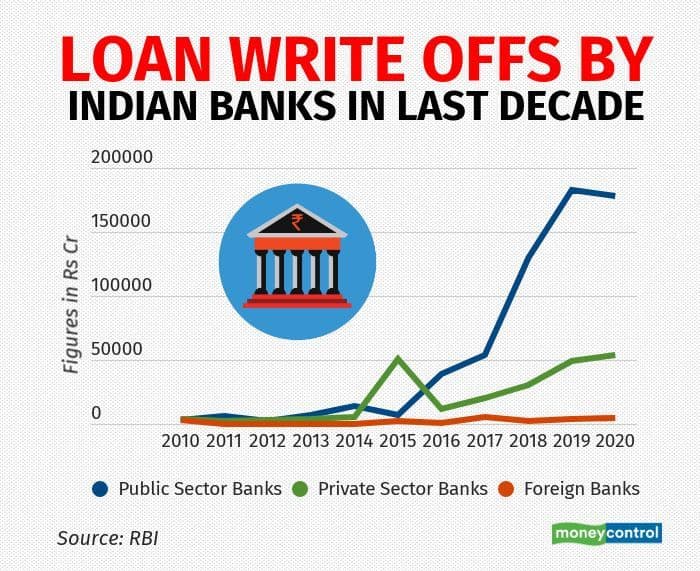

Indian banks wrote off loans worth around Rs 8,83,168 crore in the last ten years, a significant chunk of which came from government-owned banks, the latest data from the Reserve Bank of India shows.

Of this, public sector banks (PSBs) alone wrote off Rs 6,67,345 crore worth loans since 2010. This is about 76 percent of the total written-off loans in the decade, while private banks wrote off loans worth Rs 1,93,033 crore constituting about 21 percent of the total chunk. Foreign banks wrote off Rs 22,790 crore loans or 3 percent of the total write-off, the RBI data showed.

In the financial year 2019-2020 alone, banks wrote off a total of Rs 2,37,206 crore or about a quarter of the total loan write-offs in the last one decade. Of this, Rs 1,78 lakh crore was by PSBs and Rs53, 949 crore by private banks. These figures do not take into account the loans written off by small finance banks, which is a relatively smaller portion.

Individual banks

Among the banks, State Bank of India (SBI), the country’s largest lender by assets, wrote off loans worth Rs 52,362 crore in FY20 becoming the largest contributor to the pie in FY20 followed by Indian Overseas Bank (Rs 16,406 crore), Bank of Baroda (Rs15,886 crore) and Uco Bank (Rs12,479 crore), the data showed.

Among private banks, the biggest loan write-off during the year was by ICICI Bank, which wrote off loans worth Rs 10,952 crore followed by Rs 10,169.27 crore by Axis Bank and HDFC Bank which wrote off Rs 8,254 crore, the data showed.

Are these figures alarming?

Loan write-off happens when efforts for resolution fails and hence increase in loan write-off should be seen as a sign of stress in the banking system. However, it is important that these figures need to be seen in context.

As a percentage of total advances in the banking system (around Rs 92.6 lakh crore as on March 2020), total written-off loans during the year stand at 2.56 percent. In the year before (when Rs 2,36,312 crore of loans were written off), this was 2.72 percent. This means as a percentage of the total outstanding loans in the banking system, yearly loan write-off figures have come down slightly.

Loan write-offs happen when banks feel chances of recovery from borrower account are almost nil. Lenders need to make provisions (money set aside to cover the losses) against such accounts. The provisioning can rise up to 100 percent of the loan fully goes bad. Hence, write-offs impact the profitability of banks.

“ Loan write-offs went up last year because many expected recoveries didn’t happen. This was due to the economic situation,” said Sidhharth Purohit, an analyst at SMC Global securities.

“Even if the loan is written off, banks have to provide for the losses and hence loan write-offs do not come as a surprise to the markets, Purohit said. Also, some recoveries can happen from such accounts in future, Purohit said.

RBI caution

In its latest Trend and Progress report, the RBI said Scheduled Commercial Banks’ (SCBs) gross non-performing assets (GNPA) ratio declined from 9.1 percent at end-March 2019 to 8.2 percent at end-March 2020 and further to 7.5 percent at end-September 2020. But the decline in gross NPAs in the banking system was largely aided by loan write-offs, the central bank said.

“The reduction in NPAs during the year was largely driven by write-offs. NPAs older than four years require 100 percent provisioning and, therefore, banks may prefer to write them off,” the RBI said.

“In addition, banks voluntarily write off NPAs in order to clean up their balance-sheets, avail tax benefits and optimise the use of capital. At the same time, borrowers of written-off loans remain liable for repayment,” the RBI said.

The modest GNPA ratio of 7.5 percent at end-September 2020 veils the strong undercurrent of slippage, the central bank said.

Further, large borrowal accounts or accounts where exposure is Rs 5 crore and above, constituted 79.8 percent of NPAs and 53.7 percent of total loans at end September 2020, the RBI said.

During 2019-20, PSBs’ GNPA ratio as well as the ratio of restructured standard assets to total funded amounts emanating from larger borrowal accounts trended downwards. On the contrary, private sector banks experienced an increasing share of NPAs in respect of such accounts, the RBI said.

The share of SMA-0 (Special mention accounts) witnessed a sharp rise in September 2020. These accounts are those where principal or interest payment not overdue for more than 30 days but account showing signs of incipient stress.

This may be an initial sign of stress after lifting of moratorium on August 31, 2020, the RBI said. However, the share of other categories of SMAs, SMA-1 and SMA-2 remained at a relatively lower level, the RBI said. SMA accounts are accounts where repayment is overdue for 60-90 days, the RBI said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.