Dev Ashish

Moneycontrol Contributor

Buying a house is a major financial decision that may have crossed mind over 100 times. There is no doubt that there is something psychologically important about buying your first house. It could be instincts or something else, but it is nonetheless a significant monetary commitment.

It is important to identify whether you are ready to purchase your first home and this depends primarily on two factors:

Do you have the down payment available?

This is quite simple. Lenders want 20 percent of the cost of the house as down payment. So let's say if you wish to purchase a house for Rs 50 lakh, you need to possess Rs 10 lakh as down payment. The remaining can be sought as loan.

Depending on the cost of the house, if you don't have the 20 percent as down payment, it mean you aren't ready to buy a house as yet.

Can you afford the EMIs?

Even if you somehow manage the down payment, the next question arises, whether you'll be able to handle the EMIs on time.

Remember, your willingness to pay and your ability to pay are two different things.

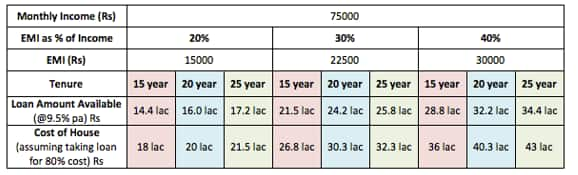

It is said that loan EMIs shouldn't be more than 30-40 percent of your month income. Anything beyond that would stretch your finances. And remember, your EMI does not only depend on the loan amount, but on the tenure as well.

Suppose your monthly income is Rs 75,000.

Let’s see what is the cost of the house that you should purchase for various combinations of EMI-as-%-of-Income & Loan Tenure (assuming home loan rate at 9.5%):

Though lenders mostly decide this, the fact is that going for a loan where EMI is 20 percent of net monthly income means being on the safe ground. Unless your income is extremely high, chances are that you might be settling for a smaller property that doesn't cost too much or maybe you are putting up a bigger down payment.

On the other hand, if the EMI is 40 percent or more of your income, then it can be a tight situation in the initial years. Around 30 percent is more of a good middle ground that can suit most people.

One important thing to highlight is that many couples take loans together to service larger EMIs. This works well, but you don't want to be in a situation where after a few years, only one person is working (ie family transitions from a double income household to single earner family) and having to pay the entire EMI, which was initially taken assuming two incomes.

But as mentioned earlier, down payment and EMI affordability are not the only things that matter when it comes to knowing whether you are ready to buy your first house or not.

Having a buffer for emergencies (+EMIs) is necessary

In life, there will be emergencies every now and then. These are unavoidable. But you can make some arrangements to tackle them.

Now, if you have already pushed yourself into a corner by using all your savings for down payment and are finding it difficult to service the large EMI (in comparison to your current income), then imagine how you will deal with unexpected emergencies (like medical emergency, temporary loss of job, major repairs, etc). Will you be in a position to arrange funds in time?

This is one reason that you should not exhaust all your savings to pay the down payment. Always keep some money for emergencies.

Ideally, having six months of regular expenses as savings is the way to go. A better situation would be to have additional three months EMI as reserve. This will come in handy in case you are temporarily unable to pay EMIs for a few months.

Save for other important goals well

Just because you can arrange the down payment, service EMIs and have some buffer for emergencies doesn't mean that your work is done.

Buying a house is important no doubt, but if some critical goals like child's higher education needs to be tackled in a few years time, you cannot ignore saving for it. You will necessarily have to reconsider how much EMI you should be handling if you need to save for such critical goals. It's a no-brainer trade-off for most parents.

Do understand that the idea of this article is not to make the decision-making complicated for first time homebuyers.

Many people, in their excitement at the prospect of owning their first piece of real estate, forget the factors (like availability of down payment, EMI serviceability in the long term, contingency buffers, saving for other short-term goals) that should be considered before making the final 'buy' decision.

So if you are in the same boat, do consider all the issues discussed above and assess yourself on each of them objectively, before you determine whether you are actually ready to buy your first home or not.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.