The defaults on bonds held by mutual funds (2018-19) and also the closure of six debt schemes by Franklin Templeton last year, resulted in SEBI issuing guidelines for assessing risks in funds. Last year, the market regulator revised the risk-o-meter that all mutual funds disclose. Then, earlier this month, it asked debt funds to define the boundaries within which they will limit the risks they take.

What do these new means of gauging risks mean for investors?

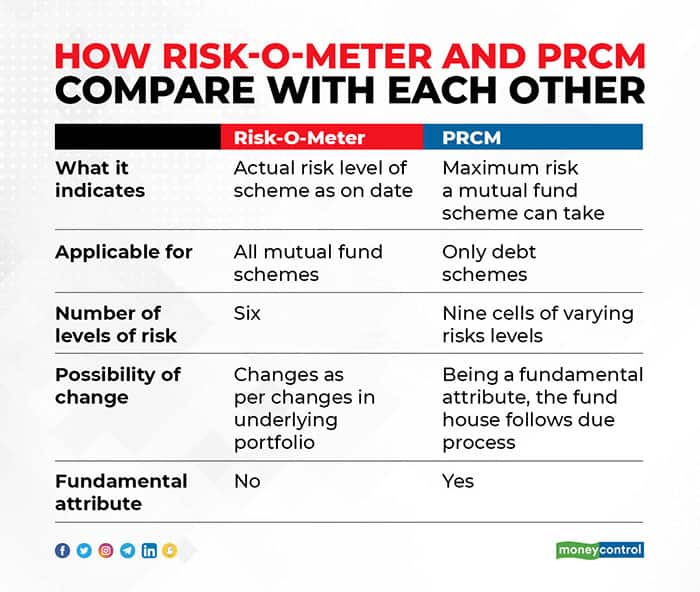

Varying levels of risksThe risk-o-meter places mutual fund schemes across six different categories of risks – Low risk to Very high risk. The Potential Risk Class Matrix or PRCM places debt funds into nine different cells – each one of these define the maximum risk a scheme can take.

Both the approaches are rule-based and depend on the weightage of a security in the portfolio and the risk attributes it carries. “While a lot is talked about investors’ risk appetite, SEBI has taken steps to define the risk levels associated with mutual fund schemes by putting in place revised risk-o-meter rules and PRCM framework,” says Rupesh Bhansali, Head-Mutual Funds, GEPL Capital.

Which factors decide the level of risk?Credit risk, interest rate risk and liquidity risk are considered for securities held by a debt fund. Each of the bonds is assessed on these parameters and depending upon their weighted average in the portfolio, the scheme is placed in one of the six risk-o-meter indicators.

For stocks held, market capitalization, volatility and impact costs are considered to assess the risk. Risk-o-meter also specifies the methodology for evaluating risks related to derivatives, gold, cash and cash equivalent and units of mutual funds and REIT held in the scheme’s portfolio.

PRCM is meant for only bond funds and uses interest rate risk measured by Macaulay duration and credit risk. Depending on varying levels of these two risks – schemes are placed in nine cells starting from Class A1 (least credit risk and least interest rate risk) to Class C3 (relatively high credit risk and relatively low interest rate risk).

“The circular on PRCM lays down the maximum maturity of individual securities. For funds with interest rate risk or volatility risk Class I, which is portfolio duration of less than one year, the maximum residual maturity is three years. For a fund in Class II, i.e., duration less than three years, the maximum maturity is seven years,” wrote Joydeep Sen, Corporate Trainer- Debt, in his Moneycontrol column.

By defining the maximum maturity, the regulator has restricted the fund manager’s ability to deploy interest rate sensitive strategies.

“While a PRCM can be instituted for equity or hybrid funds in future, if need be, there are reasons for starting with debt funds. In debt, it is more structured – numbers can be assigned easily for maturity or duration, credit rating and can be represented as a square in the matrix,” says Sen.

Bhansali expects SEBI to roll out PRCM rule framework for non-debt funds in future.

Risks that MFs can takeThe risk-o-meter may change with the underlying portfolio of the scheme. Changes in credit rating and duration of the underlying bonds, too, get reflected in the risk-o-meter of the scheme. A scheme may see improvement in risk rating over a period of time, other factors remaining the same.

If the fund manager takes additional risk, the risk-o-meter will clearly reflect that. Hybrid funds may show noteworthy changes in the risk-o-meter with modifications in the portfolio.

“Though scheme categorization has defined asset allocation for funds, there is scope for deviations. Such deviations may be captured by the risk-o-meter and investors can compare two schemes in one category on the basis of risks involved,” says Vinayak Savanur, Founder and CIO at Sukhanidhi Investment Advisors.

A scheme placed in a cell of PRCM has to clearly indicate the maximum risk it can take. Actual risk involved may even be less than what was depicted by the PRCM placement of the scheme.

Fundamental attributeRisk-o-meter is a part of the product labelling guidelines of SEBI. However, the risk category can keep changing and it is binding on a fund house to keep updating investors on such changes through email and by publishing it on its website.

A change in the PRCM cell, however, is treated as a fundamental attribute of the scheme. And any change in fundamental attribute means that the fund house allow load-free exit to investors after following the due process of filing the change with SEBI.

Though risk-o-meter and PRCM differ from each other, they work on the single goal of offering more information to investors pertaining to risk. This rule-based approach may initially be seen as a regulatory overreach by a few. But this move should increase the confidence of the investors in mutual funds.

Savanur asks investors to compare their risk appetite with the risk-o-meter rating of the schemes held in their portfolio, to avoid any negative surprises in future.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.