Say you start with an investment of Rs 1 lakh today. After a year, it grows by 100 percent and your investment becomes Rs 2 lakh. Sadly, in the second year, your investment falls by half; Rs 2 lakh becomes Rs 1 lakh. How much is your return?

Your average return in this period may be an arithmetic mean of +100% and -50%, which is 25 percent. But the CAGR of the portfolio will be 0 percent as the portfolio did not make any money in two 2 years. And this is the right conclusion. You started with Rs 1 lakh and after 2 years, you are still at Rs 1 lakh.

But as you may have noticed, CAGR hides a lot. It never gives you the complete picture.

CAGR hides volatilityTake for example an investment where your money experiences an annual return sequence of +12%, +2%, +49%, (-)19% and +28%. The final CAGR over 5-year period will be around 12%. So CAGR actually hides the volatility in the period under consideration (where your investment moved up +49% and also fell by -19%) to deliver a smooth-looking number (12% in this case).

Basically, CAGR is a mathematical construct that gives the average effective but theoretical return, which if available every year, will deliver the same final amount as delivered by a sequence of varying annual returns. The problem is that it only considers the starting and ending values to calculate the returns and ignores the fluctuations in between.

So in the earlier example, a CAGR of 12% in a 5-year period does not mean that you will get 12% every year.

Picking mutual funds

Time and again, investors are advised to pick funds that have established track records. One common proxy of a good track record used by investors is CAGR. But just relying on CAGR to select the right funds for your portfolio is not a good idea. Let’s see why.

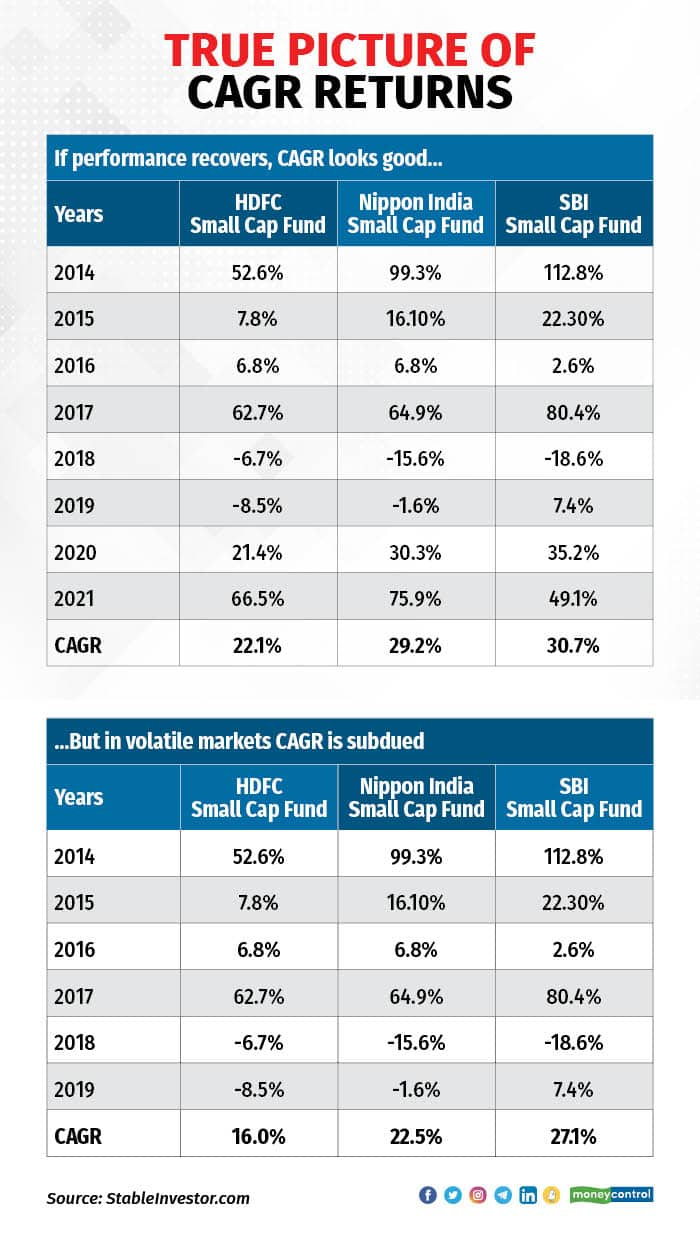

Let’s compare the annual and CAGR returns of three of the largest active small-cap funds in India, namely HDFC Small Cap Fund, Nippon India Small Cap Fund and SBI Small Cap Fund.

If we use the annual return data from 2014 to 2021, here is the CAGR (last column in the table) for the three funds.

As you can see, in this time period, all 3 funds have given great returns (CAGR) ranging from 22.1% to 30.7%. But these figures hide the volatility in between. Look at the bad sequence of returns in 2018 and 2019. Also, all the funds did pretty well in the last 2 years which may have pushed up CAGR returns.

What if we consider the period 2014 to 2019 only?

The returns moderate to 16-27%.

Still, the returns look great, although not as great as the previous ones. But the point being made here is that depending on which start or end year you drop from the analysis, the CAGR return profile will change and without any regard for intermittent volatility.

Note – The above funds have been chosen for illustrations only. Please do not consider it investment advice or recommendations. How AMCs use CAGR to promote/hide DataTypically, mutual fund houses desire higher inflows and higher corpuses. That also makes business sense for them. However, some fund houses project CAGR returns a bit louder than the rest when such figures look favorable, especially in releasing advertisements.

Suppose you invested Rs 10,000 in a fund in 2014. This grew to only Rs 14,000 by 2019 giving a CAGR (2014-2019) of just about 7%. Now, the market ran up in 2020 and your investment reached a value of Rs 28,000. Now if you calculate CAGR for the period 2014-2020, it comes to a much respectable 18.7%.

The AMC will now start using the CAGR figure of 18.7% to promote the scheme, comfortably choosing to ignore that it was just a one-year return (in 2020) that pushed up the number. Also, the CAGR fails to reveal (or comfortably hides) that the fund was not a great performer for the major part of the investment period. Many times, such 1-year performances push up funds higher in fund rankings.

So the use of CAGR in such cases can be misleading. Investors and advisors need to see through the data, slice and dice it, before deciding which funds to pick for an MF portfolio.

CAGR remains a useful tool to assess investment performance for a given period. But it has its shortcomings which can be used by people with vested interest to show you things they want to. So be careful about CAGR as a concept. At least don’t depend entirely on it to make your investment decisions.

This is also why rolling returns are a better tool to judge a scheme’s performance. A scheme’s rolling returns takes multiple entry and exit points and that capture the volatility well.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.