Despite the Reserve Bank of India (RBI) having offered loan moratorium to borrowers in 2020, many customers faced other penalties.

Some banks and non-banking finance companies (NBFC) levied ECS (electronic clearance service) bounce charges, every time their lenders’ equated monthly instalment (EMI) payments failed to go through. This charge is in addition to a higher interest and late payment fee.

More levies

In August 2020, Trivandrum-based Srinivas Kumar paid Rs 6,500 as bounce charges, as Bajaj Finance made 11 attempts to deduct his EMI from his bank account.

“As long as the payments are timely, there is never a need for representation of the ECS again in the same month. However, if the customer has missed his payments, the lender may choose to present the ECS multiple times to collect the dues,” says Ravi Subramanian, MD and CEO of Shriram Housing Finance.

Now each such attempt – when met with a failure – attracts an ECS bounce charge.

Srinivas Kumar says that he had applied for a loan moratorium with Bajaj Finance. A spokesperson of Bajaj Finance says, “Considering that these are testing times for customers, we have been very accommodating and understanding with them. A customer could reach out to us through any of the service channels – calls or mails – and their request is given due consideration. Following the guidelines issued by the regulator, we earlier offered moratorium and loan restructuring facilities to our customers. We also made our customer aware about the moratorium process through the communication across multiple mediums.”

Experts that Moneycontrol spoke to said that banks and NBFCs ought to show compassion in pandemic times. “They should treat their borrowers softly and take an easy approach in such times,” says Yogi Sadana, CEO of CASHe, a digital lending platform.

Also read: Do you know how much your bank charges and penalises you? Read on

Twice the charges

If your lender and your bank are different, ECS bounce charges multiply.

Sourabh Shah (name changed) learnt this the hard way as he was charged Rs 26,000 by a leading NBFC and Rs 15,000 by a private bank for ECS bounce during April-July 2020. “My account was hit 10 times each month for two loans. They took away whatever little amount was available in my bank account. When we are facing a financial crisis, such charges add to the crunch,” says Shah.

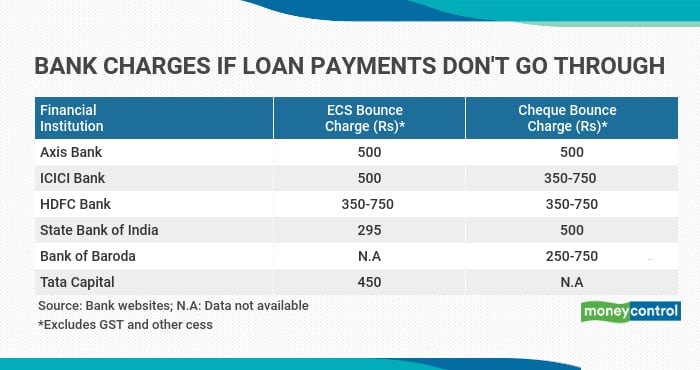

One reason behind the high bounce charges is that they multiply with every attempt. For instance, ICICI Bank levies Rs 350 for the first cheque bounce, but Rs 750 for the second instance in the same month. HDFC Bank charges similar amounts.

Are the charges justified?

“From the loan contract standpoint, these are legal charges and rightly levied by the banks if the borrower has not applied for loan moratorium and defaulted on instalments,” says a senior official with a leading NBFC in Mumbai requesting anonymity.

Says Sadana, “PSU banks have lower charges compared to private banks. Foreign banks charge more as they are premium banks.”

For instance, the State Bank of India (SBI) charges Rs 295 as ECS return charges.

But to ensure that the charges do not escalate, there are rules in place. “The Negotiable Instruments Act, 1881, states that if a bank or financier cannot collect the due amount by presenting an instrument (in this case ECS, cheque etc.) more than two times in a month, it has to get a written permission from the borrower and change the instrument (cheque, ECS, draft etc),” says Vipul Patel, CEO and founder of loan advisory MortgageWorld.

What to do, if faced with high bounce charges?

Talk to your bank and see if you can get a waiver on these ECS bounce charges. Shah was refunded the amount earlier deducted, by both his bank and lender. “If the charges are still levied unfairly, the customer should approach the banking ombudsman for redressal under the RBI’s mechanism,” suggests Sadana.

Dance tutor Kruthika saw that Rs 50,000 was deducted from her account as bounce charges. She spoke to her bank and asked for a reversal of charges. “Kotak Mahindra Bank reversed Rs 45,000 worth of charges after I revealed the financial crisis that I faced for in the month of January and February, when the digital lender Dhani tried to access my account 100 times during a span of three months,” she says.

Check your loan agreement. You may have authorized your lender to hit your bank account a particular number of times in a month. “If your lender has hit your account more than that, you have a right to complain,” says Sadana.

In the worst case, you can de-activate the ECS or NACH mandate and stop paying your EMIs. This ensures that the auto-clearing facility doesn’t hit your account on multiple instances and the subsequent levies can be avoided. But remember: you still have to pay off your loans. And the interest and late payment fee on the loan keep mounting. It takes a minimum of seven days to de-activate the NACH mandate request and hence do it at least a week prior to the EMI date.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.