The central government has approved an interest rate of 8.1 percent for Employees' Provident Fund Organisation's (EPFO) nearly five crore members, the retirement body announced on Friday.

EPFO had declared an interest rate of 8.1 percent for financial year 2021-22, down from 8.5 percent for 2020-21. Faced with criticism for declaring the lowest rate in 40 years, India’s finance minister Nirmala Sitharaman had batted for the decision.

"It is yet to come to Finance Ministry for approval, but the fact remains that these are the rates that are prevailing today and it (EPFO) is still higher than the rest of them," Finance Minister Nirmala Sitharaman had said, while defending the rate cut.

The interest rate for FY 2021-22 has been reduced to 8.1 percent from 8.5 percent earlier. To make her case, the finance minister cited returns of small saving schemes such as public provident fund (PPF), Sukanya Samriddhi Yojana (SSY), Senior Citizens’ Saving Scheme (SCSS) and the State Bank of India’s ten-year fixed deposits.

Sitharaman was right.

Also read: EPFO cuts interest rate to 8.1 percent for 2021-22, lowest in 43 years

EPF outperforms other fixed income investmentsThe Employees Provident Fund Organisation’s (EPFO) Central Board of Trustees declares the interest rate every year after deliberations. It is then credited to members’, i.e., employees’ account, after the finance ministry ratifies it. The governing body, which comprises the labour minister, members of labour unions and other stakeholders, announced the rate for financial year 2021-22 on March 13.

This is the lowest rate that EPFO has announced in over 40 years, causing heartburn among EPFO’s 60 million members, or salaried employees. However, EPF as well as its extension VPF (voluntary provident fund) continue to be indispensable as retirement planning tools.

Also read: Why the interest credit to your EPF account gets delayed every year

Here are three reasons why EPFO continues to score over other, secure, fixed income avenues.

EPF contribution is mandatoryFor one, EPF contribution of 12 percent of your basic salary (and dearness allowance, if any) is mandatory. You do not have a choice of directing this amount - that is deducted by your employer every month – elsewhere.

However, even those who contribute a higher amount voluntarily (through VPF) will find value in this trusted retirement planning avenue due to relatively higher returns and tax benefits that it offers.

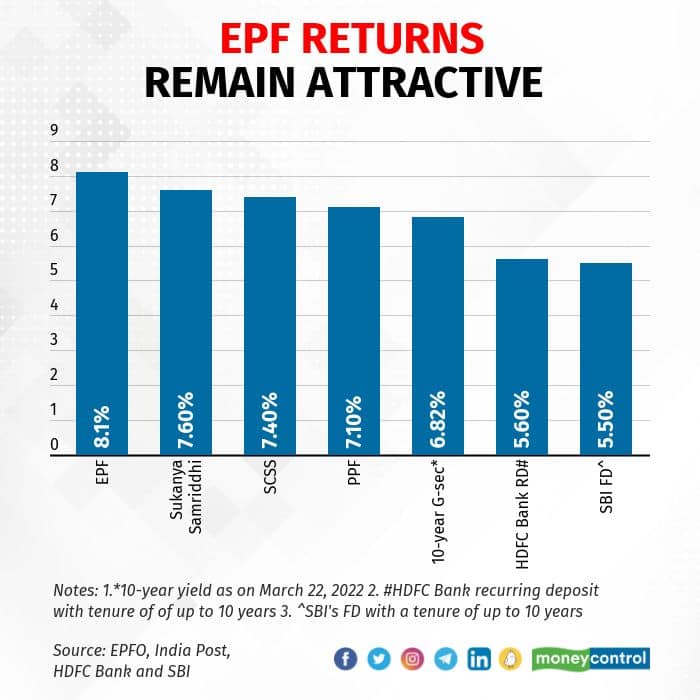

Current rate is higher than comparable fixed instrumentsEven with interest rate of 8.1 percent, it outshines returns of post office small saving schemes and bank fixed deposits. These fixed income instruments, too, are considered safe and offer secure returns. However, their returns are comparatively lower. For instance, the highly popular public provident fund offers an interest rate of 7.1 percent, while the Sukanya Samriddhi Yojana can fetch 7.6 percent per year. Senior citizen saving schemes (SCSS) and the State Bank of India’s 10-year fixed deposits yield 7.4 percent and 5.5 percent per annum respectively.

Multitude of tax benefits on offerNot only is the declared EPF rate is higher than those of other secured instruments, but more importantly, more tax-efficient too.

EPF is exempt from tax at the investment, accumulation and maturity stages, though interest earned on EPF contributions of over Rs 2.5 lakh is subject to tax from financial year 2021-22. Firstly, your annual PF contribution can be claimed as deduction under section 80C. Interest earned over the years will not be taxed, unless you are a high-earner contributing over Rs 2.5 lakh per year or breach this limit through higher VPF contributions.

The amount that you receive at maturity is also tax-free. Interest earned on SCSS and bank fixed deposits are taxable as per the slab rate applicable to you. PPF and Sukanya Samriddhi Yojana, offer tax benefits similar to EPF, but yield relatively lower returns (see table).

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.