Amid the turmoil in big banks, small & niche financiers with a strong track record grabbed our attention. AU Small Finance Bank (AU) and MAS Financial Services (MAS) had a stellar debut at the bourses last year, and although it has not been a dream run for them since listing, the fundamentals stand tall and ought to be taken cognisance of.

AU commenced its journey from Jaipur, Rajasthan in 1996 and got registered as an NBFC in 2000. The company converted into a bank in April, 2017. Currently, 82 percent of its loans are to the retail segment (vehicle finance, MSME and SME) and nearly 99 percent of the portfolio is secured.

The Company has reported robust financials with penetration in the under-served markets. The revenue has risen by 37 percent and profitability by 47 percent with 29 percent compounded annual growth rate (CAGR) in disbursement, and 30 percent in assets under management in the past four years.

The strategy of continuous expansion across regions has now led to presence across ten states and one Union Territory with significant concentration in Rajasthan, Gujarat, Maharashtra and Madhya Pradesh.

AU’s transition to a bank has been a smooth one with disbursements showing a strong traction of 47 percent. However, the progress made in garnering deposits has been a standout. In a short span of less than three quarters, deposits constitute 34 percent of total liabilities with 38 percent of the deposit base being low cost. This has aided in lowering cost of funds that should shield margin as the bank experiences margin pressure from regulatory costs and a lower yielding lending book.

AU is also bolstering the distribution business of mutual funds, life insurance and health insurance while foraying into newer lending products like gold loan, agri SME loan, consumer durable loan and housing loan.

The bank had up-fronted cost in this conversion journey, so the cost-to-income ratio has been very high. However, as the bank leverages its distribution network, the cost ratios should start moderating.

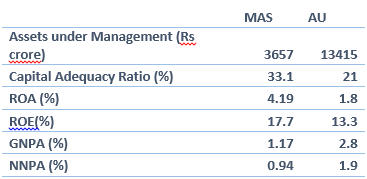

The core underwriting skill has aided the company in maintaining a decent asset quality across cycles. The slightly elevated level of NPA (non-performing assets) with Gross NPA at 2.8 percent and net NPA at 1.9 percent has been on account of reduction in period for recognition of dues to 90 days (from 180 days in the case of NBFCs) after its conversion to a bank, and the stress in the borrower markets on account of GST. However, slippages have been falling.

The bank is well capitalised (Capital Adequacy Ratio) at 21 percent. This intrinsically profitable business will generate above industry return ratios and continue to trade at a premium. Hence, investors got to buy every dip for a long journey with a solid franchise.

Unlike AU which is a scheduled bank now, MAS Financial continues to remain a well-run niche NBFC (non-banking finance company). This Gujarat-headquartered NBFC has been in existence for more than two decades.

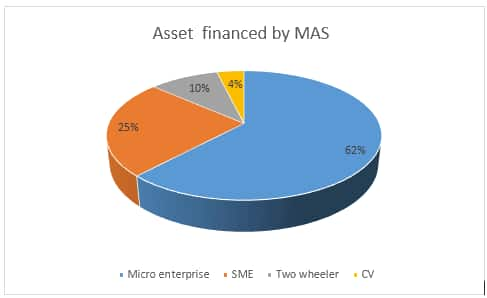

Currently, the company operates across six states. The business primarily focuses on loans to small businesses and individuals. It has four product categories – MSME, SME, two wheeler and CV, and a housing finance subsidiary catering to affordable housing.

What stands out for MAS is the knowledge of its end market and superior execution.

MAS has a unique sourcing model. In addition to sales team, the company has entered into commercial arrangements with a large number of sourcing intermediaries, including commission-based Direct Selling Agents and revenue sharing arrangements with various dealers and distributors where part of loan default is guaranteed by such sourcing partners. MAS has 106 small NBFC partners for sourcing business. The assets generated by these NBFCs are hypothecated to MAS. Nearly 56 percent of the assets have been contributed by these NBFCs.

MAS has stringent qualitative and quantitative evaluation criteria that keeps a check on delinquencies. This is reflected in the numbers with the Gross NPA and net NPA at 1.17 percent and 0.94 percent, respectively.

The company is very well capitalised (Capital Adequacy Ratio at 33 percent) and should have a steady and long road to profitability ahead. Hence, the valuation is amply justified.

While catering to the “bottom of the pyramid” looks like a profitable proposition, few have been able to execute the business with the skill exhibited by companies like AU and MAS. Both these companies have marquee investors in their shareholding list. Going forward, while competitive intensity will remain high, the ones with long-term experience will have the last laugh.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!