Nitin Agrawal

Moneycontrol Research

Robust financials, reasonable valuations, and a strong presence in a niche area make Goodyear India a good long-term investment.

The business

Goodyear India (GDYR) is a leading manufacturer of automotive bias tyres viz. farm tyres and commercial truck tyres. It also trades in “Goodyear” branded tyres manufactured by Goodyear South Asia Tyres Private Limited (GSATPL), Aurangabad. The other products which the company markets and sells include tubes and flaps.

We like the following about the company:

Niche player – Farm Equipment Tyre

Goodyear is a niche player in Indian tractor tyre industry with a market share of over 30 percent. The company directly supplies to companies such as M&M, Escorts Agro Machinery and John Deere.

Strong industry tailwinds

The company generates most of its revenues from farm tyres. The segment is doing well as tractor sales have been on the rise because of normal monsoon last year. In volume terms, tractor sales are up 16 percent so far this financial year, compared to the same period the previous year.

We expect the momentum in tractor sales to continue because of:

1. The strategic importance of rural economics to India's economy. We see a very high likelihood of government’s focus on agriculture and its target of doubling the farmers’ income by FY22

2. Normal monsoon leading to improved rural sentiment

3. Improvement in farm machination

All these factors will boost demand for farm equipment, benefiting Goodyear.

Focus on CV and PV tyre segment

Apart from tractor tyres, the company has also been focusing on the commercial vehicle and passenger vehicle segments. Both these segments are in a strong uptrend currently.

The commercial vehicle segment had a bumpy ride in FY17 as first demonetisation and then GST-led de-stocking impacted sales. Restocking has now resumed as evident from the sales numbers for last two months.

There are multiple triggers for the growth in the passenger vehicle segment as well. Rising per capital income, low penetration, and the government’s focus on increasing rural income are expected to drive demand for passenger vehicles.

Within passenger vehicles, the company is focusing on luxury and SUV sub segments as the management sees demand for premium vehicles growing. The company has partnered with premium car makers to supply tyres.

Currently, the company is also working on expanding distribution, strengthening its presence in branded retail stores and building its brand in the digital space.

Ownership – lends comfort

Goodyear India is a wholly-owned subsidiary of Goodyear Tire and Rubber Company (USA), which has 74 percent stake in the company. Institutional investors with sizeable stakes in the company include SBI Magnum Balance Fund & SBI Emerging Businesses Fund which holds 4.51 percent stake and Goldman Sachs which has 2.36 percent stake.

Immune to electric vehicle disruption

The imminent disruption from electric vehicles will not affect tyre makers in general as tyres are critical for the mobility of any type of vehicle.

Strong financial performance

Goodyear is a cash rich (~19 percent of the current market cap), debt-free company and has reported good financial numbers over past few years.

Despite flat top line over CY13-FY17, the company posted a strong growth of 11.2 percent and 10.6 percent in its EBITDA (earnings before interest, tax, depreciation and amortisation) and profit after tax over the same period, respectively. Over the same period, EBITDA margin also expanded by 438 bps and was at 14.3 percent in FY17.

The management is focussed on maintaining margins even if that comes at the cost of sales volumes. Hence, the company’s top line growth was muted and its profitability grew significantly and margins expanded even in times when raw material prices were not favourable.

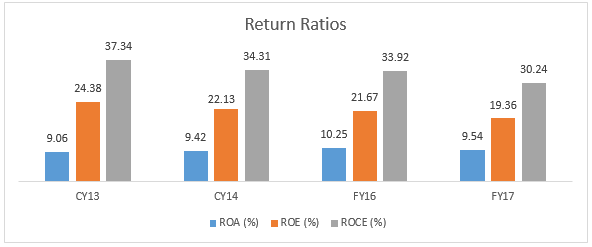

In terms of return ratios, average Return on Equity and Return on Capital Employed stood at 21.9 percent and 34 percent, respectively, over CY13-FY17.

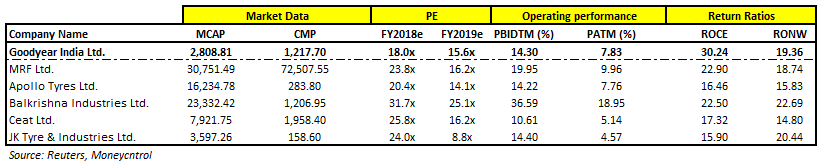

In terms of valuation, the company is trading at 18.0 and 15.6 times FY18 and FY19 projected earnings, which make it a reasonably valued stock in tyre space with very strong fundamentals and growth outlook.

Risk and concernsThe biggest risk for the company is a spike in raw material prices (natural rubber), as they account for a big chunk of the costs. However, the track record of the company suggests it has historically been able to manage the rise in the raw material prices to its customers. The lowest EBITDA margin that the company posted was 6.7 percent in last 10 years. Hence, raw material prices does not pose a very big concern for Goodyear.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!