Anubhav Sahu

Moneycontrol Research

Highlights:

- Operating performance was impacted by higher commodity prices and competitive pressure

- Joint ventures: Tata Starbucks and NourishCo posted strong growth

- Price hikes in key tea brands to aid near term margin expansion

- One of the cheapest FMCG stocks

-------------------------------------------------

Tata Global Beverages' (TGB) Q3 FY19 consolidated sales rose seven percent in constant currency terms. On a like-for-like basis, operating sales was 12 percent accounting for the impact of its Russia exit. Profit before tax declined 14 percent due to higher commodity cost and investment behind brands.

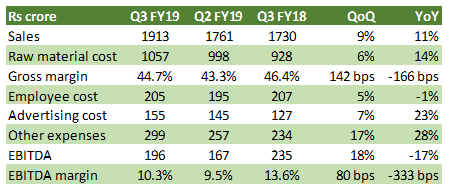

Result snapshot

Source: Company

Key positives

Improvement in operating performance was aided by topline growth in its branded business (90 percent of sales). The key positive was the continued double-digit (14 percent YoY) sales growth for green tea in India, aided by seven percent volume growth.

Its international business accounts for 53 percent of the branded business. In the US, Eight O’Clock Coffee (28 percent YoY) saw continued improvement aided by K-cup (coffee machines) sales. However, margin was impacted due to adverse sales mix and advertising cost. In the UK, Tetley saw 14% value growth (underlying growth of 6%), with market share gain in the black tea segment. Here the company benefited from softening of commodity cost as well.

Both key joint ventures -- Tata Starbucks and NourishCo -- clocked around 30% revenue growth. Tata Starbucks has expanded its store count to 136, with 20 stores opening during the year. NourishCo gained from geographic expansion (launched in West Bengal and Jharkhand) and improvement in Tata Gluco Plus.

Key negatives

India business (47 percent of branded business) saw five percent sales growth on seven percent volume growth – implying elevated competitive challenges and higher cost of tea in India.

Lower share of profits from associates and JVs was a key earnings drag. According to the management of Tata Coffee (subsidiary), the plantations segment was weak due to lower pepper sales and production in the coffee plantation business

Gross margin was impacted (-166 basis points YoY) by higher commodity cost. Higher advertising cost (brand promotion and category development) and other expenses led to 333 bps EBITDA margin impact. Here investors should take note of the management commentary that few of its incremental cost were one-offs. Hence, ballpark EBITDA contraction should be in the of 150-180 bps range YoY.

OutlookGoing forward, the key challenges for the company remains competitive intensity in the mass market. Having said that, price hike undertaken by the company for three key domestic tea brands provides some solace. Greenshoots for the company emerge from better performance from categories like green tea in India and black tea in UK. Premium launches like Tetley Cold Infusions in UK and Tetley Super Teas in Canada, along with traction in instant coffee and K-cup sales (US) should boost margins.

Its margin profile is improving sequentially. Given the price hikes and taking note of one-offs in Q3, we expect its Q4 operating margin to improve by 100-200 bps.

The stock has corrected by over 40 percent from its all-time high of early 2018 and currently trades at 18 times FY20 estimated earnings, which is a significant discount to the FMCG universe. While business verticals -- both on the international and domestic front -- remains in transition, we find it directionally improving and can be accumulated on a staggered basis.

For more research articles, visit our Moneycontrol Research Page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.