Infosys fourth quarter numbers and guidance were unimpressive, but the payout policy could cushion near term downside in the stock price.

Infosys’ constant currency revenue guidance of 8.4-8.8 percent while announcing third quarter numbers had implied a revenue growth of 0.9-2.2 percent for the fourth quarter.

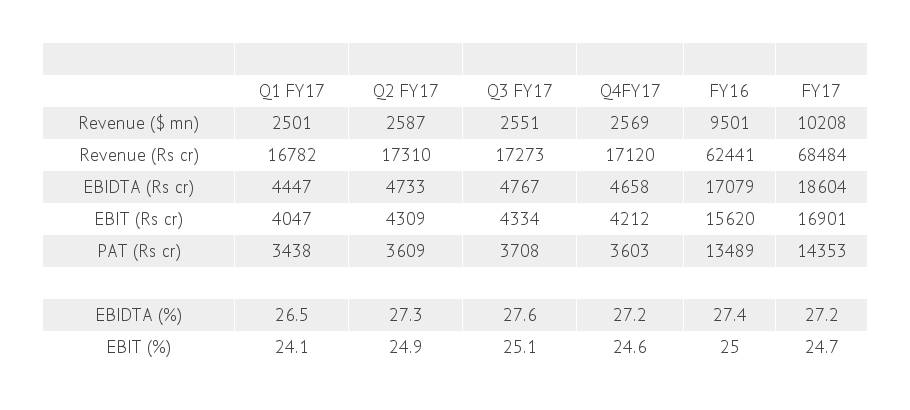

However, revenues declined 0.9 percent in rupee terms and was flat in constant currency. Consequently, it also missed its full year target – FY17 revenue grew by 8.3 percent in constant currency terms, missing even the lower end of its guidance.

Still, the company has been bold enough to guide for FY18, though the 6.5-8.5 percent constant currency growth is a tad lower than street expectations of 7-9 percent. Rupee revenue growth 2.5-4.5 percent is optically lower because of the strength of the currency (1 USD = Rs. 64.85). So only a depreciation in the currency can make the numbers look more respectable.

For FY17, the board approved a final dividend of Rs 14.75 per share, in addition to the interim dividend of Rs 11 per share. The total payout at Rs 7119 crore amounts to 49.6 percent of post-tax profits and 63 percent of free cash flow.

The carrot for FY18From FY18 onwards, the company has decided to pay dividends of up to 50 percent of post-tax profits and up to 70 percent of free cash flow.

While a buyback has not been explicitly announced, out of the total cash of Rs 38,773 crore (USD 6 billion), the company plans to return Rs 13,000 crore (close to USD 2 bn) to shareholders in FY18. While details are awaited, the dividend per share works out to Rs 49 per share (FY17 at Rs 25.75 per share), factoring dividend distribution tax as well. At the current price, this works to dividend yield of 5.2 percent. So is Infosys moving from a growth stock to one which attracts risk averse investors with a preference for high dividend yield?

Infosys ended FY17 with a revenue of USD 10.2 bn. So even if we stretch 2020 vision to end of FY21 – the company has four years to double revenue. This works to CAGR (compounded annual growth rate) of 18 percent. This is a tall ask given that the organic revenue guidance is in single digit. Even after a generous payout, the company will still have a war chest of close to USD 4 bn. But given its conservative approach to acquisitions, we find it hard to believe if any such big bang acquisition is on the cards. That brings us back to the question – will Infosys in the long-term be an acquirer or an acquiree?

The Board has appointed Mr. Ravi Venkatesan, Independent Director as Co- Chairman of the Board. We do not read much into the same. With constant criticism from the founders, it could be a move to strengthen oversight/governance and free up management bandwidth to pursue what it should – growth & M&A.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.