Soon, you will be able to buy a standard home insurance cover from any general insurance company, except health insurers, in India. The Insurance Regulatory and Development Authority of India (IRDAI) has issued guidelines on the standard home insurance policy – Bharat Griha Raksha – that will be available from April 1, 2021. In 2020, the insurance regulator had framed standard clauses for term insurance, health, COVID-19, personal accident, travel and vector-borne diseases covers. A home insurance policy with uniform clauses is the latest in this list. Like in the case of other standardised covers, the premium will be decided by insurers, but clarity is awaited on whether zone and geography-based pricing will be allowed.

A cover for your dwelling unit

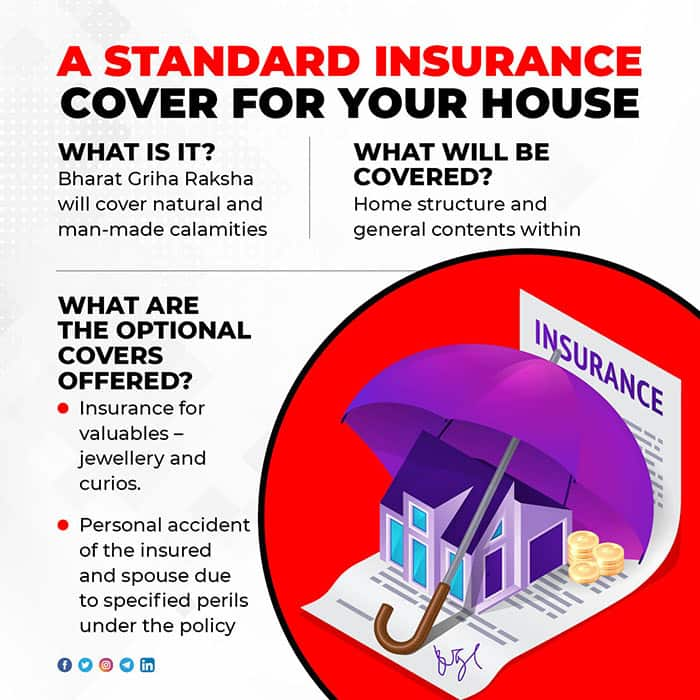

The policy will pay for damages to your house structure due to natural and man-made perils. These include fire, storm, cyclone, typhoon, tsunami, flood and even thefts, riots, strikes and acts of terrorism. What about a gas cylinder blast/short circuit caused by negligence, etc.? These accidents are often seen happening in small Mumbai homes. Now, they are not specifically mentioned in the policy wordings, but could be covered under ‘explosion’ or ‘implosion’ clauses. Full clarity is still awaited on policy wordings and the implied coverage.

The sum insured of your house will depend on your property’s carpet area and prevailing cost of construction as on the policy commencement date. You can choose between policy tenures of one to 10 years.

General contents – for instance, television set, refrigerator or furniture – in your house will also be covered. Unlike some home insurance plans in the market, you need not necessarily declare details of the contents. These will covered to the extent of 20 percent of the sum insured for the house structure, up to a maximum of Rs 10 lakh. However, if you wish to buy higher coverage for the contents in your house, you will have to share detailed information about the value of these contents.

Insurers have also been asked to offer two optional covers – insurance for valuable contents (such as jewellery and curios) and personal accident plan (for policyholders and their spouses). In case of the policyholder or the spouse’s death due to one of the specified perils that caused damages to your house, a compensation of Rs 5 lakh per person will be paid out.

Claim settlement up to sum insured

The IRDAI has also made it clear that the policy will have to give a complete waiver of underinsurance. Put simply, if the sum insured chosen by you is lower than the actual value of the property or contents, it will be termed ‘underinsurance’. In such cases, many products in the market today settle the claim proportionately. For example, under such policies, if your property’s value is Rs 2 lakh, but your sum insured is Rs 1 lakh, your claim amount will be reduced proportionately by 50 percent.

So, if your claim is, say Rs 70,000, you will be entitled to only Rs 35,000. However, since the standard product comes with an underinsurance waiver, here, you will get Rs 70,000. “If the sum insured declared by a policyholder is less than what ought to have been declared for the property in question, the policyholder’s claim will not be settled proportionately, but up to the sum insured that is declared,” the IRDAI’s official communication notes.

“This is a useful clause as it limits policyholders’ potential losses in case their sum insured is lower than their property’s valuation. Instead of being compensated proportionally, they will get the claim amount up to the sum insured,” says Abhishek Bondia, Co-founder, Securenow.in

Moneycontrol’s Take

The year 2020 has been the year of insurance awareness, with many flocking to buy life and health insurance policies. Travel and COVID-19-specific policies, too, have seen an increase in demand. However, the same is not the case with home insurance – protecting one of the most precious, and expensive, assets – is not high on the priority list for many. Besides lack of awareness, complex terms and conditions, too, were their undoing. “Regular home insurance policies came with multiple sections, terms, conditions and exclusions that sometimes ended up confusing customers. This is one of the primary reasons why home insurance is not popular. In the case of a ‘standardised’ cover, it is a blanket cover for structure and contents. Customers do not have to struggle to arrive at the right valuation while availing the insurance cover,” says Saroj Satapathy, Chief Operating Officer, JB Boda Insurance and Reinsurance Brokers.

While lay policyholders could still find it difficult to decipher standard product’s clauses, the fact that the terms are set by the insurance regulator will offer comfort. Given that you invest your lifetime’s savings into buying a house, there is every reason to insure it – and a standard product can be a good start.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.