SEBI has decided to cut mutual fund base expense ratios making investing cheaper and more transparent for retail investors. The cut may look small at first glance, but it decides how much of your money actually stays invested instead of being eaten away by costs. Over time, that difference quietly adds up.

Under the new rules approved at SEBI’s board meeting on Wednesday, December 17 2025, expense ratios have been reduced by up to 15 basis points, with most asset slabs seeing a 10 basis point cut. For open-ended equity funds with assets below Rs 500 crore, the maximum charge has been lowered from 2.25 percent to 2.10 percent, while debt funds in the same category will now be capped at 1.85 percent .

List of updated MF Expense Ratios

1. Index funds/Exchange Traded Funds (ETF)

Current (Including statutory levies) — 1.00 percent

Revised (excluding statutory levies) — 0.90 percent

2. Fund of Funds (FoFs)

Funds investing in liquid schemes/index funds/ETFs

Current (including statutory levies) — 1.00 percent

Revised (excluding statutory levies) — 0.90 percent

Funds investing ≥ 65 percent of AUM in equity-oriented schemes

Current (including statutory levies) — 2.25 percent

Revised (excluding statutory levies) — 2.10 percent

Other FoFs

Current (including statutory levies) — 2.00 percent

Revised (excluding statutory levies) — 1.85 percent

What Exactly Has Changed

SEBI has also simplified how these charges are shown to investors. The Total Expense Ratio (TER) has been renamed the Base Expense Ratio (BER).

“Earlier, investors tracked costs through the Total Expense Ratio (TER), which combined multiple expense components into a single figure. The move to a Base Expense Ratio (BER) separates core fund expenses from statutory levies, making the cost structure easier to understand and monitor over time,” says Niharika Tripathi, Head of Products and Research at Wealthy.in, a wealth management platform.

The BER will now include only the costs of running the fund, such as fund management fees, distributor commissions, and registrar and transfer agent (RTA) charges. Statutory costs like GST, stamp duty, Securities Transaction Tax (STT), Commodity Transaction Tax (CTT), and regulatory or exchange fees will be kept outside the BER and shown separately.

In simple terms, BER reflects what the fund house charges, while TER represents the final cost an investor pays after adding taxes and statutory levies. The revised limits apply across equity-oriented schemes, debt funds, index funds, ETFs, fund of funds, and closed-ended schemes.

Why A Small Cut Can Still Matter

So what does this mean for an investor’s savings?

SEBI’s move to lower expense ratios by 10-20 basis points may appear marginal, but its impact builds quietly over time.

“On the surface, a 10-20 bps cut looks negligible. But investing is not a sprint; it is a long, steady march. When these costs come down, more of your invested money stays invested and compounds more,” explains Col Sanjeev Govila (retd), Certified Financial Planner, CEO, Hum Fauji Initiatives, a financial advisory firm.

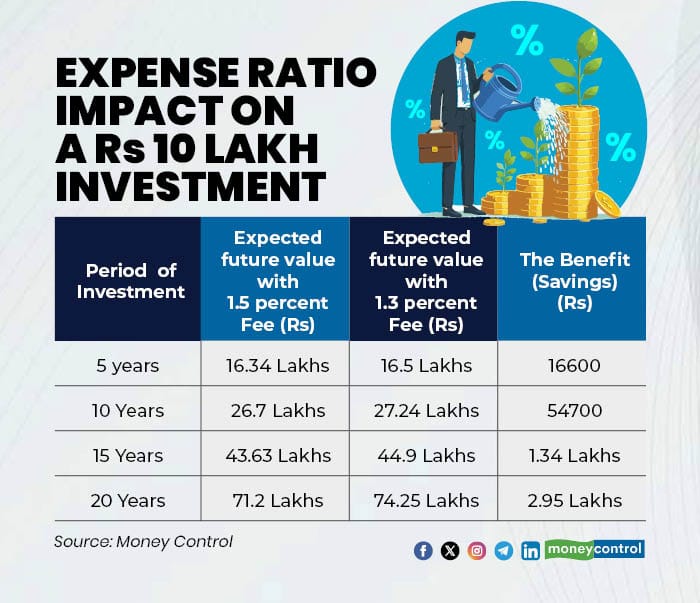

Let’s understand this with an example. Here is the impact on a Rs 10 Lakh lump sum investment growing at a hypothetical 12 percent CAGR (pre-expenses):

A 20-basis point reduction in expense ratio on a Rs 10 lakh portfolio over a 20-year period can translate into nearly Rs 2.95 lakh of additional wealth. This amount represents the net gain for the investor, arising purely from lower costs.

Govila points out, “It is not an incremental return generated by market performance, but money that remains invested and compounds over time instead of being deducted as expenses. In essence, it is a direct saving that converts into higher long-term earnings through compounding.”

Also read | Will home-loan relief continue in 2026 after 125 bps repo rate cuts in 2025?

The Long-Term Effect

Govila adds, “Every rupee saved from fees is an extra bullet available to fight the ‘demon’ of inflation. And these small numbers gain a bigger halo if we look at a 20bps cut as a 10-15 percent cost cut.”

In the short term, these savings are barely noticeable. But over long holding periods, they steadily improve outcomes. Over decades, such “small” reductions can make a meaningful difference to long-term goals.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.