Neha DaveMoneycontrol Research

Central Depository Services (CDSL) is one of only two security depositories in India.

The sector has been growing at brisk pace ever since it was made compulsory in 1999 for all securities trading to take place in the dematerialised (demat) form.

Depositories have actually been a catalyst in increasing active participation of investors in the Indian market. The business is a proxy for the capital market in general and stocks in particular.

CDSL is well-poised to benefit from capital markets continuing to grow in scale and depth. More importantly, we like the depository's inherent strength and the uniqueness of its business model. Add to this its robust financials and the stock is certainly worth considering.

Low risk, predictable business

As a security depository, CDSL facilitates holding and transacting of securities in the electronic form. The depository participants (DPs) act as its agents, offering depository services to the beneficial owner (BO) of the securities.

NSDL, which is the only other domestic player in the sector, continues to lead with a market share of around 57 percent, but CDSL has been consistently gaining market share from NSDL.

CDSL has a well-diversified revenue mix with a higher proportion of annuity revenue, which is not market-linked and is non-cyclical.

Annual issuer charges

This is a stable and regulated (SEBI determined) fixed fee charged to corporate entities annually for holding different securities (equity shares, preference shares, debt instruments, etc.) in the electronic form.

CDSL earned around 29 percent of its operating revenue from annual issuer charges in FY18. The increase in revenue from these fees will be driven by an increase in the number of companies availing demat facilities, and is expected to remain steady.

According to news reports, discussions are on to admit unlisted companies with depositories so that the Ministry of Company Affairs can get a complete view of what is happening in the sectors with respect to shareholding. This can turn out to be another line of business, though it may not be as big as the listed companies' segment.

Transaction charges

These charges are market-linked and charged to DPs based on the number of debit transactions. So the transaction fee depends on the volumes in the secondary market and the increase in number of demat/investor accounts.

CDSL's incremental market share, in terms of number of demat/investor accounts, rose to 63 percent in FY18, which is encouraging. This will drive growth in transaction charges in the future.

IPO and corporate action charges

These are paid by corporates for non-cash corporate actions like bonus issues, subdivision of shares, or creation of new shares in the demat form after an initial public offering.

Revenue from these charges has stupendously grown over the last 3 years because of a thriving capital market in general, and primary markets in particular. While this trend continues, we can expect to see higher growth in this category of charges.

Online data charges

This revenue is mainly derived from CDSL Ventures, which is a 100 percent subsidiary of CDSL. CDSL Ventures provides KYC services to investors in the capital markets, including to those in mutual funds.

CDSL's revenue pool is de-risked by the diverse nature of these charges. We see the stable revenue base from the annual issuer charges segment as one of the key strengths of the business.

The depository has deployed its capital to some other businesses that provide services such as insurance repository and commodities repository. It was recently granted a license by SEBI to become an RTA (registrar and transfer agent).

All these initiatives are in nascent stages and are not making any meaningful contribution to the company's revenue as yet. However, we are encouraged by CDSL's foray into new business segments and expect it to translate to revenue at some point in the future.

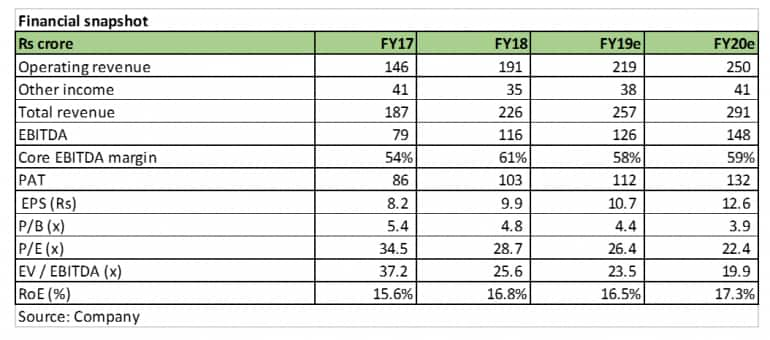

Robust financials

Annual issuer charges are expected ensure stable growth in the company's revenue. The booming capital market, with a large number of primary issuances, high trading volume in the secondary market and huge inflows into mutual funds, will combine to deliver higher revenue growth in the years to come.

CDSL's main operating costs are employee cost and software development and maintenance costs, which are largely fixed in nature. This results in high economies of scale, which is visible in CDSL's high-yet-improving EBITDA margin.

The company's EBITDA margin has expanded to 60 percent in FY18 from 39.4 percent in FY13 as the improvement in revenue growth trickled down to higher profit because of high operating leverage. Moreover, CDSL's debt-free status and minimal capital expenditure requirement enables it to generate strong free cash flows.

Promising outlook

With the only two depositories in the country being promoted by its two major stock exchanges (NSDL by NSE and CDSL by BSE), the depositories sector has a strong entry barrier.

SEBI is considering allowing corporates to enter the depository business based on the recommendations of the panel set up under the guidance of former RBI Deputy Governor R Gandhi.

However, we don't see this move severely impacting the incumbents. With strong parental lineage, these depositories will have a clear advantage over any new entrant, if at all they have to face one.

The growth of depositories is linked to the increase in capital market transactions. We see multiple growth drivers such as increasing financial savings, more retail participation, increase in market capitalisation in sync with economic growth, higher trading volumes and buoyant primary markets, aiding the growth of depositories.

CDSL, being the only listed depository, could be a play on the increase in penetration of financial markets.

Reasonable valuations

The CDSL stock had run up after the company's public issue in June 2017 and is currently trading at 42 percent below its 52-week high. In terms of valuation, the stock is currently trading at 22 times the company's estimated earnings for FY20.

While it is still at a premium to the valuation of BSE, which is a closely-related business, we believe the higher multiple is justified because of its less-cyclical nature vis-a-vis exchanges.

Given the strong return ratios, with RoE at 17 percent (subdued because of cash in the balance sheet), and the inherent strength in its business model, we see a strong upside to the stock's current market price, driven by earnings growth and valuation re-rating. Long-term investors, looking for relatively low-risk financial service businesses with high return potential should buy the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.