Consider this. If you were drawing up a plan to secure your child’s future and had the choice between saving up for her education or her retirement, what would you choose?

Given that her retirement would be decades away, it is most likely that you would prioritise creating an education corpus for her. Then, there is your own retirement to take care of.

According to an HSBC study, 78 percent of affluent Indian parents either want to send their kids abroad to pursue studies or have already done so. This, despite the fact that the cost of education in countries such as the UK and the US could account for 64 percent of their retirement savings. Nearly one-third (27 percent) are even willing to sell their assets to fund their kids’ overseas education.

In this backdrop, it is unlikely that parents can afford to set aside substantial funds to build their children’s retirement corpus, when their own retirement preparedness ought to be priority.

What is NPS Vatsalya?

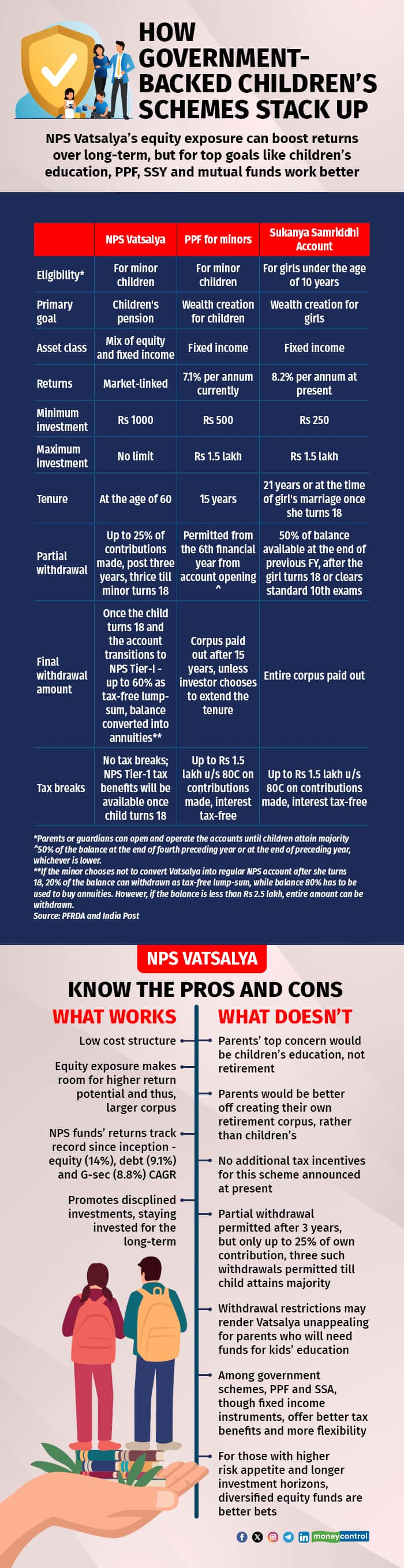

Announced in Budget 2024 and rolled out on September 18, NPS Vatsalya is a pension scheme that allows parents to invest in the name of their children up to the age of 18 years.

Once minor children attain the age of majority (18 years), it will transition to a regular NPS account. The objective is to create a corpus for their children over the long term. Parents or guardians can contribute a minimum of Rs 1,000 annually, without any maximum investment limit.

The effect of compounding over the long-term can ensure that even smaller amounts invested regularly grow into a substantial corpus by the time children turn into adults and start drawing their own income. It will also inculcate savings discipline for children as also their parents.

Moreover, NPS funds have delivered impressive returns since inception (2009 in the case of private sector NPS) – equity schemes have yielded 14 percent returns, corporate debt 9.1 percent and G-sec 8.8 percent.

“Retirement planning is one of the most ignored financials goals for an Indian investor. NPS Vatsalya addresses it to some extent by giving it a head-start and that too from a parent. Parents having seen more ups and downs of life, are more in tune to the need of building a retirement corpus,” says Amol Joshi, Founder, PlanRupee Investment Services.

Investing a small sum should be manageable, he says. “Though most parents would first need to be self-sufficient to manage their own retirement; however, if cashflow permits, making a small Vatsalya beginning is a good idea – Rs 1,000 minimum per annum is a manageable sum.”

Also read: NPS Vatsalya: How to invest in this scheme? Understand the features, benefits, eligibility and more

The flipside

Do not assume that you can easily dip into this corpus to meet your children’s education needs in the interim, if required. The scheme allows partial withdrawal of up to 25 percent of your own contribution - and not the entire account balance that includes returns - after a lock-in period of three years. Three such partial withdrawals are permitted till the child turns 18.

Once the child attains majority, she has the choice of withdrawing up to 20 percent as lump-sum while the balance has to be mandatorily used to buy annuities. Else, it gets converted into a regular NPS Tier-I account, where 60 percent of the corpus can be withdrawn as tax-free lump-sum when the accountholder turns 60, with the balance being converted into annuities.

“Individuals find it challenging to channel savings into retirement schemes due to high expenses and short-term goals. To expect people who may not be saving for their own retirement to think of their children’s old age is a bit much to digest,” says Mrin Agarwal, Founder, Finsafe India.

Are PPF and Sukanya Samriddhi better options?

Unlike NPS-Vatsalya, neither the public provident fund (PPF) for minors nor Sukanya Samriddhi Account (SSA) offer any exposure to equities. Yet, they are popular among parents as they offer secure, higher-than-fixed-deposit returns and come with an exempt-exempt-exempt structure. Investors get 80C tax deductions of up to Rs 1.5 lakh under the old tax regime when they contribute to these schemes, the returns earned during the tenure do not attract any tax and final maturity proceeds are tax-free too.

“Education will help children be independent and be capable of planning their own retirement. As such, corpus for education needs to be planned separately with higher degree of importance. This can be done via PPF, Sukanya Samriddhi, as well as equity mutual funds if you have an investment horizon longer than 10 years,” says Joshi. Financial experts say equity is the best asset class for creating long-term wealth if you can stay invested over the long-term and can stomach market volatility in the interim.

PPF and SSA, too, come with lengthy maturity periods (15 years in the case of PPF and maximum of 21 years in the case of SSA). Also, the maximum contribution is capped at Rs 1.5 lakh. Pure debt exposure could mean lower return-generating capability when compared to NPS Vatsalya where equity allocation can be as high as 75 percent, but these schemes’ government-guaranteed returns and more flexible withdrawals are huge advantages.

“If parents invest in these instruments in the name of their children, they will be able to access the funds around the time the kids need funds for their higher and overseas education. In contrast, funds in NPS Vatsalya will add to the children’s retirement corpus. So, it might allow parents to create a sizeable kitty by the time children turn 18, but they may not always be able to utilise it if the education corpus falls short of requirements,” says Mrin Agarwal, Founder, FinSafe India.

Besides PPF and SSA, parents with a risk appetite can also consider diversified mutual funds to create an education corpus. “Diversified mutual funds could do better due to higher equity component – as it will be 100 percent vs 75 percent in NPS/Vatsalya. However, the investor should be mindful that it is essential to remain invested for long periods of time, just like it would happen in NPS. Let short-term market movements not deter you,” says Joshi.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.