One of the most important features of CY20 was the build-up of household (HH) savings on account of many factors. Since a large part of the world economy was under physical lockdown, it led to a huge build-up of ‘forced savings’ among households.

Further, the highly uncertain economic environment increased the risk perception, leading to higher ‘precautionary savings’. Moreover, the fiscal response during COVID-19 was very swift and co-ordinated across the globe. As the fiscal support included direct cash transfer to the citizens, it helped replace lost income and/or supported minimum spending.

All these factors led to higher HH savings in many parts of the world. A comparison of actual HH savings vis-à-vis non-COVID-19 savings (counterfactual scenario) will reveal the level of excess savings. The accumulation of such excess savings over a period of time is ‘cumulative excess savings’.

According to the International Monetary Fund (IMF), “…as economies reopen, the release of excess savings accumulated during the pandemic could further fuel private spending…”. This, along with accommodative monetary and fiscal policies, has led to concern about the possibility of persistently high inflation. Therefore, tracking excess HH savings has become a very important indicator to understand the likely future trajectory of economic growth, and inflation.

Unfortunately, there is no official quarterly data on India’s household savings. Net financial savings, which account for 30-40 percent of household total savings, are published on quarterly basis by the Reserve Bank of India (RBI), and the recent data available is up to Q3FY21 (or Q4CY20). Physical savings are released on annual basis with a lag of 10 months (FY21 data will be published at end-Jan’22). In order to bridge this gap, we prepare in-house quarterly estimates of household savings in India using various monthly indicators.

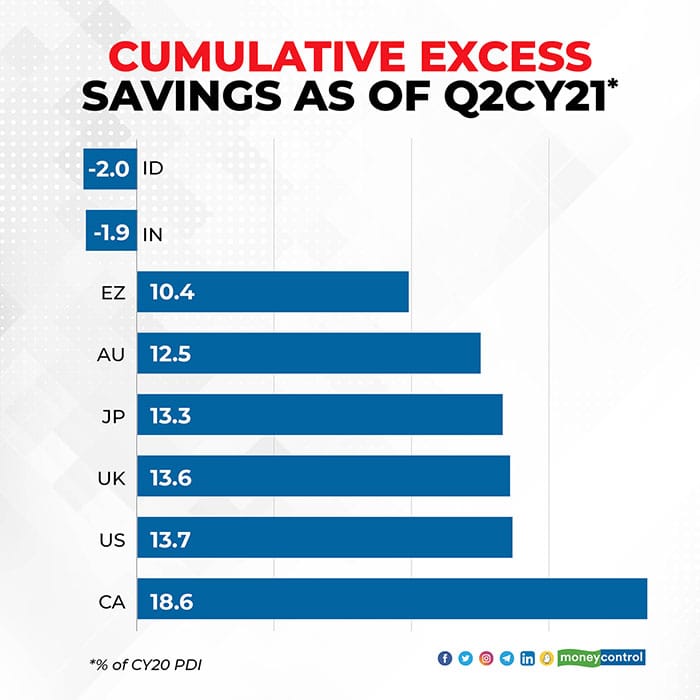

Our calculations suggest that in stark contrast to advanced nations, there are no cumulative excess HH savings in India (IN). India’s cumulative excess HH savings were -1.9 percent of CY20 personal disposable income (PDI) between Q1CY20 to Q2CY21, compared to 10-19 percent of PDI in advanced nations. The official data for Indonesia (ID), another developing economy, also reveal that the cumulative excess savings during the period were -2 percent of CY20 PDI, similar to that in India, and in contrast to rich nations (See graph below).

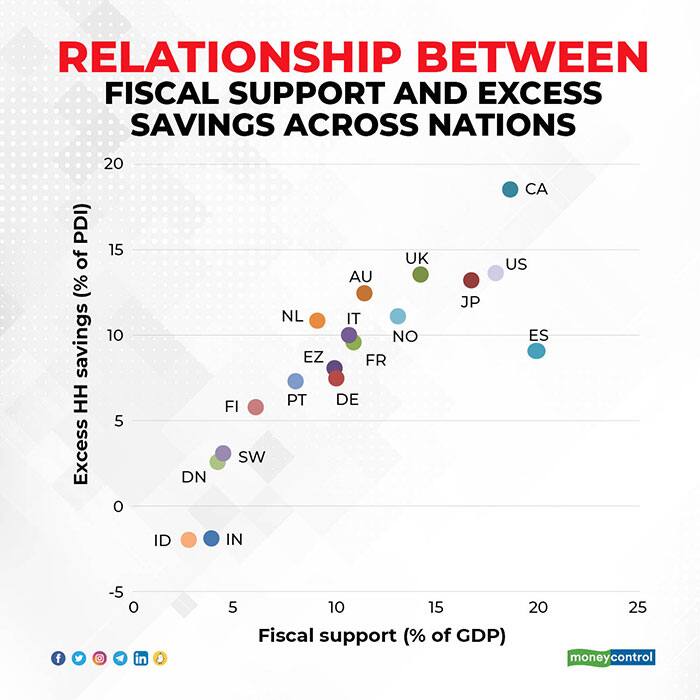

While it is difficult to attribute the contribution of various factors to the build-up of huge excess savings in advanced nations, a cross-country analysis confirms a very strong positive relationship between the cumulative fiscal support, and excess savings during the period. As the governments transferred cash/income to citizens during the lockdowns, their inability to spend it pushed savings higher automatically. Therefore, the greater the fiscal support, higher could be the extent of excess savings in an economy.

Very low level of cumulative excess savings in IN/ID is in line with the weak cumulative fiscal support as of 2QCY21, amounting to just 3.9 /2.7 percent of CY20 GDP. At the other end is Canada (CA)/the US, where the cumulative fiscal support amounted to 18-19 percent of GDP, leading to the highest cumulative excess savings as well (See graph below).

Overall, the debate about the overheating of the economy, and the resurgence of inflation in advanced economies hinges over the fact that there is a large build-up in excess savings in these nations. Nevertheless, the situation seems to be at the other extreme in developing economies. There are no excess savings in India or Indonesia, which alleviate the potential fears of over-heating and inflationary concerns in these nations.

Therefore, it is necessary that Indian authorities consider these differences carefully while making appropriate policies, rather than giving too much weightage to the US. This is exactly what was done by RBI Governor Shaktikanta Das, when he called it ‘unfair’ to compare the Indian economy with the US.

The financial position of the Indian HH sector is very weak, which is in stark contrast to most rich nations. COVID-19 only exacerbated that weakness since the households incurred the maximum share of COVID-19-led income losses in India.

Overall, we argue that India’s economic growth is likely to remain subdued, which alleviate the inflationary concerns also.

Nikhil Gupta is Chief Economist, Motilal Oswal Financial Services.

Views are personal and do not represent the stand of this publication.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.