Nitin Agrawal

Moneycontrol Research

With all regulatory headwinds behind the automobile industry, Maruti Suzuki India (MSIL), the country’s top car maker with a market share of close to 57 percent in the passenger vehicle segment, continues to post a steady result. The company posted strong topline and realisation in Q4 FY18. However, operating margin witnessed a contraction due to rising staff and other costs.

Today, MSIL has a virtual monopoly in the Indian passenger vehicle market driven by strong dealership network, brand loyalty on the back of competitive prices and resale value. With a slew of new launches including refreshers, strong order pipeline, product rejig toward premium products and leadership position in Indian market, the stock will continue to enjoy investor attention despite its premium valuation.

Quarter in a nutshell

Strong volume and average selling price growth

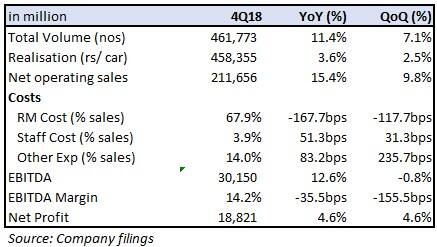

MSIL continued to post double-digit volume growth of 11.4 percent on a year-on-year (YoY) basis, led by new launches and healthy demand from rural areas which grew 15 percent and forms 36 percent of total sales. Utility vehicles (UVs) witnessed a significant 29.6 percent growth YoY, followed by compact segment which grew 12.7 percent YoY. UVs now contribute close to 14 percent of total domestic sales.

Net operating revenues registered a strong 15.4 percent YoY growth on the back of a rise in volumes and average realisation (up 3.6 percent YoY). The management attributed the increase in net realisation to expanding premium products in the portfolio, which it sells through its Nexa outlets.

Stable EBITDA margin; staff cost and other expenses exert pressure

The company posted a 35.5 bps YoY and 155.5 bps quarter-on-quarter (QoQ) contraction in earnings before interest depreciation and tax (EBITDA) margin on account of an increase in staff cost and other expenses. Staff cost witnessed a spike due to change in the Gratuity Act and other provisions related to variable cost. Increase in freight cost and royalty payments due to an unfavourable exchange rate led to rise in other expenses. Additionally, the management expects raw material cost to continue to rise.

Should one own Maruti stock for the long-haul?

Premiumisation trend continues

The management has been able to identify customer preference patterns and tailor its products accordingly. It has successfully reoriented its product portfolio, which was earlier dominated by small cars, to premium products that cater to the changing customer preference. The new Swift and Swift Dzire have received very strong traction from customers.

Strong distribution network a moat

MSIL’s strength lies in its strong distribution network. This gives it an edge in an otherwise competitive market. In a strong quest to cater to the premium segment, the management is expanding its Nexa network. It currently has around 250-300 Nexa outlets and plans to expand it to 400 by 2020. On the back of a strong product portfolio and distribution network, the company has been able to grow its market share despite the entry of multiple global players.

Strong product pipeline

The company has planned a slew of launches over the next three years. The management has a track record of more success than failures over the last four years. Except for S-Cross, all other launches from FY12 till FY18 witnessed strong customer demand.

Getting ready for EV

The company is gearing up for the next big disruption in the automobile industry: electric vehicles (EVs). Recently, it announced an investment of Rs 1,200 crore for setting up a Li-ion manufacturing unit in India. As per the management, the indigenous development of the battery could substantially bring down prices of EVs.

Capacity expansion

MSIL has a huge order backlog, indicating strong demand from customers and need for capacity expansion. The management has clearly chalked out its capacity expansion plan. Production from Phase I of the Gujarat plant has begun. The plant is expected to produce 250,000 units this year. Phase II would start from January next year. The management expects to expand capacity of this plant to 1.5 million units.

Change in royalty

In FY18, royalty payment stood at 5.4 percent of net sales compared to 5.8 percent last year. For Q4 FY18, royalty was higher at 5.7 percent due to an unfavourable exchange rate. The management said royalty payments are expected to be revised downward for all new models and refreshers starting with the Ignis. It has received approval from the Suzuki board for the same. As per the agreement, it would now pay royalty in rupee terms rather than in yen and after a certain volume is achieved, the royalty rate would reduce.

Valuations at elevated levels

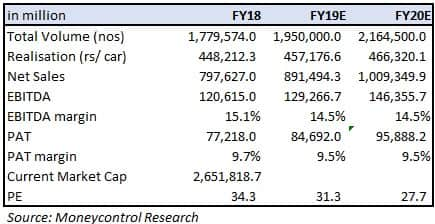

The counter currently trades at 31.3 times FY19 and 27.7 times FY20 projected earnings. Despite our high comfort on the business, the valuation leaves little room for comfort. We would advise investors to accumulate the stock on any weakness.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.