Although the market has seen rangebound trade in the current festive season, it has been hitting fresh highs day-after-day. The 30-share BSE Sensex crossed another milestone of 34,000 in previous session and maintained that level in Wednesday's trade.

The 50-share NSE Nifty also traded above 10,500 level, rising more than 28 percent, so far, in current calendar year. The rally was largely driven by liquidity on hopes of recovery in corporate earnings & economic growth, and government reforms.

The broader markets also participated in the rally, outperforming frontline indices. The Nifty Midcap shot up more than 45 percent year-to-date.

The market buoyancy is likely to continue in 2018 as well, though it could be volatile due to events like states elections, Union Budget. The Nifty50 is expected to give 10-15 percent return and the midcaps are likely to continue their outperformance in the coming year, experts suggest.

"We expect Indian markets to remain highly volatile in CY2018 led by domestic and global factors. While we do not expect a similar run on Nifty as in CY2017, we do expect it to generate around 15 percent in CY2018," Ajay Jaiswal, President – Strategies & Head of Research at Stewart & Mackertich Wealth Management said.

He expects Nifty to trade around 16.50 times FY20(E) EPS of around 734 towards the end of December 2018, which leads to a level of around 12,111.

However, select stocks and sectors would continue to outperform benchmark returns by a wide margin, he feels.

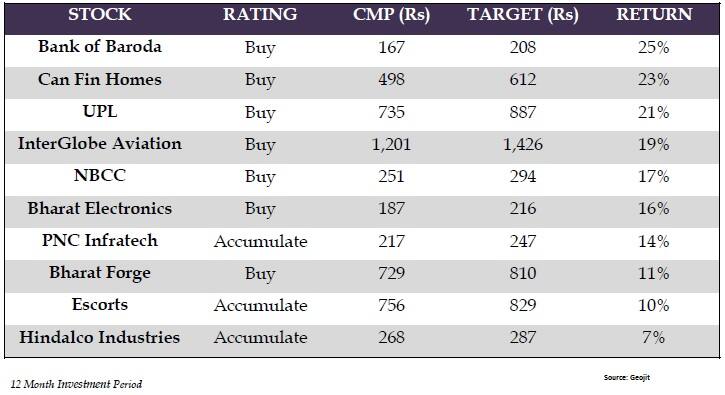

Geojit Financial Services has come out with a list of top 10 stocks that rallied up to 155 percent in 2017, but can still give up to 25% return in 2018:

Bank of Baroda is one of India's largest banks with strong domestic presence spanning across 5,422 branches. The bank also has significant international presence with a network of 106 branches across 25 countries.

Given the management's focus on cleaning up the balance sheet and laying the foundation for sustainable growth, the gradual improvement in asset quality will lead to better profitability.

As a result, we expect return on assets and return on equity to improve to 0.5 percent and 9 percent, respectively by FY19.

We maintain Buy rating on the stock with a target price of Rs 208.

Can Fin HomesCan Fin Homes is a south based housing finance company sponsored by Canara Bank with focus on Tier 1 and 2 cities.

Given the strong traction in loan book expansion and sustained healthy asset quality (gross/net NPA at 0.2 percent / 0.0 percent as of FY17) and its premium valuations within the housing finance companies space is justified.

We project Can Fin Homes to deliver around 2 percent return on asset over FY17-19. We recommend Buy rating with a target price of Rs 612 per share.

UPL is a leading manufacturer of crop protection products and ranks among the top five generic agro-chemical companies globally. It offers a range of crop protection products, such as herbicides, insecticides and fungicides.

We expect EBITDA / PAT to grow at a strong CAGR of 17.4 / 13.7 percent over FY17-19 led by better product mix, backward integration, new product launches and rising market share in high-growth countries like Brazil and India. We value UPL at P/E of 17x on FY19 with a target price of Rs 887 and we have Buy rating for the stock.

InterGlobe AviationInterGlobe Aviation (IndiGo) is one of the most efficient low cost carriers with a market share of 40 percent in Indian aviation sector.

We are positive on IndiGo given increasing air travel penetration, market leadership position, and strong balance sheet. We value at P/E of 20x on FY19 with a target price of Rs 1,426 and recommend a Buy rating.

NBCCNBCC is a Navaratna enterprise under Ministry of Urban Development. Its business verticals include - project management consultancy, engineering, procurement & construction, and real estate business.

NBCC is at sweet spot considering its huge order book, limited competition and expertise in executing large projects. More potential opportunities are in pipeline from Dharvi, Railway station redevelopment and irrigation project in Maharashtra.

Given strong execution capability, we expect FY18 EBITDA margin to improve by 34 bps to 6.8 percent and FY19 margin to 6.9 percent.

Given strong earnings outlook, we value NBCC's core business at a P/E of 30x on FY20 and Rs 25 per share for land parcel held to arrive at SOTP target price of Rs 294 and maintain Buy.

Bharat ElectronicsBharat Electronics is a Navaratna enterprise having 37 percent market share in Indian defence electronics. Its core capabilities are in radar and weapons systems, defence communication and electronic warfare.

In recent times, BEL's valuation has significantly re-rated due to strong order inflow and improvement in earnings profile. Given its robust order book and healthy order pipeline we continue maintain a strong Buy rating for the stock. We value BEL at P/E of 22x on FY20 with a target price of Rs 216 per share.

PNC InfratechPNC Infratech is an infrastructure construction, development and management company; expertise in execution of projects including highways, bridges, flyovers, airport runways, industrial areas and transmission lines.

Given strong order book (Rs 11,148 crore) and lean balance sheet, we maintain our positive view and value standalone business at a P/E of 18x FY20 EPS, and BOT/HAM projects at 1.2x P/B with a change in rating from Hold to Accumulate.

The overall visibility has improved and we expect progress in awarding new road projects by MoRTH, NHAI will drive order book by 19 percent CAGR over FY17-19.

Bharat ForgeBharat Forge is a leading player in the forgings industry. The company is serving, several sectors including automobile, power, oil & gas, rail & marine, aerospace, construction, mining etc.

We expect Bharat Forge to register 17 percent revenue CAGR over FY17-19 on account of healthy demand from US commercial vehicle, revival of oil & gas sector and new order from domestic auto and non-auto space.

De-risking the utilisation in non-auto segment and ramp up of passenger vehicle sales will support growth. We expect Bharat Forge to trade at a premium valuation given its strong earnings outlook.

We expect the earning to grow by 40 percent CAGR over FY17-19 factoring higher export mix. We maintain our rating as Buy with a revised target price of Rs 810 per share.

EscortsEscorts is the third largest agricultural tractor manufacturer in India. It has a strong presence in the north and west market, with an overall market share of 11 percent as on FY17.

We believe that the current valuation is justifiable on the back of robust earnings outlook and initial favourable monsoon. We value Escorts at 22x on FY20 EPS with a revised target price of Rs 829 and maintain our rating as accumulate.

Hindalco IndustriesHindalco Industries, an Aditya Birla Group Company, is an industry leader in aluminium and copper. The acquisition of Novelis in 2007 placed the company among the world's leading manufacturers of aluminium.

We maintain our positive stance on the stock on the backdrop of company's continued focus on deleveraging its balance sheet and improvement in free cash flow generation.

Additionally, improving earnings visibility at Novelis with higher proportion of high margin auto sheet business and sustenance of competitiveness in the domestic market led by its low cost of production and higher coal linkages will drive growth going forward.

We value Hindalco based on SOTP, valuing both standalone and Novelis business at 6x EV/EBITDA. Recommend Accumulate with a target price of Rs 287.

Disclaimer: The views and investment tips expressed by brokerage houses on moneycontrol.com are his own, and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.