Neha Dave

Moneycontrol Research-

-Private non-life players continue to gain market share

-State-owned insurance companies report muted growth in premiums

-The sector is in a sweet spot supported by progressive regulations-ICICI Lombard better positioned in a growing sector

-------------------------------------------

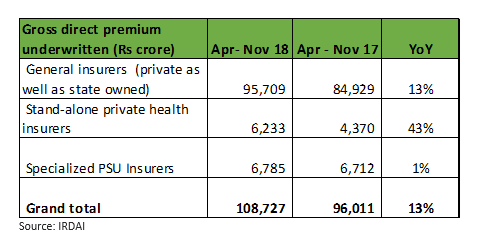

For the period April-November 2018, the total gross direct premiums underwritten by non-life insurers (general insurers, stand-alone private health insurers and specialized PSU insurers) in the country grew by a healthy 13 percent year-on-year (YoY) to Rs 1.08 lakh crore as per data released by IRDAI on December 26.

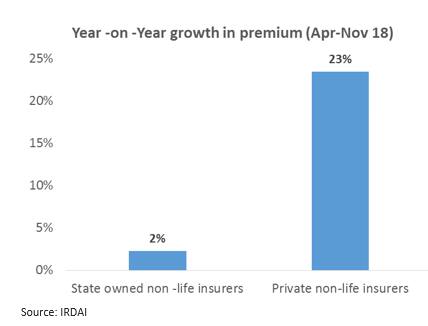

Market share continues to edge up for private insurers

The overall growth in premium was led by private general insurance companies which reported a growth of 23 percent YoY. State-owned general insurance companies witnessed muted growth of around 2 percent in the gross premium underwritten for the same period. Consequently, private players continue to gain market share which now stands at around 48 percent as compared to 40 percent for state-owned insurers.

Immense sectoral opportunities

The size of the Indian general insurance industry is Rs 1.5 lakh crore on a GDPI (Gross direct premium income) basis as at end FY18. It has grown at a compounded annual growth rate (CAGR) of 17 percent in GDPI in last 17 years. There are 33 general insurance companies offering multiple products like motor, health, crop, fire and marine.

There are several growth levers that will drive the high-teen growth for the general insurance industry over the next few years. India continues to be a grossly underpenetrated market with a non-life penetration at one-third of the global average in 2017. The insurance density (non-life insurance premium per capita) also remains significantly lower than other developed and emerging market economies.

We see multiple opportunities for the underlying sub-segments. A higher cost of healthcare and rising incidences of critical illness will likely increase health insurance penetration. Increase in new vehicle sales will be a key growth driver for the motor insurance segment. The significant growth in the segment like crop insurance was driven by government initiatives like Pradhan Mantri Fasal Bima Yojana.

As of now, motor insurance forms the largest product segment, contributing more than 30 percent of GDPI for the sector. Motor along with health contributes nearly three-fourth of the gross premium written in India.

Progressive regulations support growth

Regulations too continue to be progressive and supportive of the growth in the sector. For instance, following Supreme Court’s order, IRDAI made third party (TP) insurance cover for new cars and two-wheelers mandatory for a period of three years and five years respectively from 1st September as against one year earlier. This was a positive development as it well addresses the problem of non-renewal of motor insurance in case of older vehicles. Since long-term policies reduce the uncertainty related to renewal premium, we can expect strong growth in TP motor insurance premiums and to benefit well-entrenched players like ICICI Lombard.

Also Read: SC third party motor insurance ruling: Here’s how it impacts general insurance companies.

Another example of supportive reform is the passage of The Motor Vehicles (Amendment) Bill, legislation approved by the Lok Sabha and currently awaiting approval in Rajya Sabha. It is expected to improve the profitability of the insurers in the motor segment in the long term.

ICICI Lombard well placed in the growing sector

ICICI Lombard General Insurance, India’s largest private sector non-life insurer with a market share of around 9 percent, remains our preferred pick in the sector.

ICICI Lombard is well poised for earnings growth with an increase in insurance penetration, focus on profitable segments and improvement in operating efficiency. The stock has outperformed Nifty year to date by around 3 percent and is trading at 7.5 times its trailing book. The current valuation is rich even after considering the high return on average equity at more than 21 percent.

We have seen that leading companies in the secular growth sector tends to trade at higher multiples for a long period in time. In the absence of suitable and comparable listed peer, ICICI Lombard trades as a proxy for the sector commanding a higher valuation. While the premium valuation will sustain, near-term upside in stock price is limited. Nevertheless, for investors with a long-term horizon and wanting to participate in the growth in the non-life insurance sector, the stock is worth considering.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.