Sachin Pal

Moneycontrol Research

started FY19 on a strong note, reporting strong volume growth and operational performance in Q1. The company has a strong positioning in central India and is benefitting from positive market demand. The recent market correction provides an opportunity to accumulate the stock at current levels.

Strong quarterly performance

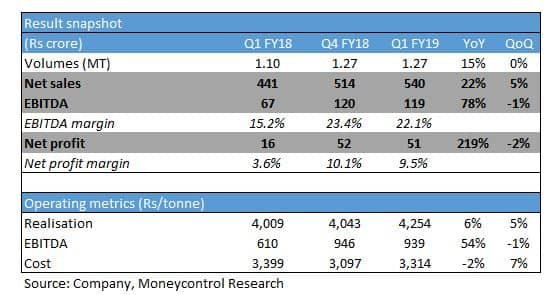

For Q1 FY19, the company reported sales and earnings before interest, tax, depreciation and amortisation (EBITDA) growth of 22 percent and 78 percent year-on-year, respectively. This was aided by volume growth of 15 percent owing to strong demand in the central region.

Operating leverage from higher capacity utilisation along with cost benefits from its Waste Heat Recovery System plant and conveyor belt offset increased cost pressures and resulted in the sharp jump in operating profit to Rs 119 crore in Q1 FY19. EBITDA realisation remained flat on a quarter-on-quarter (QoQ) basis.

High volume offtake to continue

The capacity utilisation during Q1 was more than 90 percent. The monsoon has had little impact on demand in the seasonally weak Q2. Volumes for July-September quarter are expected to remain strong as the management has indicated a capacity utilisation of 80 percent for clinker and 90 percent for cement. Overall volume growth for FY19 is pegged to be in the 8-10 percent range.

Central region leads on demand and pricing front

Cement prices across India have been supported by higher exit prices at the end of June. Prices in most regions trended higher in July, but corrected moderately (2-3 percent) over August and September. The northern region saw another quarter of stable prices, but cement realisations continue to be weaker than other regions.

Price uptrend in the central India is being supported by 80 percent capacity utilisation in that region. Growing demand as well as limited capacity addition in the central region will continue to drive prices higher.

Input cost pressures to persist

During Q1, majority of companies in the sector reported minor improvement in operating margin as input costs appear to be stabilising. But the recent fall in the rupee will make pet coke imports costlier. This, along with the hike in diesel prices, will amplify existing cost pressures. The impact on Heidelberg is expected to be limited as the company has a strong focus on the cost structure and has been able to maintain margin in a challenging operating environment.

Outlook and recommendationWith a pick-up in infrastructure development, demand is expected to remain firm overall. Government spending on infrastructure along with affordable housing schemes should lead to cement growth of 7-8 percent in the current fiscal.

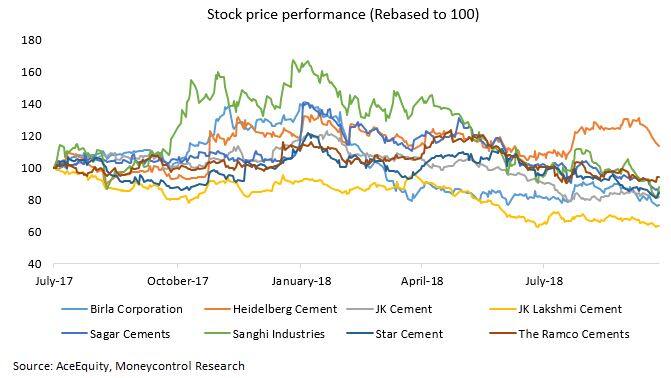

We continue to prefer Heidelberg Cement from the midcap cement pack as the company has strong positioning in the central market and a superior margin profile compared to peers. Driven by improving fundamentals, the company continues to outperform its sectoral peers. In fact, it is the only company among the listed midcap cement peers to have delivered positive returns since July last year.

Firm cement prices in the central region along with strong operating leverage is expected to aid earnings over the next 12-15 months. The stock witnessed a strong rally after the Q1 result but has shed most of its gains in the broader market correction. The current valuation (FY19 enterprise value/EBITDA multiple of 9 times) appears reasonable for a fresh entry. Long term investors looking to add equity exposure in the midcap cement space can look forward to accumulate this stock on declines.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!