Jitendra Kumar Gupta and Madhuchanda DeyMoneycontrol Research

The first week of the quarterly result season wasn’t just about the performance of IT bellwether Infosys. There were quite a few hits and few misses that should vie for investor attention.

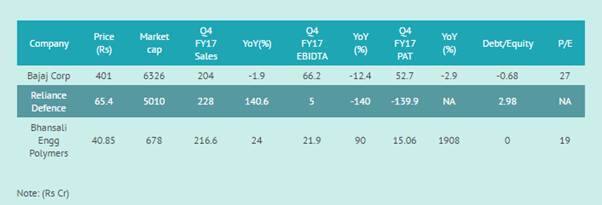

Bhansali Engineering Polymers, which operates an integrated petrochemical business manufacturing ABS, a raw material used by automobile, home appliance and telecommunication industries, saw a huge spurt in its reported profits as a result of benefits of operating leverage in the business. The company’s profits jumped to Rs 15.06 crore in March 2017 quarter as against Rs 75 lakh in the corresponding period.

While revenue grew by 24 percent, expenses rose by a modest 18 percent and the company managed to keep interest expenses steady despite higher topline.

For FY17, Bhansali made reported a profit of Rs 34.77 crore, which is more than double the profits it made last year. Markets have already cheered its strong financial performance as the stock saw a huge spurt on Monday.

The current market capitalisation of Rs 640 crore values the company at 18 times its FY17 earnings. However if we assume that profits will grow at current rate (Q4FY17 profit at Rs 15.06 crore), the valuation works out to a reasonable 10 times FY18 earnings.

Reliance Defence and Engineering, earlier known as Pipavav Shipyard, has seen significant improvement in execution and consistent growth in revenues over the last three quarters. The company has been sitting on a huge order book of Rs 5,700 crore and an annual sales turnover of Rs 563 crore: a healthy book-to-bill ratio of 10.1.

In the fourth quarter, turnover stood at Rs 228 crore as against Rs 69 crore in the corresponding quarter and Rs 121 crore in the previous quarter.

Consequently, it has broken even at the operating level - EBITDA of Rs 34.2 crore in FY17 as against EBITDA loss of Rs 147 crore last year.

Execution pick-up is critical as the company incurred a huge annual interest cost of Rs 625 crore. In the fourth quarter, the company earned an EBITDA of Rs 5 crore and had interest cost of Rs 164, thus leading to 139.7 crore loss at the net levels. While the valuation at 3.3 times its FY17 book value captures part of the optimism, the upcoming opportunity in the defence space makes it a candidate worth watching out for.

The other hit of the early result season was DCB Bank. The headline of drop in profit conceals the robust operating performance. NII grew 31 percent to Rs 220 cr on the back of 25 percent growth in interest earning and 10 basis points improvement in margins to 4.04 percent.

The decent profit before tax was helped by modest growth in provision. The reported profit decline was on account of tax benefit in the year-ago quarter as opposed to full tax in the current quarter.

Asset quality was stable with slippages largely flat at Rs 75 crore. Gross NPA rose 12 percent sequentially. Although relatively smaller banks are having to navigate in a competitive landscape, DCB is targeting aggressive growth. The steep run up in the stock has rendered the valuation a tad expensive – 2.6X trailing book. Investors need to keep this stock on their radar for a suitable opportunity.

The first week had a handful of disappointments. Notable among the losers was Bajaj Corp, a leading player in light hair oil market. In the final quarter of FY17, the company reported a close to 2% decline in sales, 12 percent decline in operating profit and 3 percent fall in after-tax-profit.

Bajaj Corp did not manage to improve sales despite substantial stepping up of expenditure on beefing up the sales team; this led to a significant decline in operating margin year-on-year.

For the full year, notwithstanding flat revenue and operating profit, lower exceptional loss compared to previous year resulted in 11 percent jump in profit to Rs 218 crore. Notwithstanding, the continued disappointing performance, valuation at 27X trailing earnings should protect the downside.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.