Sachin Pal

Moneycontrol Research

Asian Paints reported a mixed set of earnings in Q2 FY19. Revenue came in-line with our expectation as the company delivered strong double-digit volume growth. However, profit declined as crude-related margin pressures became visible in the quarter gone by.

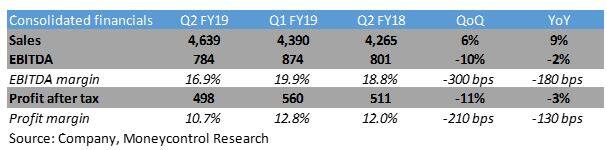

Consolidated net sales increased 9 percent year-on-year (YoY) to Rs 4,639 crore in Q2 FY19. Operating profit declined 2 percent to Rs 784 crore as margin reduced on account of inflationary cost pressures. Profit after tax declined 3 percent to Rs 498 crore.

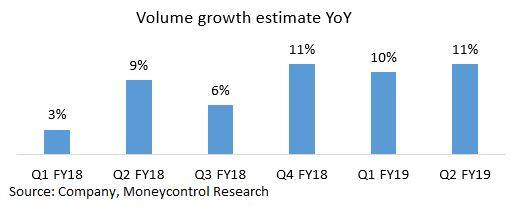

Low double-digit volume growth

Volume growth is estimated at 11 percent in the quarter gone by. A favourable base, along with higher demand from the emulsion segment, drove higher volumes. Demand was also impacted by a number of factors including a delayed festive season and a Goods and Service Tax (GST) rate reduction. Overall, the company delivered its third successive quarter of double-digit volume growth.

Sales growth was, however, lower than volume growth due to a change in product mix, permanent shutdown of Phthalic Anhydride plant (in Q2 FY18) and price revisions.

The management has a cautious outlook as the weak monsoon has resulted in subdued rural demand. The demand uncertainty has also increased in the market in light of the upcoming elections.

Domestic operations on track

While the domestic decorative business continues to do well, the industrial paints business witnessed strong growth in both the protective and powder coatings segment.

The home improvement business (Sleek and Ess Ess) is in expansion mode and saw a strong jump in revenues (on a small base) to Rs 104 crore from Rs 84 crore YoY.

International operations facing some challenges

While domestic business seems on track, the international business (which constitutes around 10- 12 percent of total revenue) is facing challenging times.

Operations in Africa (Ethiopia and Egypt) and Middle East are facing some challenges on account of adverse currency fluctuations and increased competitive intensity.

In Asia, Indonesia is witnessing strong traction, but Sri Lanka was negatively impacted by rains in the quarter gone by.

Delay in price hikes to put pressure on margins

The company witnessed some margin pressure in the past few quarters as key inputs linked to crude continued to move northwards. A large portion of these raw materials (30-35 percent) are imported. Currency depreciation has further intensified cost pressures and this was evident in Q2 FY19.

The company has been offsetting input costs pressures with consistent price hikes. After the 1.5 percent hike initiated in March, it had announced another price hike of 1.9 percent effective May. The management was contemplating another price hike in August to mitigate rising cost pressures, but delayed the same on account of reduction in GST (revised from 28 percent to 18 percent for paint companies).

Asian Paints witnessed logistical challenges toward the end of July as it had to re-label all dealer inventories with the new GST rate.

The latest price hike of 2 percent (effective October) is expected to alleviate cost pressures being faced by the company. However, the quantum is unlikely to offset the rise in input costs. Another rate revision in the near term seems unlikely as the company has already initiated three price hikes in the last six months and further hikes could have a negative impact on demand.

Outlook and recommendationAlthough the company has reported a pick-up in volume growth in the past three quarters, the management remains cautious as demand is yet to witness a broad-based recovery and competitive intensity continues to remain elevated. In the short term, inflationary cost pressures will continue to weigh on margins as oil prices have witnessed a sharp rise in the past one year. Over the medium to long run, we expect margin to return to earlier levels as Asian Paints commands dominant market share in the industry and therefore enjoys strong pricing power.

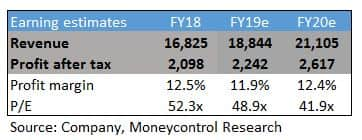

Asian Paints commands premium valuations on account of its market leadership position. Over the past three months, the stock has moved in-line with the broader market index and is now valued at 42 times FY20 estimated earnings. We see value beginning to emerge in this stock after the sharp correction post its Q2 results. Long term investors with low-to-mid teens return expectations can slowly build positions in the stock on any further correction from current levels.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!