Capital market Intermediaries/participants always tell you when to buy, but seldom guide when to sell your longer term equity or debt mutual fund (MF) investments. Let’s looks at how a retail investor, using simple and publicly available historical data, can not only identify the approximate entry/exit time in these investments, but also maximise their returns.

For this, the 10-Year Government Securities (G-Sec) and Nifty 50 index has been used as a proxy to calculate return on debt and equity investments respectively. Investors can track/invest in these two assets either directly or through respective MF schemes.

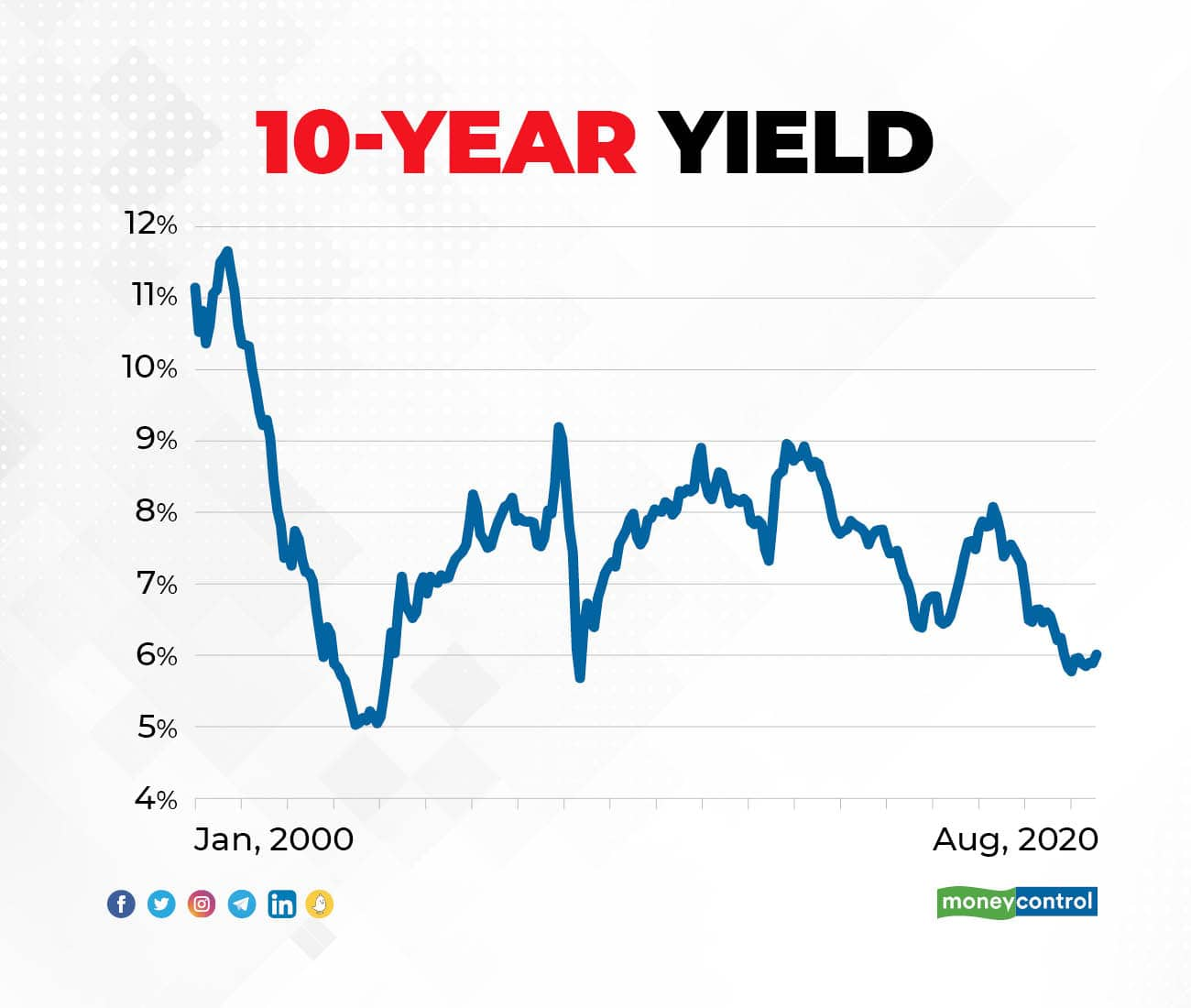

An interesting observation while analysing 10-year G-Secs since 2000 is that they broadly move in the 6-9 percent band. Whenever the yield crosses 8.5-9 percent it starts falling subsequently and as soon it touches/falls below 6.5 percent, it starts to go up.

The price of a debt instrument is inversely proportional to the yield. Which means if the yield is rising the price falls and hence one tends to lose money (the interest received on the debt instrument partially arrests losses). Conversely, when the yields are falling the gains are significant as in addition to the rise in price of the instrument the coupon (interest rate quoted during the issue of the debt instrument) also tends to be higher.

Since, equity and debt are different asset classes, let’s check the returns generated by both during the same time period. In the graph below Nifty returns since 2000 have been superimposed on the G-Sec graph for the same time period.

The above graph shows that there are more months of positive returns reported by Nifty whenever the 10Y G-Sec yield curve is rising (after breaching 6.5 percent levels) and there are more negative monthly returns on Nifty whenever the G-Sec yield is falling (after crossing 8.5 percent levels). This means whenever the equity market does well, returns on debt is lower and vice versa.

The below table provides the numeric validation of the same, along with ideal portfolio decision.

The key takeaway from the above table is that one has to sell equity whenever 10-year yields touch 8.5 percent or more (and correspondingly buy into debt funds) and buy equity whenever 10-year yields fall below 6.5 percent (and correspondingly sell debt funds).

The table below details the kind of returns one would have made if they followed the strategy based on the prevailing 10-year yield.

It is also evident from the above table that even debt investments – just like equity -- have a performance cycle. In other words, there are periods when returns from debt instruments are higher and there are times where returns are lower.

If one looks at the monetised value from the above strategy it would look something like this:

If Rs 100 was invested in January 2000 and investments in debt or equity were not sold throughout the last 20-odd years (three full cycles in each asset class) then the compound annual growth rate (CAGR) would be 8.3 percent and 8.9 percent respectively. However, if investments were switched between the two asset classes (as in the above graph), then the returns would have been more than double at 18.6 percent.

It is important to switch because there have been time periods in the past where these two asset classes have not delivered returns more than inflation.

The above table also demystifies the clichéd statement ‘stay invested for a long term and returns will be maximised’. Hence, to beat inflation as well as maximise returns, using 10 year G-Sec yield as an indicator, one could identify when to switch between equity and debt.

What are the fundamental/economic reasons for this?

When interest rates are at their peak or start declining from their peak, inflation tends to be higher. This means goods and services become expensive and consumption declines. This in turn impacts its demand, resulting in falling sales revenues of companies manufacturing/providing the same. Also, because of higher interest rates, the interest expenses of companies which have loans go up.

These above factors, in turn, negatively impact the companies’ profit/EPS/ RoE and other fundamental metrics. Further, due to higher interest rates, the benchmark return expectations are elevated and with higher discounting rate used for valuing future cash flows, valuations of companies/projects/acquisitions are lower.

This impacts equity valuations and the stocks start getting traded at lower levels, which result in lower returns for investors. At the same time, the debt returns are higher due to higher coupons as well as appreciation in market prices of debt instruments (due to falling yields).

Hence, in such circumstances investors should invest in debt MFs and sell equity MFs to optimise their returns.

When interest rates are at the bottom or start rising from lower levels, inflation is also low. Here, the higher disposable income leads to a rise in demand for products leading to an uptick in revenue growth. With operating leverage kicking in and interest costs also being lower, profits and related growth metrics grows disproportionately. Additionally, with the benchmark return being lower, the discounting rate (used for calculating cash flows) is also lower. This leads to stocks and projects starting to be available at cheap/attractive valuations.

Corporates have cheaper access to loans from financial institutions which are used to fund expansions and acquisitions. On the back of an uptick in the equity markets, more and more corporates are raising equity due to lower discounting rates/attractive valuation compared to their peers. With respect to debt investors, till the time peak interest rates are more than 50-100 basis points away, investors are likely to incur losses on their debt investments and hence continue to prefer any alternative asset classes which would provide better returns/hedge on inflation.

Since, debt returns are lower and business growth outlook is higher, investors keep investing in equity. Hence, in such circumstances investors should invest in equity MF and sell debt MF during this time period and optimise their returns.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.