FD Trap: Why Rs 80 lakh falls short

FDs promise 6 to 7 percent yields but taxes erode them to 4.5 percent for high earners, trailing inflation. Over five years, Rs 80 lakh grows to about Rs 1.13 crore — impressive on paper, yet deficit of roughly Rs 70 lakh against the Rs 1.83 crore target.

The math is unforgiving. With expenses rising annually and returns stagnant in real terms, withdrawals accelerate corpus shrinkage. “A 7 percent FD might fund initial years but by decade's end, inflation outruns interest, risking a shortfall mid-retirement,” said Jain.

Also read | SIP of Rs 10,000 from your savings account or an STP from a Rs 1.2 lakh liquid fund- which works better?

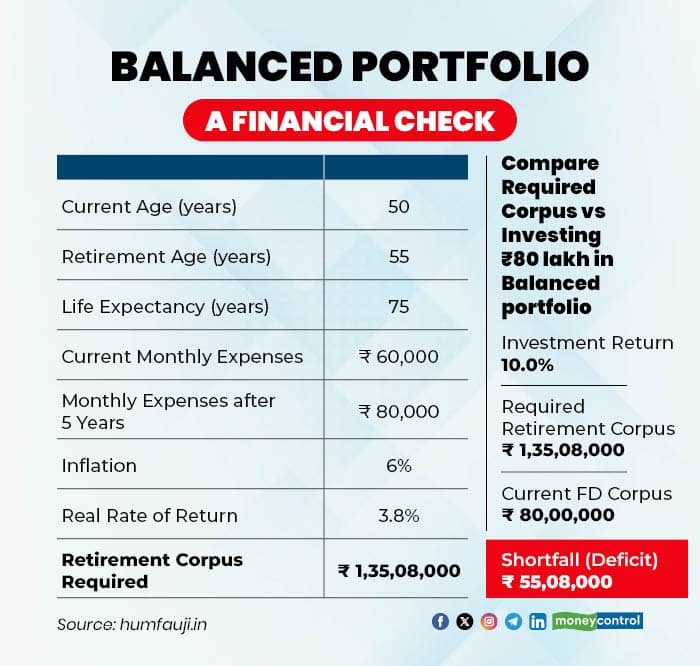

Diversifying to Grow: Beyond FDs in five years

To close the gap, shift from FD isolation to a balanced portfolio targeting 9–11 percent returns. "A well-diversified investment strategy—combining safety, stability, and growth," Govila said.

Jain favours allocating to equity mutual funds for growth and debt/bonds for stability. Achieving this higher blended return is essential for meeting the retirement corpus target within the available timeframe.

“Debt and hybrid mutual funds can outperform FDs on a post-tax basis, especially if held for more than three years, due to lower long-term capital gains tax and slightly higher returns,” said Govila.

However, this approach comes with risks such as equity market volatility, interest rate fluctuations and emotional reactions during market corrections.

With a balanced portfolio, the deficit reduces to Rs 55 lakh from Rs 1.03 crore. This remaining gap can be comfortably managed by starting regular SIPs or by gradually investing any additional surplus for this goal over the next five years.

Sustaining the Corpus: Withdrawal wisdom

A Rs 1.83 crore nest egg demands discipline. Jain recommends withdrawing only 3 to 4 percent of the corpus annually to avoid depletion. At 3.5 percent withdrawal rate, Rs 1.83 crore yields Rs 51,000 monthly — below inflated needs — so trim luxuries or boost corpus.

Govila advised keeping part of savings invested in growth assets like hybrid or equity funds to help the corpus grow and beat inflation. He recommended a bucket strategy: Bucket 1 (0-5 years) for immediate expenses in FDs and liquid/debt funds, Bucket 2 (5-10 years) in hybrid funds for medium-term needs, and Bucket 3 (10+ years) in equity or hybrid funds for long-term growth.

Rebalance yearly, keep 20–30 percent in growth assets post-retirement. This combats longevity risk — living past 75 — and rising medical costs.

Also read | Silver prices at all-time high this week: Should you buy, hold, or sell?

Contingency shields

Life is unpredictable and unexpected events like market crashes, health crises, or inflation surges can happen. Building buffers can help you navigate these challenges.

To counter this, the investor should maintain separate reserves for short-term expenses, medium-term needs, and long-term wealth generation. Jain said, "This layered approach ensures immediate expenses are met without liquidating growth investments at the wrong time, while allowing other funds to continue compounding."

Start with an emergency fund (three–six months' expenses in liquid funds). Secure health insurance — family floater plus super top-up — to shield against Rs 5–10 lakh hospital bills.

“Adequate health insurance (family floater) and critical illness cover reduce the risk of large, unplanned withdrawals from your retirement corpus,” said Govila.

Act now for tomorrow's peace

Retiring in five years with Rs 80 lakh in FDs requires urgent action, as a deficit of over Rs 1 crore is likely without diversification. By combining safety and growth investments, aiming for 3 to 4 percent withdrawals, and preparing for contingencies, it's possible to make the corpus last until age 75 and beyond.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.