If you follow personal finance content closely, you’ve probably come across the 15×15×15 SIP rule.

The idea is simple: invest Rs 15,000 a month, stay invested for 15 years, and assume annual returns of 15 percent to build a corpus of around Rs 1 crore.

It sounds practical, achievable and, frankly, reassuring. No complex spreadsheets, no constant portfolio tweaks, just one neat formula that promises clarity and certainty. But this is where things start to get complicated.

Several investors who follow the rule diligently still end up disappointed, not because they lacked discipline but because the returns falls short of promise.

The biggest risk to the 15×15×15 rule isn’t market volatility but the assumptions it makes.

The rule works beautifully on paper, calculator or whatever is your device of choice . Real life, however, doesn’t operate on clean averages. Markets fluctuate, returns vary, inflation chips away quietly and risk doesn’t always reward patience the way we expect.

This isn’t about dismissing the rule entirely. It does have value but it’s important to understand where it starts to fall apart.

Let’s break down the three flaws that are often overlooked.

15% annual return is the exception, not the Rule

Let’s start with the biggest assumption: 15 percent returns for 15 straight years.

On paper, Rs 15,000 invested a month for 15 years at 15 percent CAGR does get you close to Rs 1 crore.

But markets are not known for consistency.

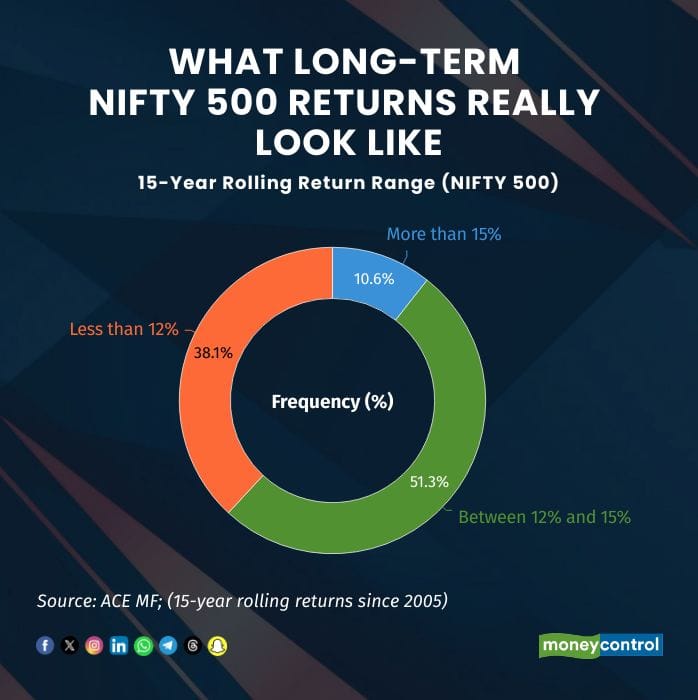

When we looked at 15-year rolling returns of the Nifty 500 since 2005, the picture changed quickly:

Returns exceeded 15 percent CAGR only about 10.6 percent of the time.

Nearly 40 percent of the time, returns were below 12 percent.

Even well-managed, diversified equity mutual funds, often held as long-term core investments, have delivered around 11-13 percent on average, not the promised 15 percent.

Now here’s where this stops being abstract.

If your returns are 12 percent instead of 15 percent, your final corpus after 15 years isn’t Rs 1 crore. It’s closer to Rs 75 lakh.

That’s a Rs 25 lakh gap, created not by bad decisions but by optimistic assumptions.

What this means for investors: If your plan works only when everything goes perfectly, it’s not really a plan. Even a small drop in returns can derail your long-term goals if you don’t account for them from the start.

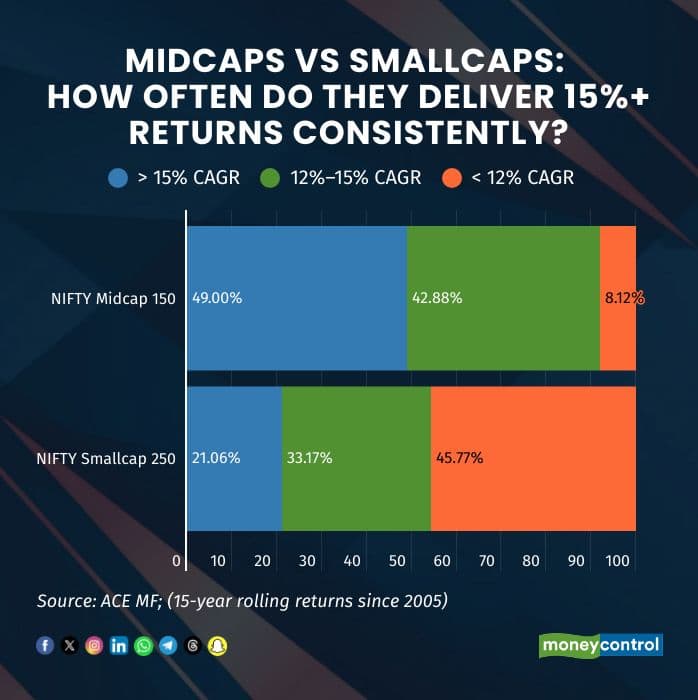

Taking more risk doesn’t magically fix the problem

With this rule, investors think they’ve found the solution: “If large-cap or diversified funds won’t give me 15 percent, I’ll move to mid-cap or small-cap funds. Higher risk, higher returns.”

It sounds logical. It just isn’t consistently true.

Over the past 20 years:

While mid-cap funds did slightly better but consistency was missing.

Yes, these segments can outperform in certain cycles but they also experience longer drawdowns, sharper falls and extended periods of underperformance. Many investors enter chasing past returns and exit at the wrong time.

What this means for investors: You can’t force a 15 percent outcome by taking more risk. In fact, chasing high returns often increases the chance of behavioural mistakes — panic selling, switching funds too often or abandoning SIPs altogether.

Inflation shrinks the final number

Let’s assume the best-case scenario for a moment.

You invest for 15 years. You stay disciplined. You actually manage to hit Rs 1 crore.

Now comes the uncomfortable question: what will that Rs 1 crore be worth?

At an average 6 percent inflation rate, the purchasing power of money drops significantly over time. Rs 1 crore after 15 years would be worth only about Rs 42 lakh in today’s terms.

That is the real value of your corpus.

And this is before considering taxes, lifestyle upgrades, changing responsibilities and longer life expectancy.

The number still looks impressive but its ability to support your future life is far more limited than it appears.

What this means for investors: If your goals aren’t inflation-adjusted, you may hit your target and still fall short of what you actually need.

Should you ignore the 15×15×15 rule?

No, but you shouldn’t follow it blindly, too. The 15×15×15 rule works well as a starting point. It introduces the habit of investing, the power of compounding and the importance of time in the market. Where it fails is as a complete financial plan.

A better way to plan is to keep return expectations realistic, factor in inflation from day one, increase SIPs as your salary grows and invest according to your own risk comfort, not a one-size-fits-all rule.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.