As India advances toward a $5 trillion economy and aspires to reach $10 trillion by 2037, it faces a silent yet powerful constraint. The nation’s Weighted Average Cost of Capital (WACC) remains among the highest among large economies, averaging around 10.8%, with the cost of equity near 14.2%. This compares unfavourably with developed economies, where WACC levels range between 6–8%.

This persistent premium acts as a structural growth tax, raising the hurdle rate for every investment decision, discouraging risk-taking, and compressing innovation and job creation.

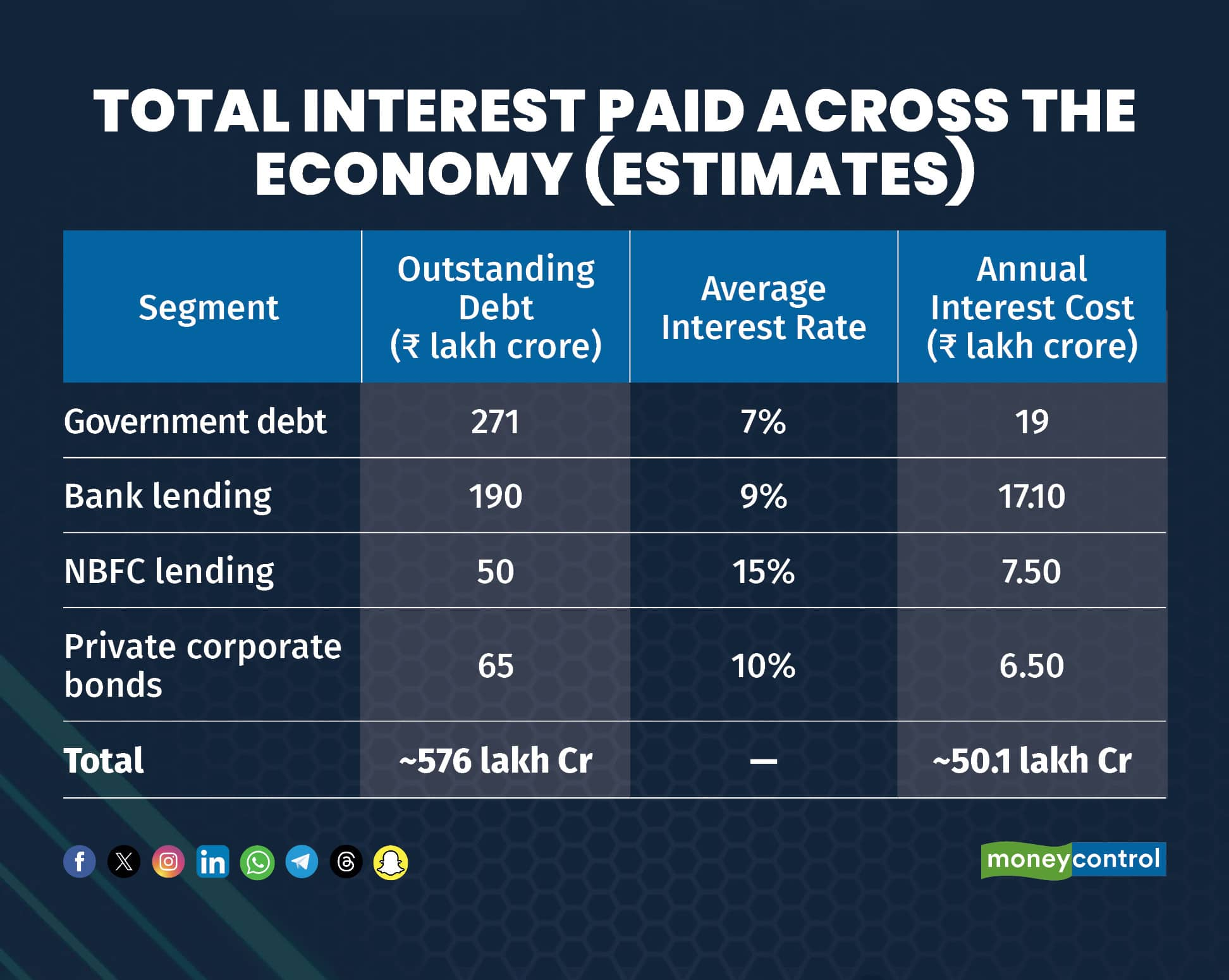

A nation paying too much for capital

India’s economy is caught in a high-interest equilibrium. Roughly 22% of Union government revenues are used to service interest on past debt. When extended across the economy, this translates into an annual interest bill of about ₹50.1 lakh crore, or 15.14% of India’s GDP.

This figure is striking when benchmarked globally. Developed nations such as Germany or Japan typically spend 4–6% of GDP on interest outflows. India’s much higher ratio underscores how deeply its capital structure absorbs national output merely to sustain past obligations. The consequence is less fiscal space for infrastructure, education, and welfare, areas essential for long-term productivity gains.

Why India’s WACC remains stubbornly elevated

Several structural bottlenecks explain why India’s WACC remains persistently elevated even as inflation moderates and financial markets deepen.

1) Underdeveloped Bond Markets

India’s corporate bond market equals only 18% of GDP, compared to over 100% in the US and nearly 80% in Japan. Over 99% of issuances occur through private placements, restricting transparency and participation. Limited secondary market liquidity and fragmented regulation keep yields high and access narrow, particularly for mid-tier companies.

2) Inflation and Monetary Policy

India’s inflation has averaged 5.9% in recent years, forcing the RBI to maintain relatively high policy rates. While inflation targeting has anchored expectations, it has also kept real rates positive and borrowing costs sticky.

3) Sovereign Risk and Ratings Ceiling

India’s sovereign credit rating, though recently upgraded to BBB, still sits just above the investment-grade threshold. This “sovereign ceiling effect” raises borrowing costs across the corporate spectrum by embedding a 2–3% risk premium versus AAA-rated countries. Without a sustained improvement in fiscal indicators and institutional depth, this ceiling will continue to cap India’s cost competitiveness.

4) Capital Account Restrictions

Despite gradual liberalisation, foreign participation in India’s debt markets remains limited. External Commercial Borrowings (ECBs) are still subject to end-use restrictions and approval processes. The lack of deep currency-hedging markets further deters global investors.

The economic cost of high WACC

A high cost of capital reshapes the economy’s growth pattern in several visible ways.

* Slower Capital Formation

Research shows capital formation drives up to 80% of productivity growth in emerging economies. India’s investment rate, at 32.2% of GDP, must rise to 36-38% to sustain 8% growth. A high WACC shrinks the universe of economically viable projects, especially in infrastructure, manufacturing, and renewable energy, forcing capital rationing even in high-potential sectors.

* Innovation Penalty

India’s startup ecosystem, responsible for 1.6+ million jobs and 10–15% of GDP growth, depends on patient, risk-tolerant capital. Elevated WACC compresses valuations, shortens funding runways, and deters long-term R&D. In contrast, economies with lower WACC such as South Korea demonstrate significantly higher rates of innovation diffusion and technology adoption.

* Employment and Wage Suppression

High borrowing costs limit capital investment per worker, constraining productivity and wage growth. The distortion is most visible in manufacturing and infrastructure, where capital intensity is essential for job creation. Over time, this imbalance leads to a growing share of income accruing to capital rather than labour, weakening consumption growth.

* Sectoral Imbalance

Capital-intensive industries such as energy, logistics, and heavy manufacturing face much tighter constraints than asset-light digital or service sectors. This uneven access limits industrial diversification.

Reforms for lower-cost growth

Achieving a reduction 200-400 basis points requires a coordinated set of policy, market, and institutional reform.

- Deepen the Bond Market

Simplify issuance processes, harmonise regulations between RBI and SEBI, and rationalise stamp duties across states. Introducing market-making mandates and electronic trading platforms will improve liquidity. Creating unified KYC and disclosure systems will lower barriers for issuers and investors alike.

- Expand Foreign Participation

Gradually lift investment limits on foreign investors in rupee-denominated corporate bonds. Modernise the ECB framework to provide easier global debt access. Simultaneously, build robust hedging infrastructure to manage currency risk, deepening the forex derivatives market.

- Improve Fiscal and Monetary Coordination

Continue the path of fiscal consolidation to reduce sovereign risk premiums. The government’s commitment to lower debt-to-GDP ratios will help elevate India’s credit rating, indirectly lowering private sector costs. The RBI can refine its inflation targeting framework to distinguish between supply-side and demand-driven inflation, allowing more policy flexibility.

- Strengthen Institutional Investors

Empower pension funds, insurance companies, and mutual funds with updated investment mandates. These institutions represent stable, long-duration capital that can anchor India’s bond markets. Policy should remove restrictive government quotas and allow greater participation in infrastructure and corporate debt.

- Build Credible Market Infrastructure

Invest in clearing, settlement, and risk management systems to reduce transaction costs and improve price discovery. Enhancing credit rating agency credibility and competition will also help rationalise spreads across the risk curve.

The urgency of reform cannot be overstated. India’s elevated WACC is a defining structural barrier to equitable growth. If India aspires to become a developed economy by 2047, reforming its financial architecture to lower this cost must be treated as an economic emergency, not a long-term aspiration.

A sustained reduction in India’s WACC will catalyse a virtuous cycle of higher investment, better jobs, and rising wages. The dividend of a cheaper, more efficient cost of capital is a more dynamic, innovative, and globally competitive India, capable of compounding growth sustainably for decades to come.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.