The year 2025 brought relief for home-loan borrowers. After almost five years, the Reserve Bank of India (RBI) set into motion a rate-cut cycle, which brought down the repo rate to 5.25 percent from 6.5 at the start of the year.

In October 2019, banks linked floating-rate retail loans, including home loans, to an external benchmark, which is repo rate for most banks. Any changes to the repo rate directly affect the interest rates on these loans. When the repo rate is cut, borrowers benefit from lower rates and when it is raised, their interest burden increases.

Let's break down the RBI's rate cuts from February to December and their impact on the borrower.

February: Cuts repo rate to 6.25%, signals cheaper loans ahead

The RBI kicked off 2025 with a rate cut in February, slashing the rate from 6.5 percent to 6.25 percent, paving the way for lower interest rates and equated monthly instalments (EMIs).

It cut brought a welcome relief for those struggling with EMIs.

The last time the RBI's monetary policy committee cut rate was in May 2020, when it lowered it to 4 percent to cushion the economy from Covid-19's impact. Since May 2022, it hiked rates seven times to 6.5 percent to tackle inflation and global price surges and maintained a pause since February 2023.

April: Repo rate reduced to 6%, EMIs get cheaper

The second rate cut, 25 bps again, came in April, bringing down the repo rate to 6 percent, further easing EMI burden and making loans more affordable. Home loan borrowers cheered, and investors also welcomed the favourable environment.

June: RBI goes big with 50 bps cut

The RBI slashed its policy rate by 50 basis points in June in its third reduction of the year and MPC shifted its stance from "accommodative" to "neutral". Banks passed on the benefit to customers, offering concessions on home loans.

August and October: Status quo

In August and October, the RBI held the repo rate steady at 5.5 percent. Though there was no cut, its earlier moves kept things comfortable for borrowers.

Also read | HDFC Bank cuts FD interest rates on deposits up to Rs 3 crore- Check the latest RoI

December: RBI cuts repo rate by 25 bps

In its last policy review of 2025, the RBI cut the repo rate for the fourth time, bringing it down 5.25 percent.

The MPC lowered the repo rate by 125 bps in 2025, with four cuts making home loans cheaper and EMIs more manageable.

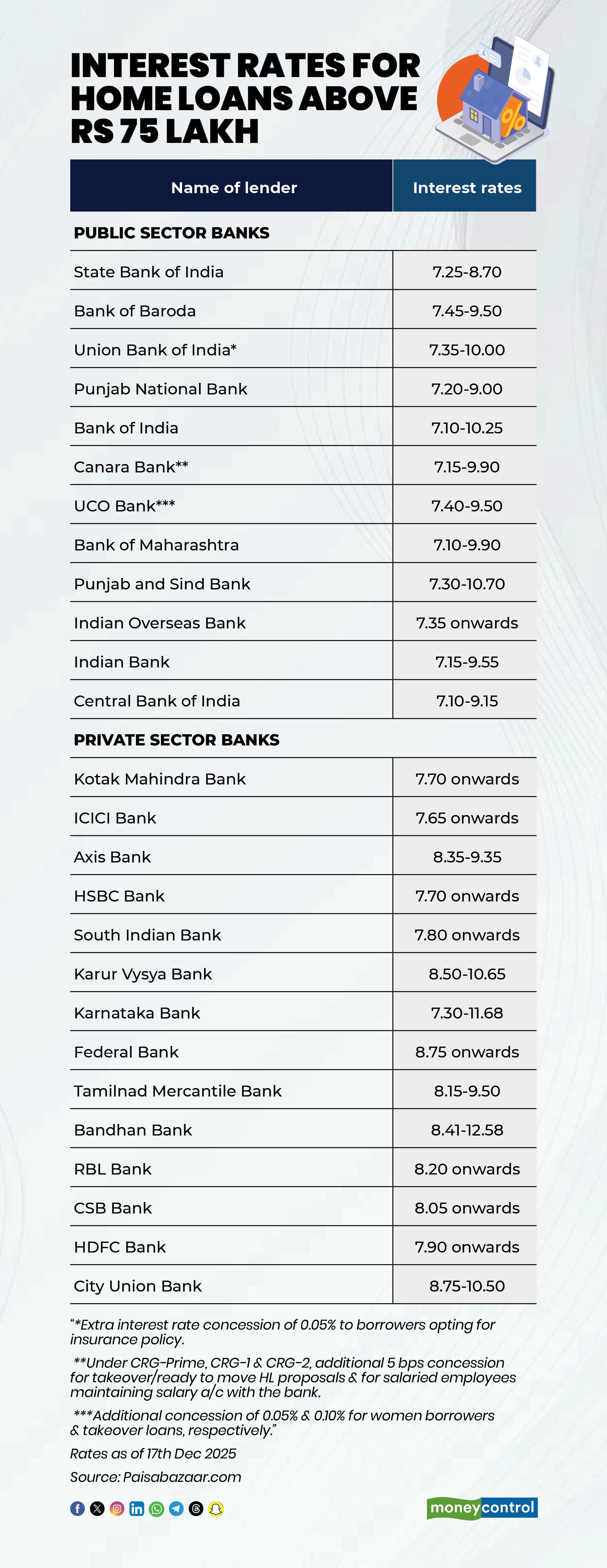

Bank of India, HDFC Bank, ICICI Bank, State Bank of India (SBI), Bank of Baroda and Canara Bank are offering home loan at rates starting at 7.1-7.9 percent.

Impact on existing borrowers

With the RBI lowering the repo rate, home loan interest rates and EMIs fall too.

Typically, unless explicitly asked, banks keep EMIs unchanged after repo rate revisions but shorten tenures.

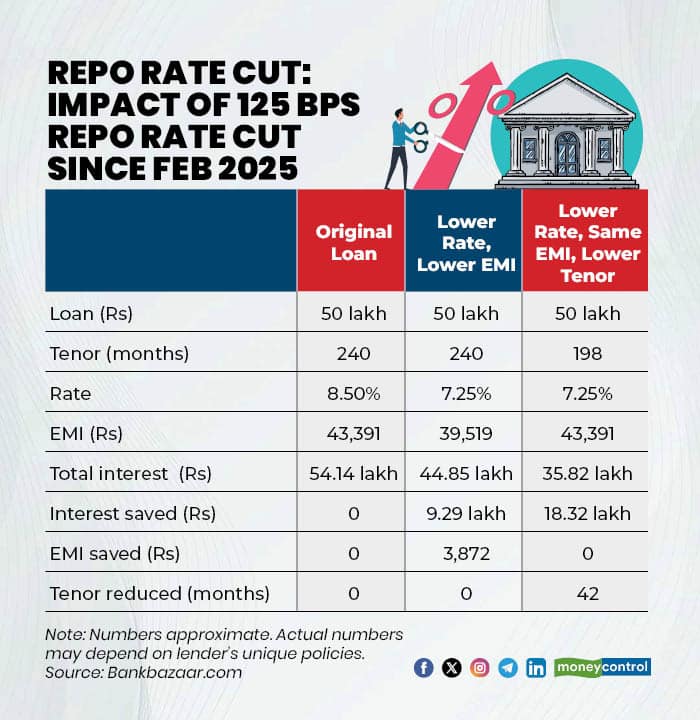

For instance, if your Rs 50 lakh, 20-year home loan at 8.5 percent interest was disbursed in January, you would have gained significantly from 125 bps reduction. It would have shorten your loan tenure to 198 months and saved your around Rs 18.32 lakh in interest payments.

If you chose to reduce the EMI amount, your interest savings would be relatively lower. You would have saved around Rs 9.29 lakh.

New vs existing borrowers

A comparison of home loan rates on January 31 and December 17 shows that most public sector banks have reduced rates for fresh home loans by 125 bps, in line with the RBI's decisions.

Some private sector banks have not transmitted the entire benefit to new borrowers, choosing to adjust the spread over the repo rate instead. For instance, ICICI Bank’s lowest rate for new borrowers was 8.75 percent in January. This has reduced by 110 bps to 7.65 percent, according to Paisabazaar data as on December 17. Similarly, Axis Bank reduced rate by 35 bps to 8.35 percent and HDFC Bank by 45 bps to 7.9 percent.

Borrowers with existing loans at high interest rates may benefit from switching to repo-linked products, which can help reduce interest costs over the long term, financial advisers says.

In home loan transfer, some charges are levied by your current lender and some by the new one.

“Your current lender may charge document handover charges. The new one may charge loan processing fee as a percentage of the loan amount, plus small absolute amounts for legal, valuation, and registration charges,” said Anuj Kesarwani, Founder of Zenith Finserve.

“A loan transfer makes sense only when interest savings over the remaining tenure clearly outweigh processing, legal, and conversion costs,” said Kirang Gandhi Pune-based Financial Mentor.

Interest rate outlook for 2026

RBI governor Sanjay Malhotra has told the Financial Times that he expects interest rates to remain low for a "long period", as the economy remains robust and could receive a boost from trade deals with the US and Europe.

“If the GDP growth continues and inflation remains low, then we may even see the RBI cutting interest rates further,” said Kesarwani.

A section of economists expects the RBI to cut rates by 25 bps in February. "With inflation expected to be around 3 percent in the next 12 months, the current real rate is still higher than the RBI's neutral real rate of 1.4 to 1.9 percent. This suggests the rate-easing cycle may continue," Bandhan Bank chief economist Siddhartha Sanyal said.

While the RBI signals a focus on monetary transmission, given the growth and inflation dynamics, an additional 25 bps rate cut is expected in this cycle, particularly if global trade slows down, Nuvama Institutional Equities has said in a report.

“With 2026 likely to remain borrower-friendly due to stable or softer interest rates, disciplined borrowers should focus on reducing tenure, improving cash flow, and timing refinancing wisely, not reacting emotionally to every small rate cut,” Gandhi said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.