Sachin Pal

Moneycontrol Research

Highlights:

- Everest Industries had a steady quarter- Visaka's margins in Q3 contracted by more than 400 bps

- New product launches to drive earnings

- Everest appears better placed to grow in the current market environment

-------------------------------------------------

Asbestos cement sheet manufacturers Everest Industries and Visaka Industries reported a mixed quarterly performance in the third quarter of FY19. While the profitability of former was supported by tighter cost controls, increase in selling & distribution expenditures hampered the margins of the latter.

Industry reforms and government policies have had a positive impact on the organised building material players as indicated by the robust volume growth in the past few quarters. We look at the quarterly performance of these companies to understand the sector dynamics and the way forward.

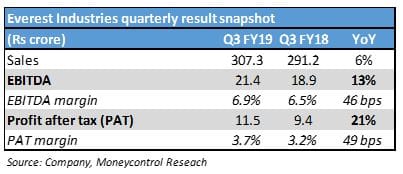

Everest Industries

Revenues for the quarter increased by 6 percent year-on-year (YoY) to Rs 307 crores. Operating profits increased from 19 crores in Q3 FY18 to 21 crores in Q3 FY19 representing a growth of 13 percent YoY. Profit after tax (PAT) also increased by 21 percent as reduction in interest and depreciation expenses offset the higher tax outgo and lower other income.

Steady growth across both its business lines resulted in a decent quarterly performance. The volume growth of the building products (fibre-cement sheets, boards & panels) tapered to 5 percent in Q3 FY19 in comparison to 19 percent in Q2 and 16 percent in Q1 FY19. Higher share of value-added products drove the realisations as well as margins higher in the quarter gone by. Steel building segment had a subdued quarter as the volumes were down 10 percent YoY. However, the jump in realisations aided the 3 percent growth in topline. Margin improvement in Q3 was driven by improvement in execution cycle and large projects, however, the underlying volatility in steel prices continue to have a bearing on the margins on a quarterly basis.

The company appears well-positioned to grow as the building products segment is anticipated to get a boost from the increased government spending on the infrastructure and rural segments. Also, the strong order-book of steel segment provides decent earnings visibility over the next 12-18 months. Everest continues to improvise its portfolio offering through launch of new products. Everest Super, coloured waterproof roofing sheets launched earlier this year, is gaining traction among customers. On the cost front, the company continues to focus on internal business efficiencies through better working capital management and debt reduction.

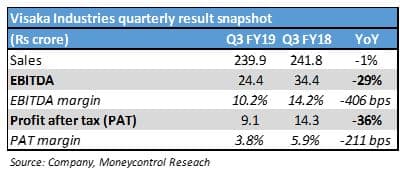

Visaka Industries

Visaka Industries had a weak quarter. Revenues for the quarter declined by 1 percent YoY to Rs 251 crores. Operating profits also declined to 24 crores as the margins contracted by more than 400 bps.

The revenues for building products segment were down 4 percent YoY due to double-digit decline in asbestos cement sheet volumes. Profitability of the segment was hit by a combination of forex losses, lower sales volume and higher selling expenses.

Synthetic yarn segment continues to benefit from the cotton upcycle. While the volumes came in flat, higher realisations boosted the performance of this segment. Going forward, the management expect the yarn division to witness double-digit volume growth along with an improvement in margins.

Synthetic yarn segment continues to benefit from the cotton upcycle. While the volumes came in flat, higher realisations boosted the performance of this segment. Going forward, the management expect the yarn division to witness double-digit volume growth along with an improvement in margins.

The company is nearing the completion of its capex cycle and expects these new launches to boost the topline in coming months. The company has increased its advertising and selling expenditure to the push the sales of its latest roofing product ATUM (integrated solar panel with a cement base). The commencement of new V-Boards plant (capacity 50,000 tons) at Jhajjar (Haryana) has been delayed and it is now expected to come on-stream in the March-April of this calendar year.

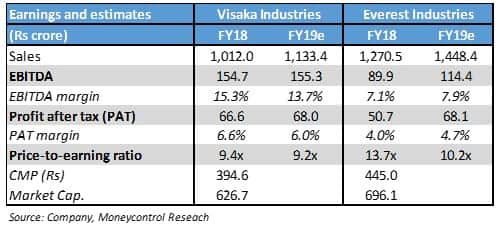

Outlook and recommendation

The profitability of Visaka Industries is expected to remain subdued in the near term as the expenditures related to the new product launches will continue to drag its bottomline for the next 1-2 quarters. In contrast, Everest Industries is consistently working on value-added products to improve its margins and is also working on brand development through marketing activities. The increased focus on costs (reduction in working capital and debt) should aid the margins going forward.

From a valuation standpoint, Visaka trades at a minor discount to Everest due to the presence of cyclical yarn business (~20 percent of revenues) in its portfolio. Everest remains our preferred pick among the two as the company has better return rations and is anticipated to grow faster than its peer.

Also Read: Hyderabad Industries Q3 review: Mixed results not a dampener

For more research articles, visit our Moneycontrol Research page

(Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.