As India's benchmark indices scaled dazzling heights on November 27, the investment landscape feels both exhilarating and precarious. BSE Sensex and Nifty 50 touched, marked all-time peaks amid robust economic signals during the year. Yet, this euphoria masks a perennial investor dilemma: With markets at such lofty valuations, should one deploy a lump sum into a diversified equity fund right away, or opt for a steady monthly Systematic Investment Plan (SIP)?

The choice pits the allure of immediate compounding against the safety of gradual entry, especially when timing feels impossible.

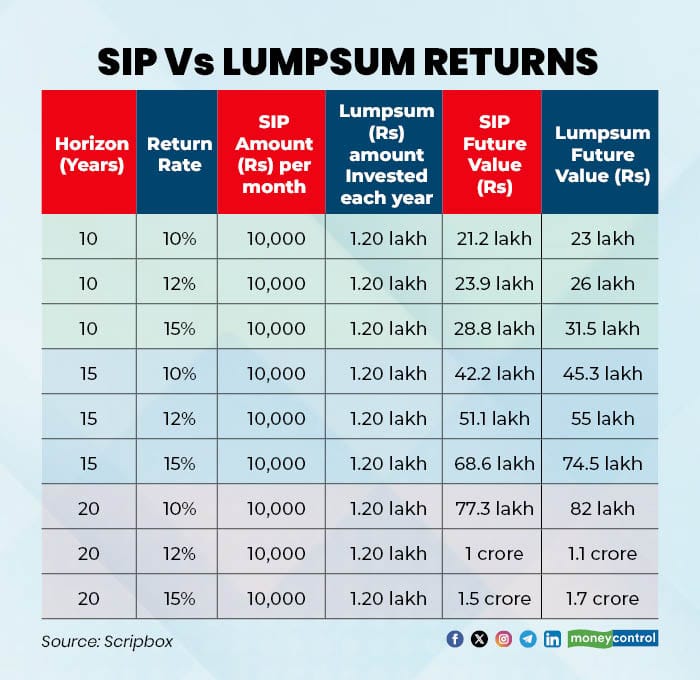

The mathematical case for lump sum investing

Pure mathematics favors the lump sum, as the full amount compounds from day one, outpacing the staggered SIP inflows. Consider this illustration, assuming annual returns of 10%, 12%, and 15%—realistic for diversified equity funds over long horizons. Both strategies invest Rs 1.2 lakh annually (lumpsum) and SIP via Rs 10,000 monthly.

The table reveals, lump sums yield higher returns because of extended compounding. "Lump sum investing has a natural mathematical advantage because the money stays invested for the full year and compounds for longer," said Charu Pahuja, Director & Chief Operating Officer at Wise Finserv. However, this edge assumes steady market climbs— a rarity in volatile equities.

Also read | How Labour Code 2025 can shrink your salary, if basic pay is below 50% CTC

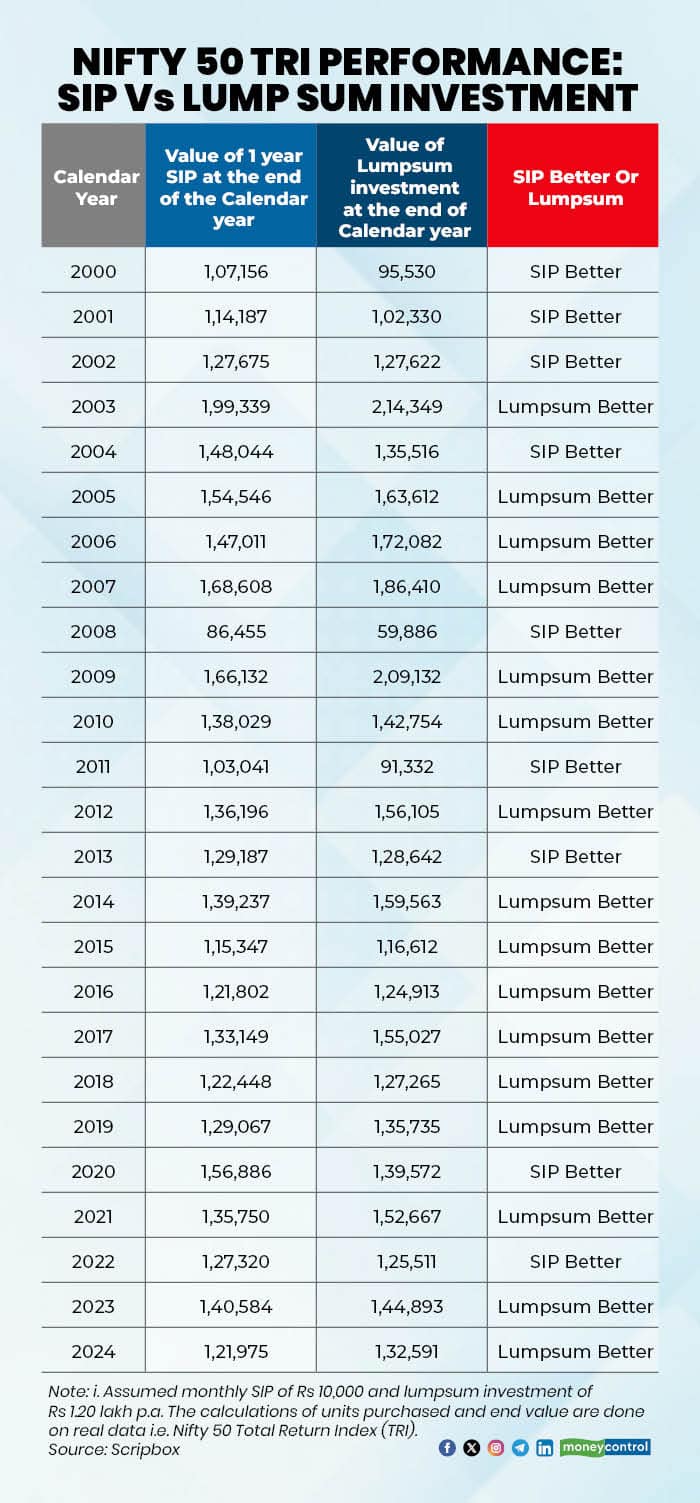

SIP's edge in volatile markets

Atul Shinghal, Founder and CEO of Scripbox, cautions that such models overlook "sequence risk," where early drawdowns erode lump-sum gains. "If the market falls 20-40 percent immediately after investing a lump sum, the long-term return drops sharply," he explains, drawing from Nifty 50 Total Return Index (TRI) data. Real-world analysis shows lump sums thriving in bull runs but faltering in choppy starts, while SIPs close the gap through rupee-cost averaging.

"SIPs actually benefit from market volatility, snatching up more units when prices dip," Pahuja said.

During downturns like 2008 and 2020's COVID crash, units bought during the crash boosted SIP returns dramatically in the years that followed.

Why SIPs align with everyday investors

For most salaried investors, SIPs align with monthly cash flows, fostering discipline without timing stress. They reduce panic-selling odds and match behavioral realities. Shinghal said, "SIPs match monthly income patterns and build long-term wealth automatically, especially valuable amid frequent 10-20 percent corrections.”

Also read | What to expect after switching from NPS to UPS post-deadline of November 30?

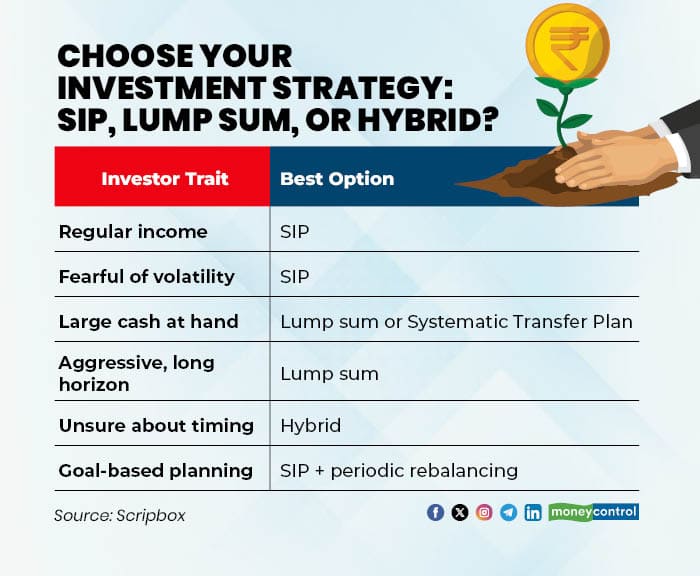

Scenarios where lump-sum investment shines

That said, lump sums shine in select scenarios. Deploy them post-corrections, with windfalls like bonuses, or for risk-tolerant profiles eyeing long-term investment of more than 15 years. Shinghal said, "Lump sum works best when market valuations are reasonable or cheap, and the investor has a high-risk appetite."

Blending strategies: The hybrid approach

By combining SIPs, lump sum investments, and tactical top-ups, you can create a winning formula. “Keep SIPs as your core wealth-builder, pumping in regular investments. When markets dip or surplus funds arrive, deploy lump sums to seize opportunities. And don't forget to top up your SIPs annually, keeping pace with your rising income,” said Pahuja.

“Hybrid strategy smooths out entry prices, mitigates timing risks, and lets you capitalize on market opportunities – a flexible and effective way to navigate India's dynamic markets,” said Shinghal.

This hybrid approach marries discipline with flexibility, helping you navigate market ups and downs while building wealth over time. Wealth creation favors consistency over perfection—choose what sustains your journey.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.