There was good news for the first time home-buyers looking for an affordable house costing up to Rs 45 lakh. Finance Minister Nirmala Sitharaman extended the tax benefits under Section 80EEA of the Income Tax Act, 1961, by one more year till March 2022.

Be that as it may, in the current low interest rate scenario and the rule governing the amount of loan sanctioned for a house, will a property buyer be able to take full advantage of this extension? The answer is a no. Here’s why.

The criteria and deduction

Under Section 80EEA, a homebuyer purchasing a residential property of up to Rs 45 lakh is entitled to get additional tax benefit of Rs 1.5 lakh on payment of interest on the home loan. This will be in addition to the Rs 2 lakh available under Section 24 (b). So, the total tax exemption on payment of interest on home loan goes up to Rs 3.5 lakh.

Who gets full deduction?

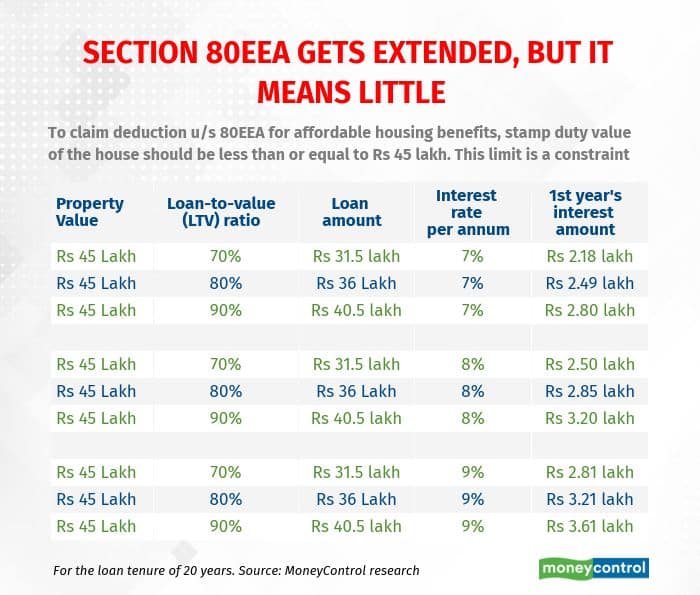

The limit on just the interest paid appears generous. But simple calculations show that the generous limit does little to help a vast majority of home buyers who might want to take full tax deduction benefits. There are two reasons for this: the prevailing home loan interest rates and the loan-to-value (LTV) ratio.

To avail the tax benefit to the fullest, a homebuyer needs to take 90 percent loan on a residential property valued at Rs 45 lakh, for 20 years, at an interest rate of 9 percent, to exhaust the limit of Rs 3.5 lakh deduction. Since the prevailing interest rates for affordable housing are around 7 percent or less, about 200 basis points lower than 9 percent, the home buyer cannot exhaust the permissible limit of tax concession.

Aarti Khanna, co-founder and CEO, AskCred.com, says, “At an interest rate of anywhere less than 8 percent per annum, it doesn't give much monetary benefit to the home buyer as one would not be able to fully exhaust the benefit. At an interest rate of 8 percent per annum or more, it still does.”

The other complication lies in the loan-to-value (LTV) ratio. Khanna says that with banks anyways giving approximately 70 percent LTV of the property value, the benefit is “quite frankly, an eye wash; one would not be able to utilise the benefit to its fullest.” She says that the finance minister should reconsider and increase the property limit of Rs 45 lakh to at least Rs 60 lakh.

On the other hand it can also be argued that home buyers at least get some additional deduction over and above Rs 2 lakh if not the full benefit, she says.

Other experts echoed the thought. V Swaminathan, CEO Andromeda & Apnapaisa, says, “The Rs 3.5 lakh deduction available for affordable housing made sense when the interest rates on such loans were 8-9 percent.”

"It helps to bear in mind that the actual loan amount is likely to be lower than Rs 45 lakh, if the registered value of the house is capped at Rs 45 lakh to avail this benefit. Also, the interest amount is likely to decrease over time, given the principal repayments are part of EMIs. To correct this, the government should revise the registered value to Rs 60 lakh so that buyers can avail the full benefit of these provisions," says Swaminathan.

Under-construction property might be the way out

However, tax experts indicate that in certain conditions a borrower can be able to take full benefit of 80EEA. "It may also be noted that for claiming deduction u/s 24(b), completion of property and possession thereof is mandatory. However, there is no such condition for claiming deduction of interest u/s 80EEA,” says Shailesh Kumar, Partner, Nangia & Co LLP.

“Thus, there may also be situations, where the homebuyer has got the loan sanctioned and partially disbursed for purchase of an under-construction property and is paying interest on such a home loan. The homebuyer may be eligible for deduction u/s 80EEA on such interest, though deduction cannot be claimed u/s 24(b) in that year due to property possession not yet handed over," added Kumar.

Moneycontrol’s take

The push for affordable housing is well-intentioned. It nudges more and more Indians to have a roof over their heads. And carving out a separate section in the Income Tax Act, just for affordable housing, works well. In that sense, Budget 2021’s decision of extending the loan facilities till March 2022 is welcome.

But if ground realities do not allow the home buyer to take the full benefits, it is a waste of income-tax deductions. In view of the pressing need to boost economic growth, raising the limit for affordable housing at this juncture will help everyone.

One way in which this gap can be addressed is to make the required change in the Finance Bill 2021 while replying to the debate on the Bill in parliament.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.